一、什么是PLM(产品生命周期管理)

什么是PLM(产品生命周期管理)?产品生命周期管理(Product Lifecycle Management,简称PLM) ,是一种为企业产品全生命周期提供服务的软件解决方案。PLM可以应用于在单一地点或分散在多个地点的企业内部,以及在产品研发领域具 有协作关系的企业之间,集成与产品相关的人力资源、流程、应用系统和信息,以支持产品全生命周期的 信息创建、管理、分发和应用。

PLM是企业信息化的重要组成部分:PLM侧重以产品为核心,将企业智力资产作为一个有机的整体进行合 理有效地管理,从而协同推动新产品的研发和更新迭代,帮助企业组织增强产品开发能力和竞争能力。

1. PLM:生产数据规模化的产物,CAD/PDM概念的延伸

PDM/PLM概念的应用与发展与CAD息息相关:CAD的大量应用,使企业认识到了与产品数据管理的重要性, 从而推进工业数字化、工业4.0和PLM行业的重大变革,加速供应商在解决方案中融入新兴技术的趋势。

PLM完全包含了PDM技术(产品数据管理),是其功能的延伸:PDM主要针对产品开发过程,强调对工程 数据的管理,而PLM在其内容基础上又强调了对产品生命周期内跨越供应链的所有信息进行管理和利用,从 而使特定产品生命周期过程的内外部涉众之间可以更加密切协作,更好地适应市场需求。

2. PLM是企业经营管理的集成支撑环境

使用PLM软件真正管理一个产品的全生命周期,需要与企业经营管理的多系统进行集成:只有PLM可以最大 限度地实现跨越时空、地域和供应链的信息集成,在产品全生命周期内,充分利用分布数据资源和企业智力 资产。因此,PLM系统的价值取决于在企业内能否与ERP、SCM、CRM来集成使用,组成PLM生态系统, 实现更全面意义上的协同工作。

3. PLM功能:以最低的成本和时耗做最正确的研发

PLM最关键的功能在于优化产品研发的全管理流程,增强企业产品的市场竞争力:研发是产品力的坚强基石, PLM通过数据的关联管理可以更好地支持企业产品的研发和变更,帮助其快速回应市场消费需求。同时,PLM 还可以辅助尽早发现和修正错误,从而降低企业试错成本,优化研发流程体验。

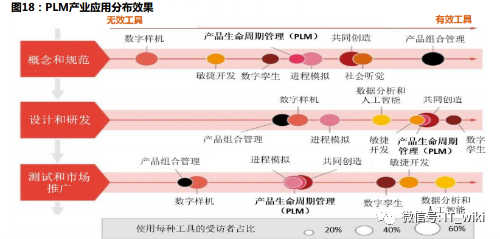

PLM在设计和研发方面应用最为广泛:根据Business data的调查数据,PLM软件最主要的功能是可以缩短产 品研发周期(30.94%),并改善产品服务的设计迭代流程(27.34%),有效降低产品的研发成本。PLM在高 级可视化、预测分析以及工程制造方面的应用也加速了该技术的发展。

4. PLM应用:为数据资源提供个性/差异化的存储和管理

PLM市场自2015年起正在逐渐走向定制化,并推出个性化的行业解决方案:PLM系统可以根据企业所属的 不同行业制定差异化解决方案,例如达索系统与IBM公司推出的CATIA航空航天解决方案,西门子公司为船舶 业、全球能源与公共事业行业开发的Teamcenter 解决方案等,都是针对企业的要求而进行的个性化研发。

行业头部供应商西门子、PTC和已基本完成由许可证向订阅模式的转型:为了提供更加灵活的产品功能体验, PLM软件正从永久许可模式转向订阅模式,以确保客户能够访问产品的最新版本和增强功能。2017年至 2019年,PTC实现了毛利率从72%到76%的增长,订阅的高毛利率是公司毛利率增长的主要驱动因素。

5. PLM产品分类

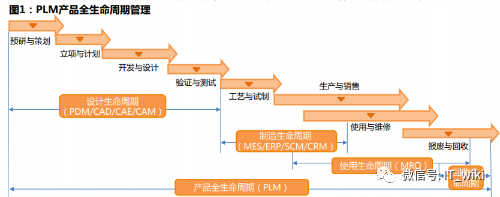

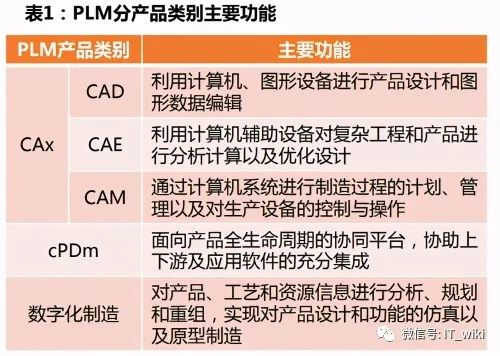

PLM产品主要可以分为CAx,cPDm和数字化制造三类:PLM将计算机辅助设计(CAD),辅助分析(CAE)、 辅 助制造(CAE)以及产品数据管理(PDM)等系统衔接一体,使企业能够对产品服务从设计、研发、生产最终报废 等全生命周期的设计及信息进行高效和经济的应用、集成与管理。

PLM软件供应商来源可以分为PDM/CAD工具类软件和ERP软件两类:由于ERP与PLM系统之间无明显技术 壁垒,而ERP厂商往往具有良好的研发制造企业泛客户群,因此会选择进军PLM业,打通企业信息化链条。

二、PLM的市场规模

1. 未来三年:市场前景广阔,2023年全球规模有望达到263亿美元

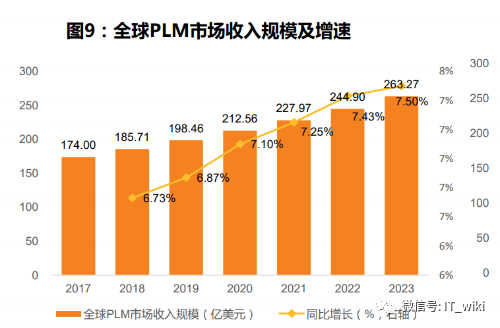

全球PLM市场前景广阔:根据Quadrant Knowledge Solutions的调研报告,2018年-2023年全球PLM市 场将保持持续增长趋势,市场规模将于2018年的185.7亿美元增至2023年达到263.3亿美元,全球PLM市 场在2018-2023年的CAGR约为7.2%。

内部配置领域是PLM市场发展趋势:在部署类型上,PLM市场主要由本地部署和专业服务占据,2018年 二者份额共计达93.1%,从市场趋势看,内部配置是大型传统行业发展PLM的首选。

2. 下游客户:新冠疫情影响深远,PLM仍处于投资的上行通道

根据e-works的统计,2019年全球PLM市场投资规模达514亿美元,增长率为7.6%,其中数字化制造市场 增长8.6%,达到8.9亿美元。全球大部分PLM投资来自汽车、国防航空、高科技和工业机械等行业。

2020年受新冠疫情影响,消费需求的衰减将一定程度上传导至PLM市场,全球PLM行业的市场投资增长率 预估为2.4%,但结合经济复苏效应与产业实际需求,PLM仍处于投资的上行通道。

大部分企业认为PLM企业值得继续投入:根据CIMdata的调查,近58%的调查企业每年PLM预算超过100 万美元,84%的企业表示2020年将对PLM投入保持不变或增长。

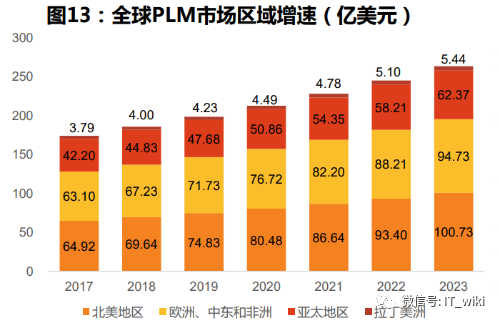

3. 地域分布:区域差异化显著,北美地区持续主导

区域部署差异化,北美地区继续主导行业市场:来自北美和欧洲,中东和非洲地区的收入共同占PLM总市场收 入的73.7%,北美和西欧发达地区将持续为PLM软件供应商提供最多的商机。

主要原因为,一方面北美强大的财务状况使其能够在PLM先进解决方案和技术上大规模投资,为该市场提供了 竞争优势;另一方面,该地区主要PLM软件供应商,如PTC,甲骨文、IBM竞争激烈,技术发展变革较快,为 企业争夺全球市场份额提供更有利条件。

中国PLM市场规模较低:对于中国PLM厂商来说,进入市场较晚,资本积累还需一段路程,但中国整体PLM市 场的利好环境,会给本土PLM厂商更多的市场机会和挑战。

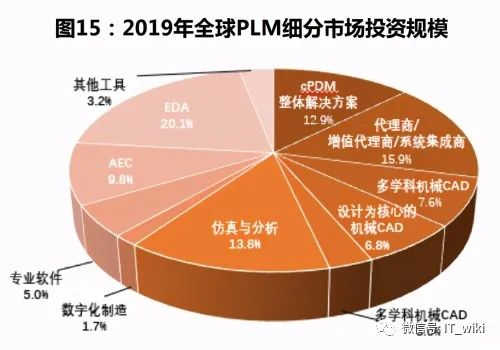

4. 产业结构:工具类软件规模较高

行业工具类软件规模较高,市场竞争集中:工具类软件(Tools)包括设计仿真和CAX系列,在全球PLM 市场中占比达31.2%,我国工具类软件市场规模则超过了60%。

目前的产业结构中,国内供应商可以大致分成三类:

①以计算机辅助设计(CAD)为主体,代表性厂商有西门子、达索和PTC;

②以PDM为主体的PLM厂商,主要代表性厂商包括北京艾克斯特、清软英泰、上海思普和武汉开目等;

③以PLM+ERP为主的信息化解决方案提供商,包括用友、甲骨文、SAP等。

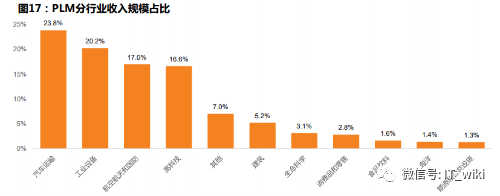

5. 横向趋势:PLM正逐渐从主流离散制造行业进入非传统行业

PLM解决方案的主要应用行业为汽车运输、工业设备、航空航天和国防以及高科技工业部门,它们共计占 2018年全球PLM市场收入的77.6%,预计2018-2023年的年复合增长率为7.4%、7.1%、6.8%和7.2%。

未来几年,PLM主要厂商正在试图凸显差异化竞争:仿真分析、系统工程等领域将会持续增长;服务收入 在cPDm市场的占比逐渐降低;PLM软件将更多进入零售业、能源业、食品饮料业等非传统行业。

此外,云PLM服务在中小企业和非传统行业中获得的市场吸引力持续上升,PLM供应商将继续专注于提高 他们的技术能力,并提升整体技术服务研发,以支持组织实现数字化企业战略的愿景。

6. 纵向趋势:与人工智能、机器学习领域密切结合

PLM在主要通过与人工智能(AI)和机器学习(ML)两大领域结合而推动工业4.0的发展,其在设计和研发 方面应用最为广泛:智能互联产品的开发和管理方式正在改变PLM的实现途径,用户对于PLM的使用将不再 局限于管理层面,而是在此基础之上寻求产品/业务的优化与创新。;在AI和ML的先进企业中,61%已完全集 成的PLM系统,而未接触两者的企业中,PLM的应用比例仅为12%。

三、竞争格局

1. 企业竞争格局:全球主流市场被外企垄断

PLM行业主流市场被外国企业垄断:根据Quadrant Knowledge Solutions的统计,PTC,达索系统和西门子是 全球PLM市场中表现最佳的前三大技术领导者。

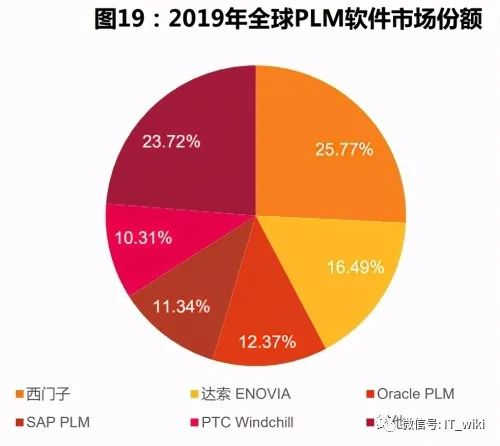

在PLM的主流应用市场中,共有14,971家企业在使用PLM软件产品。西门子的 Teamcenter 和 达索系统的 ENOVIA软件最受青睐,分别在市场份额中占比25%和16%。提供PLM的专业公司包括达索系统、西门子、PTC 等;由于ERP与PLM都体现流程管理的思想,关系密切,一些ERP巨头如SAP、甲骨文、IFS也提供PLM软件。

2. 产品选择倾向:主要受供应商行业优势与地域位置影响

西门子与达索系统都在美国拥有最高的市场份额,其客户的地域分布具有本土化倾向;在行业方面,企业客 户在选择PLM产品时可能会优先考虑供应商的行业优势,达索系统专注于航空航天领域,而西门子则在汽车 行业具有一定优势。

3. 企业竞争格局:中国进入市场较晚,行业分布离散化

中国企业进入市场较晚,集中于机械、电子领域:2009年,国内软件企业用友、金蝶以并购的方式涉足PLM, 与外企存在较大的技术服务差距;服务领域方面,三大PLM国外厂商的服务范围覆盖较为全面,而大部分的本 土PLM厂商则呈现出行业离散型特征,无法全面覆盖医药制造、化工、食品饮料和其他新兴行业市场。

4. CAD厂商领跑行业

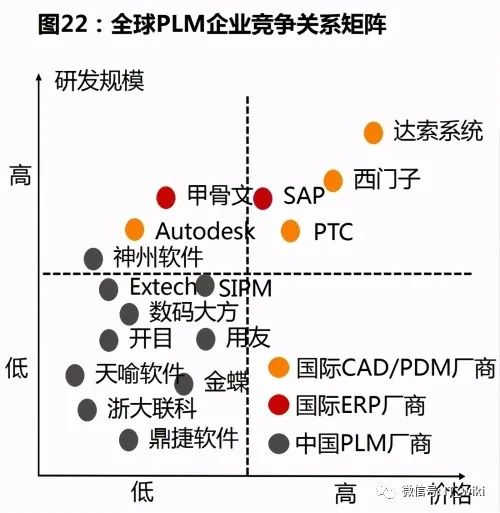

CAD厂商处于技术领先位置,持续领跑PLM行业:根据2010年CIMdata对PLM的统计,三大CAD国际巨头 PTC、达索系统和西门子已经处于行业绝对领先位置,三者共计市场份额占比达到52%。近十年中,CAD厂商 在PLM行业持续拥有较大的市场影响力,CAD领先厂商Autodesk也一直是PLM领域的有力竞争者之一。

可能的原因是,一方面,PLM/PDM技术的发展与CAD的发展息息相关,正是CAD的大量应用,才使企业认识 到了产品数据管理的重要性;另一方面,根据PLM概念的发展历史,其是对CAD的集成延伸,因此CAD 厂商 进入PLM行业具有一定的技术与客户资源先决优势。

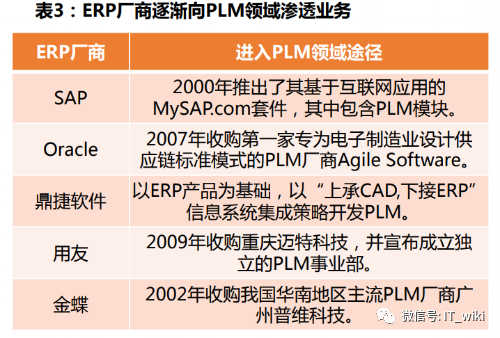

5. ERP厂商进入PLM市场的趋势呈现

二者并无技术壁垒:相比CAD/PDM厂商,ERP厂商在资源管理与组织协同方面具有更强的竞争能力;PLM 供应商则多提供全面的研发技术组合,包括设计,仿真,产品数据管理和协作技术等。

ERP背景的PLM厂商主要包括SAP、Oracle甲骨文、鼎捷软件、用友、金蝶等。根据Quadrant Knowledge Solutions的统计,虽然大多数PLM供应商可能提供所有的核心功能,但其功能的广度和深度存在差异;技术 平台,集成BOM管理的复杂性和基于模型的数字孪生管理战略是企业最具竞争力的差异化因素。

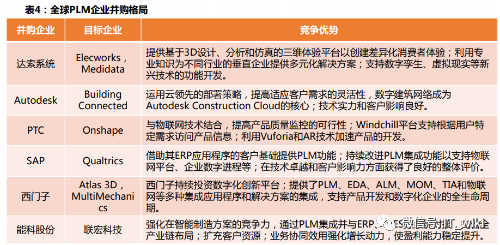

6. 行业竞争动态化,企业并购活跃

全球行业并购活跃:根据CIMdata与e-works的研究统计,2019年PLM市场共发生106起并购案例,略低于 2018年的123起和2017年的135起,绝大部分PLM市场被业界领导厂商掌控。

风险提示

(1)疫情影响下游制造业客户投资规模受限。工业软件主要面对制造业企业,行业中,中小企业占多数,资金预算 有限,需要投入生产设备或生产材料,疫情影响下,公司削减或推迟工业预算。

(2)PLM厂商竞争激烈。公司目前和潜在的竞争对手既有大而有名气的公司,也有新兴的初创公司。激烈的竞争可 能限制或减少公司的市场份额,进而降低公司的收入和利润。

(3)工业互联网发展不及预期。受疫情影响,下游制造业客户削减工业预算,PLM厂商的收入增长率可能下降,工 业软件行业的发展可能会受到限制。

(4)我国PLM厂商发展不及预期。工业软件属于高技术壁垒行业,我国PLM行业相比于国际大厂商起步较晚,技术 优势落后,发展较为缓慢,一旦企业研发没有找对方向,就可能处于技术弱势地位。

翻译:

PLM, product life cycle management

Product Lifecycle Management (PLM) is a software solution that provides services for the entire life cycle of enterprise products. PLM can be used in a single location or within multiple locations, as well as between companies collaborating in product development, to integrate product-related human resources, processes, applications, and information to support the creation, management, distribution, and application of information throughout the product lifecycle.

PLM is an important part of enterprise informatization: PLM focuses on the product as the core, the enterprise intellectual assets as an organic whole for reasonable and effective management, so as to jointly promote the development of new products and update iteration, help enterprises to enhance product development capabilities and competitiveness.

PLM: The product of production data scale, an extension of the CAD/PDM concept

The application and development of PDM/PLM concept is closely related to CAD: the large number of applications of CAD has made enterprises realize the importance of product data management, thereby promoting major changes in industrial digitalization, Industry 4.0 and PLM industries, and accelerating the trend of suppliers integrating emerging technologies into their solutions.

PLM fully incorporates PDM technology (Product Data Management) and is an extension of its capabilities: PDM mainly focuses on the product development process and emphasizes the management of engineering data, while PLM, based on its content, emphasizes the management and utilization of all information across the supply chain during the product life cycle, so that internal and external stakeholders of a particular product life cycle process can cooperate more closely and better adapt to market needs.

PLM is an integrated support environment for enterprise operation and management

Using PLM software to truly manage the full life cycle of a product requires integration with multiple systems of business management: only PLM can maximize the integration of information across time, geography and supply chain, and make full use of distributed data resources and enterprise intellectual assets throughout the product life cycle. Therefore, the value of PLM systems depends on whether they can be integrated with ERP, SCM, and CRM within the enterprise to form a PLM ecosystem and achieve a more comprehensive sense of collaborative work.

PLM function: to do the most correct research and development at the lowest cost and time

The most critical function of PLM is to optimize the whole management process of product development and enhance the market competitiveness of enterprise products: Research and development is a strong cornerstone of product strength, PLM can better support the development and change of enterprise products through data association management, and help it quickly respond to market consumer demand. At the same time, PLM can assist in the early detection and correction of errors, thereby reducing the cost of trial and error and optimizing the R&D process experience.

PLM is the most widely used in design and research and development: According to the survey data of Business data, the most important function of PLM software is to shorten the product research and development cycle (30.94%), improve the product service design iteration process (27.34%), and effectively reduce the product research and development cost. The application of PLM in high-level visualization, predictive analytics, and engineering manufacturing is also accelerating the development of this technology.

PLM applications: Provide personalized/differentiated storage and management for data resources

The PLM market has been moving towards customization since 2015, with the introduction of personalized industry solutions: PLM systems can be developed according to the different industries of the enterprise to develop differentiated solutions, such as Dassault Systemes and IBM launched CATIA aerospace solution, Siemens for the shipping industry, global energy and utilities industry Teamcenter solution, etc., are personalized research and development for the requirements of enterprises.

Industry leaders Siemens, PTC and PTC have largely completed the transition from a license to a subscription model: In order to provide a more flexible product feature experience, PLM software is moving from a perpetual license model to a subscription model to ensure that customers have access to the latest versions and enhancements of the product. From 2017 to 2019, PTC achieved gross margin growth from 72% to 76%, with high gross margin from subscriptions being the main driver of the company’s gross margin growth.

PLM product classification

PLM products can be divided into CAx, cPDm and digital manufacturing: PLM integrates computer-aided design (CAD), aided analysis (CAE), aided manufacturing (CAE) and product data management (PDM) systems, enabling enterprises to efficiently and economically apply, integrate and manage the design and information of the whole life cycle of product services from design, research and development, production and final scrap.

PLM software suppliers can be divided into PDM/CAD tool software and ERP software: because there is no obvious technical barrier between ERP and PLM system, and ERP manufacturers often have a good R & D manufacturing enterprise customer base, so they will choose to enter the PLM industry to open up the enterprise information chain.

Market size

The next three years: The market has broad prospects, and the global scale is expected to reach $26.3 billion in 2023

The global PLM market has broad prospects: According to the research report of Quadrant Knowledge Solutions, the global PLM market will continue to grow from 2018 to 2023, and the market size will increase from $18.57 billion in 2018 to $26.33 billion in 2023. The global PLM market will grow at a CAGR of about 7.2% from 2018 to 2023.

The field of internal configuration is the development trend of the PLM market: in terms of deployment types, the PLM market is mainly occupied by local deployment and professional services, with a total share of 93.1% in 2018. From the perspective of market trends, internal configuration is the first choice for the development of PLM in large traditional industries.

Downstream customers: The impact of the COVID-19 epidemic is far-reaching, and PLM is still in the upward channel of investment

According to e-works, the global PLM market investment reached $51.4 billion in 2019, with a growth rate of 7.6%, of which the digital manufacturing market grew 8.6% to $890 million. The majority of global PLM investments are in industries such as automotive, defense aerospace, high-tech and industrial machinery.

In 2020, affected by the COVID-19 epidemic, the decline in consumer demand will be transmitted to the PLM market to a certain extent, and the market investment growth rate of the global PLM industry is estimated to be 2.4%, but combined with the economic recovery effect and the actual demand of the industry, PLM is still in the upward channel of investment.

According to CIMdata, nearly 58 percent of surveyed companies have annual PLM budgets of more than $1 million, and 84 percent say PLM spending will stay the same or increase in 2020.

Geographical distribution: There is significant regional differentiation, and North America continues to dominate

North America continues to dominate the industry market: Revenues from North America and the EMEA region together account for 73.7% of total PLM market revenues, and the developed regions of North America and Western Europe will continue to provide the most opportunities for PLM software vendors.

The main reasons are: on the one hand, North America’s strong financial position has enabled it to invest heavily in advanced PLM solutions and technologies, providing a competitive advantage to this market; On the other hand, major PLM software suppliers in the region, such as PTC, Oracle, and IBM, are fiercely competitive and rapidly changing in technology development, providing more favorable conditions for enterprises to compete for global market share.

China’s PLM market is relatively small: for Chinese PLM manufacturers, it is late to enter the market and capital accumulation still needs a long way, but the favorable environment of China’s overall PLM market will give local PLM manufacturers more market opportunities and challenges.

Industrial structure: The scale of tool software is high

The scale of industry tool software is relatively high, and market competition is concentrated: Tools software, including design simulation and CAX series, accounts for 31.2% in the global PLM market, and the market size of China’s tool software exceeds 60%.

In the current industrial structure, domestic suppliers can be roughly divided into three categories:

① Computer-aided design (CAD) as the main body, the representative manufacturers are Siemens, Dassault and PTC;

② PLM manufacturers with PDM as the main body, the main representative manufacturers include Beijing Exeter, Qingsoft Yingtai, Shanghai Sipu and Wuhan Kaimu, etc.;

③ PLM+ERP based information solution providers, including UF, Oracle, SAP, etc.

Horizontal trend: PLM is gradually moving from the mainstream discrete manufacturing industry into non-traditional industries

The major application industries for PLM solutions are the automotive transportation, industrial equipment, aerospace and defense, and high-tech industrial sectors, which together accounted for 77.6% of the global PLM market revenue in 2018 and are expected to grow at a CAGR of 7.4%, 7.1%, 6.8%, and 7.2% from 2018 to 2023.

In the next few years, the major PLM vendors are trying to highlight the differentiation of competition: simulation analysis, systems engineering and other areas will continue to grow; The proportion of service revenue in cPDm market is decreasing gradually. PLM software will enter more non-traditional industries such as retail, energy, food and beverage.

In addition, the market traction gained by cloud PLM services in smes and non-traditional industries continues to grow, and PLM vendors will continue to focus on improving their technical capabilities and overall technology services R&D to support organizations in realizing the vision of their digital enterprise strategy.

Vertical trend: Closely integrated with artificial intelligence and machine learning fields

PLM is driving the development of Industry 4.0 mainly through the combination of artificial intelligence (AI) and machine learning (ML), and it is most widely used in design and research and development: The development and management of intelligent and connected products is changing the way PLM is implemented, and users will no longer be limited to the use of PLM at the management level, but will seek product/business optimization and innovation on this basis. ; Among advanced AI and ML organizations, 61 percent have fully integrated PLM systems, while only 12 percent of organizations that do not have access to both have PLM applications.

The competitive landscape

Corporate competition pattern: The global mainstream market is monopolized by foreign companies

The PLM industry is dominated by foreign players: According to Quadrant Knowledge Solutions, PTC, Dassault Systemes and Siemens are the top three best-performing technology leaders in the global PLM market.

In the mainstream PLM application market, 14,971 enterprises are using PLM software products. Siemens’ Teamcenter and Dassault Systemes’ ENOVIA software were the most popular, accounting for 25% and 16% of the market, respectively. Professional companies that provide PLM include Dassault Systemes, Siemens, PTC, etc. Since ERP and PLM both embody the idea of process management and are closely related, some ERP giants such as SAP, Oracle and IFS also provide PLM software.

Product selection tendency: mainly affected by the supplier’s industry advantages and geographical location

Both Siemens and Dassault Systemes have the highest market share in the United States, and the geographical distribution of their customers tends to be localized. In terms of industry, enterprise customers may prioritize a supplier’s industry strengths when selecting PLM products, with Dassault Systemes focusing on the aerospace sector and Siemens having certain strengths in the automotive industry.

Enterprise competition pattern: China entered the market late, and the industry distribution became discrete

Chinese enterprises entered the market late and concentrated in the fields of machinery and electronics. In 2009, domestic software companies UF and Kingdee got involved in PLM by way of mergers and acquisitions, and there was a big technical service gap with foreign companies. In terms of service fields, the service coverage of the three major PLM foreign manufacturers is more comprehensive, while most of the local PLM manufacturers show the characteristics of the industry dispersion, unable to fully cover the pharmaceutical manufacturing, chemical, food and beverage and other emerging industry markets.

CAD manufacturers lead the industry

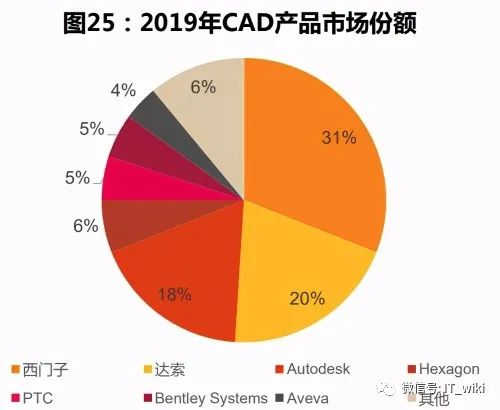

CAD manufacturers are in the leading position of technology and continue to lead the PLM industry: According to the statistics of CIMdata on PLM in 2010, the three international CAD giants PTC, Dassault Systemes and Siemens have been in the absolute leading position in the industry, and the total market share of the three has reached 52%. In the past decade, CAD vendors have continued to have a large market influence in the PLM industry, and CAD leader Autodesk has been one of the strong competitors in the PLM field.

The possible reasons are that, on the one hand. The development of PLM/PDM technology is closely related to the development of CAD. And it is the large number of applications of CAD that make enterprises realize the importance of product data management. On the other hand, according to the development history of the PLM concept. It is an integrated extension of CAD, so CAD manufacturers have certain advantages in technology and customer resources to enter the PLM industry.

ERP vendors are entering the PLM market

There is no technical barrier between the two: compared with CAD/PDM manufacturers, ERP manufacturers have stronger competitiveness in resource management and organizational collaboration; PLM vendors offer a comprehensive portfolio of R&D technologies, including design, simulation, product data management, and collaboration technologies.

PLM manufacturers with ERP background mainly include SAP, Oracle, Dingjie Software, UF, Kingdee and so on. According to Quadrant Knowledge Solutions, while most PLM vendors may offer all of the core features. There are differences in the breadth and depth of their capabilities. The technology platform, the complexity of integrated BOM management and the model-based digital twin management strategy are the most competitive differentiators for enterprises.

Dynamic industry competition and active mergers and acquisitions

Global industry M&A activity: According to CIMdata and e-works research statistics. There were 106 M&A cases in the PLM market in 2019, slightly lower than 123 in 2018 and 135 in 2017. And the majority of the PLM market is controlled by industry leaders.

Risk warning

(1) The epidemic affected the investment scale of downstream manufacturing customers. Industrial software mainly faces manufacturing enterprises, in the industry, small and medium-sized enterprises account for the majority. The capital budget is limited, need to invest in production equipment or production materials, under the impact of the epidemic. The company cut or delay the industrial budget.

(2)PLM manufacturers are highly competitive. The company’s current and potential competitors range from large and established companies to emerging startups. Intense competition can limit or reduce the company’s market share, which in turn reduces the company’s revenue and profit.

(3) The development of the industrial Internet is not as expected. Affected by the epidemic, the downstream manufacturing customers cut industrial budgets. The revenue growth rate of PLM manufacturers may decline. And the development of the industrial software industry may be limited.

(4) The development of China’s PLM manufacturers is not as expected. Industrial software belongs to the high-tech barriers industry. China’s PLM industry compared with the international manufacturers started late, technical advantages lag behind. The development is relatively slow, once the enterprise research and development does not find the right direction. It may be in a weak position in technology.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源于未来智库;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。