一、商业银行数字化转型的时代背景

随着数字技术产业化和传统产业数字化,数字技术的快速发展和广泛应用逐步改变了社会和经济的运行环境与运行模式。在消费互联网仍在不断演进、电子政务水平持续提升之时,工业互联网和产业互联网的发展使得大量传统企业的经营决策、生产运营和外部协同也变得高度数字化和智能化,形成了数字经济这一新的经济形态。数字经济有三个主要特征:一是数据成为推动经济发展的关键生产要素;二是数字基础设施成为新的经济基础设施;三是需求和供给日益走向协调。数字经济使资源配置效率得以优化,社会交易成本显著降低,因此,其已成为更高质量发展的经济形态。数字化转型网szhzxw.cn

2017年,牛津经济研究院和华为共同发布了一份名为《数字溢出》的数字经济研究报告。报告分析认为,投资ICT数字技术长期回报是非ICT 投资回报的6.7 倍;除金融、通信等高度依赖数字技术的行业外,2000年以来传统行业包括房地产、农业和采矿业数字技术投资复合增长率超过10%;同时,预测到2025 年全球数字经济占比将高达24.3%。这三个数字背后的逻辑非常清晰,那就是数字技术已经成为企业与行业生产效率和创新能力提升的主要推动力。

见证了互联网在零售、社交和金融支付等领域带来的颠覆,或许会更容易理解“数字化转型将是关系到商业银行生存和发展的一场变革”。相比过去银行全面控制产品和交付,侧重内部职能和局部流程,以提升效率和便利性为主要目标的信息化建设,数字化转型是在社会和经济迈向数字化时代的背景下,由数字技术驱动的银行产品和服务、客户经营、风险控制、运营模式以及与外部合作伙伴和生态关系的一次跳跃性演进。新冠肺炎疫情全球爆发使商业银行引发了对互联网和数字技术更多的关注,增强了数字化转型的紧迫感。同时,转型并非会自然发生并获得成功,银行需要把数字化转型放到战略的核心位置,通过分析未来数字经济的形态,找准定位,以终为始确定转型的目标和路径,以坚定的执行力推动实施。数字化转型网szhzxw.cn

二、商业银行数字化转型的五个重心

1、数字化转型要求整个组织拥抱科技数字化转型网szhzxw.cn

科学技术是第一生产力。回望历史,无论是栽培技术带来的农业革命,还是由蒸汽技术、电气技术、计算机与信息技术带来的三次工业革命,无一不是技术取得重大突破而引发的划时代变革。今天,以大数据、云计算、人工智能、物联网和区块链等技术为代表的新一代数字技术,正在开创一个数字社会和数字经济新纪元。数字化转型网szhzxw.cn

随着信息技术发展和互联网应用的普及,一些商业银行先后提出科技引领战略,加大资源投入以科技手段提升经营效率和质量。然而,现实中对于什么是“科技引领”在认识上一直都还存在着偏差和误区。科技引领战略提出的背后是对科技已成为推动银行发展最关键变量的认识,那些以工资待遇和干部职数为目的的地位提升,或谁强谁说了算的事关话语权分配的理解无疑都过于偏颇和狭隘。科技引领应有的内涵是运用数字技术对银行进行再造,不仅为了提高效率或降低成本,更重要的是实现自身的进化,以适宜外部环境发生的广泛而深刻的变化。科技引领要求整个组织拥抱科技,所有人员都形成利用科技手段优化、变革和创新的思维方式和行为习惯。有效实施科技引领战略需要科技与业务深度融合,技术和业务双轮驱动。科技人员在技术能解决什么问题的认识方面具有优势,业务人员对金融产品、风险和经营有更全面的理解,两者唯有密切协作、相互启发和促进才能充分发挥数字技术的全部潜力创造业务价值。实施科技引领战略同样要求科技更加前置,深入业务规划和决策中,与业务共同承担业务发展的责任。数字化转型网szhzxw.cn

2、敏捷是数字化转型必备的组织能力数字化转型网szhzxw.cn

当前,我们能看清的是数字社会和数字经济未来发展的方向和总图景,而未来的微观结构和具体形态的形成具有高度的不确定性,甚至超出我们今天的想象。受技术本身发展、新商业模式探索、众多参与主体的合作与竞争、政策调整以及行为习惯变化等诸多因素的影响,数字社会和数字经济的发展必定是一个持续创新、试错、迭代演进的过程。因此,在难以预测的动态环境中能够敏锐感知变化,迅速做出反应的敏捷能力,成为数字化转型的必备能力。对于商业银行而言,敏捷组织成为科技与业务融合在组织和机制层面的保障。

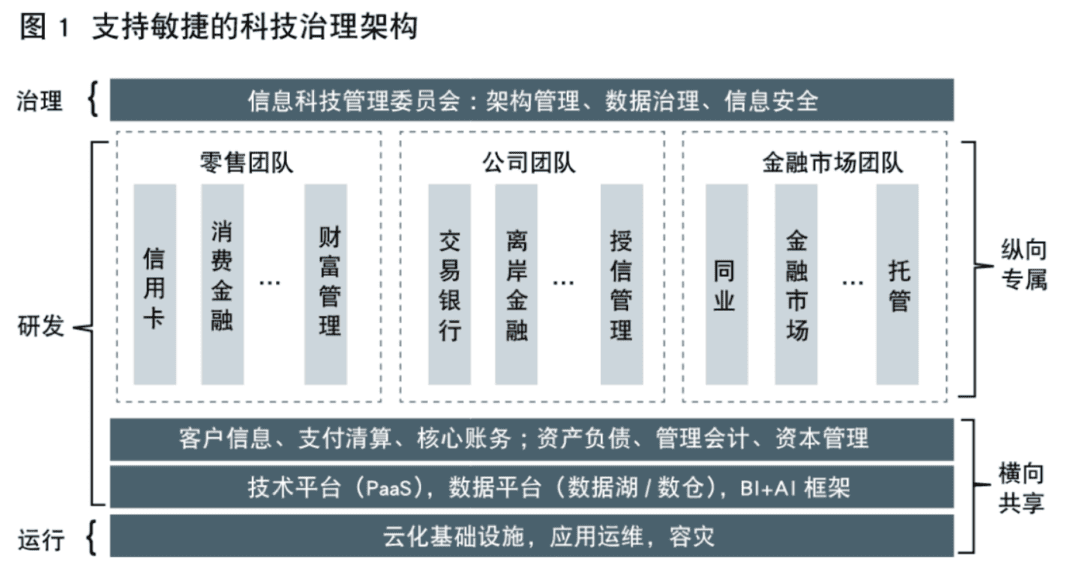

传统银行科技治理模式存在诸多弊端。一方面,集中化的科技资源管理导致过于强调统一规划和统一建设,难以做到技术最优地匹配业务的差异性,大量跨业务线、跨部门的协调使得行动变得迟缓。另一方面,部门银行下以项目驱动的系统建设模式又导致大量的系统孤岛、数据割裂和重复建设。此外,旧有治理模式下的条线意识无形之中拉大了科技与业务的距离。数字化转型需要新的科技治理模式,以建立融入了科技要素的业务敏捷能力(见图1)。

资源配置方面,将承担业务线相关渠道、产品、风险和运营系统建设任务的研发团队配置到业务线,与业务人员共同承担业绩指标,科技负责人向业务主管行长和CIO双线汇报。其余研发资源承担中后台系统建设任务,同时为所有研发团队提供基础技术平台和共享应用支撑能力。架构管理、数据标准及信息安全等重要科技职能实行统一管理,所有科技团队都要遵从这些领域的制度流程和技术规范。数字化转型网szhzxw.cn

运作机制方面,配置到业务线的研发人员与业务合署办公,科技骨干参与日常业务规划和经营活动,赋予具有业务思维的科技人员更多项目规划和决策权。同时,项目驱动的系统建设模式向产品驱动和运营驱动模式转变,使科技投入能够更加聚焦于业务价值的交付。数字化转型网szhzxw.cn

在研发模式方面,推动传统瀑布模式向敏捷模式转换,建立敏捷方法与CMMI实践相结合的组织级研发体系。敏捷方法实现快速交付, CMMI提供完整的组织级流程和框架,实现对业务敏捷响应的同时有效保证软件质量,控制大型项目的风险。数字化转型网szhzxw.cn

3、数据是数字化转型的核心资源

数据从来都至关重要,让全社会都认识到数据的价值,互联网发挥了重要作用。互联网平台促进海量数据的产生和汇聚,又通过对数据的利用展现了令人惊叹的价值。2020年4月,中央关于要素市场化配置的首个文件中,将数据作为一种新的生产要素类型,与土地、劳动力、资本、技术等并列,表明数据已成为数字经济的关键生产要素。数字化转型网szhzxw.cn

国内银行对数据的应用大致可以分为三个阶段。早期关注有限的客户数据、账户数据、核算数据以及授信客户的财务数据,为的是满足会计和财务需要。随着监管要求变化和竞争日趋激烈,银行开始收集运用更全面的业务数据,在客户分析和精准营销之外主要服务于内部精细化管理,满足资金转移定价、管理会计、资产负债和资本管理需要。当互联网和科技公司开始渗透到金融业务领域,伴随着大数据技术日益成熟和普及,银行逐步扩大各类外部数据的运用,在内外部数据支持下,以线上线下结合的新模式开展客户经营和风险管理(见图2)。数字化转型网szhzxw.cn

银行围绕信息收集和处理开展业务,天然具有数据驱动的业务特性。为全面实现经营管理数字化和智能化,银行特别需要在数据治理和基础平台建设方面付出更大的努力。数字化转型网szhzxw.cn

当前,数据质量、数据孤岛、数据安全等问题在全行业依然普遍。扫除这些障碍需要将数据治理作为一项重要的基础工作持续来抓。在建立制度流程、标准规范等常规治理工作之外,要着重做好以下几项工作:一是超越技术视角建立面向业务的资产管理体系,让业务人员和算法工程师对数据资产及各维度信息一目了然;二是对数据进行分级分类,通过明确使用权限和建立高效审批程序实现数据全行共享;三是建立集成的数据治理平台和工具,赋能数据分析和系统设计研发,实现数据治理闭环管理;四是意识教育、制度规范和技术手段并重,全面加强数据安全和个人信息隐私保护。数字化转型网szhzxw.cn

以传统数据仓库、数据集市和商业智能工具为主的技术体系无法支持对各类非结构化、半结构化数据的挖掘和分析,银行需要对标领先的互联网科技公司建立更为强大的数据能力。一是引入人工智能(AI)技术,借助机器学习、深度学习算法提升数据挖掘应用能力。支持基于大数据洞察的客户营销和风险管理,基于人脸等生物识别的安全认证,基于语音识别的自动化服务,以及证照、单据与合同文本要素提取等应用场景。二是大数据能力平台化,即通过对大数据技术栈相关技术组件和框架的集成与整合,实现复杂数据处理流程的线上化和自动化,使人员投入能够聚焦于数据业务价值的挖掘,大幅提升未来常态化数据分析工作的效率和效能。数字化转型网szhzxw.cn

4、云计算是数字化转型的技术方向

数字经济时代,包括商业银行在内的各类经济主体和生态形成广泛的数字化连接,金融服务呈现出显著的多元化、数字化和场景化特征,极致体验成为服务选择的基本要求,价值观和情感演变为影响因素,基于事件的金融需求也将变为常态。对于具有一定规模、寻求业务均衡发展的商业银行,需要采用新的技术路线和架构体系构建面向未来的业务系统,技术和架构转型的主流方向是云原生(Cloud Native)和网格应用与服务架构(MASA – Mesh App and Service Architecture)。数字化转型网szhzxw.cn

就云计算技术体系而言,建立在虚拟化和容器技术之上基础设施云已成熟而稳定。云原生是在基础设施云之上关于系统构建的技术和理念,云原生隐含了未来应用都将运行在云上的趋势判断,不论是公有云、私有云还是混合云。2013年云原生概念被正式提出,2015年云原生计算基金组织(The Cloud Native Computing Foundation,CNCF)成立后,随着更多厂商的不断加入和更多项目的实施,云原生技术体系和工程方法日渐完善和成熟,逐步形成一批事实上的工业标准,引领了技术的发展方向。云原生代表技术包括容器、服务网格、微服务、不可变基础设施和声明式API,以及DevOps工具和流程。基于云原始技术体系可构建容错性好、弹性伸缩、易于维护的松耦合系统,不仅可以使企业获得持续交付、快速响应的敏捷创新能力,同时保证了系统的高可用性和安全性,这是过去只有领先互联网公司才具备的技术能力。云原生是一个内在要素有机结合的技术体系和工程方法,单一和局部应用都无法获得能力的全面提升。数字化转型网szhzxw.cn

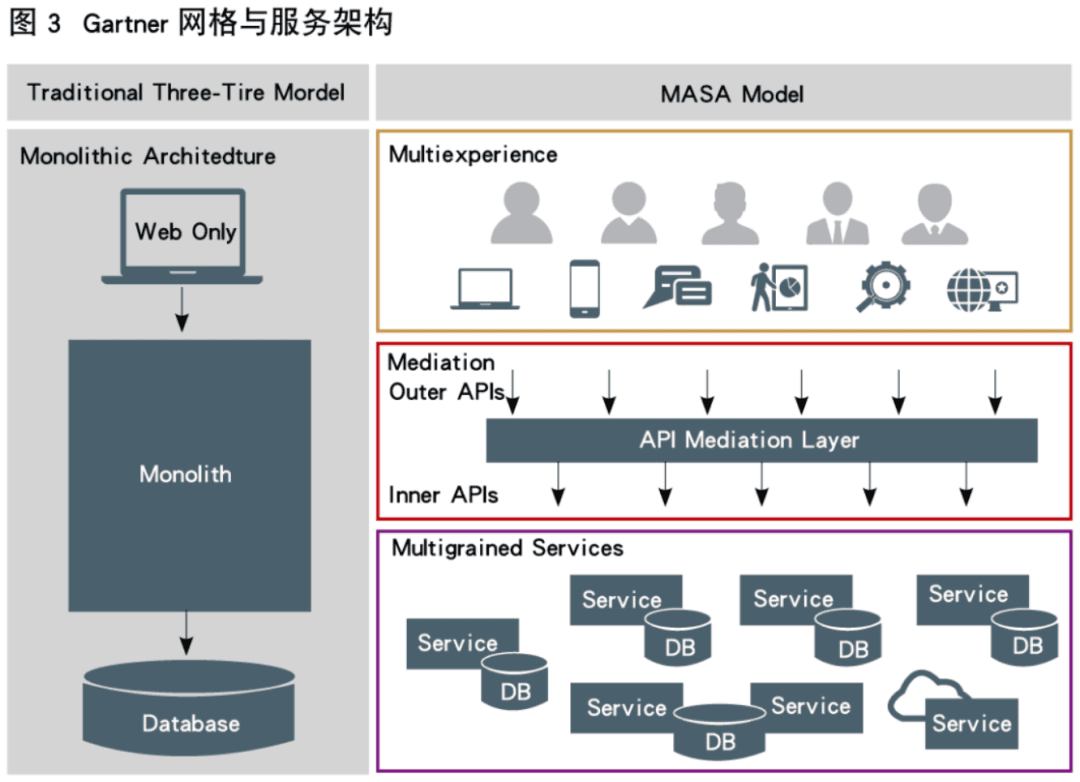

应用架构方面,Gartner公司通过对众多实践进行的提炼和总结,结合数字技术和应用生态的最新发展提出的网格与服务架构(MASA),为银行新的应用架构提供了最好的参照。这是一个新的三层架构:以体验为核心,为适应不同场景开发的各类前端应用层;以业务敏捷为目标,对传统单体应用进行解构与重组,由多粒度服务通过应用程序接口(API)对外发布的后端服务层;以及解耦前后端,提供灵活性和安全性的中间解析层。事实上,这两年常被提及的中台可视为该架构中多粒度服务按应用领域进行的集成。网格与服务架构能够满足提升用户体验和实现业务敏捷的双重目标,支持应用体系的渐进转型,同时能很好地支持开放银行和混合云部署模式。对于业务品种多,处理复杂,面向众多客户与合作伙伴,具有大量传统应用的商业银行,网格与服务架构契合了数字化转型的要求(见图3)。

5、业务价值是数字化转型的唯一目标

商业银行为数字化转型所做的一切努力,最终都要以业务价值创造为落脚点。数字技术创造的业务价值可以由小到大分为三类。

第一类是业务运营模式不变,通过在局部环节、流程或领域采用数字技术实现效率提升或成本节约。用新技术解决特定问题相对容易识别和实施,一段时间后会在整个行业普及,实现全行业经营效率和质量的提升。比如,采用人脸识别技术辅助安全认证,采用OCR(光学字符识别)技术自动识别各类证照和单据,用RPA(机器人流程自动化)技术去手工操作等。

第二类是以数字技术创新方法和模式,实现已有业务经营业绩的显著提升。这类价值创造的难度更大,会带来行业内部竞争能力的此消彼长。比如,以基于大数据的风险管理能力显著降低业务损失或得以开展新的资产业务,通过开放银行进入更多的业务场景触达更多客户群体,通过云模式输出企业财资管理能力增强客户黏性成为主办银行,输出供应链金融平台能力实现线上化的批量获客。数字化转型网szhzxw.cn

第三个层次则是通过创新和颠覆,创造新的业务价值开辟新的收入来源,往往会涉及跨行业的渗透,新的价值链和平台打造。通过算法输出基于大数据的风险评估和定价能力,基于自身积累的大量数据联合外部数据对外提供企业风险评估服务,银行主导整合外部资源构建产业互联网平台等,都属于这类价值创造。数字化转型网szhzxw.cn

三类价值创造有联系也有显著差异。一类价值创造可能是另一类的基础,或者随着量的积累产生质变而上升为另一个层次。第二、三类价值创造关系到银行能否在迈向数字经济的时代进程中抓住机遇求得生存和发展,成为银行之间以及银行业与其他行业之间竞争的主战场。物联网和区块链是在这类竞争中最具潜力的数字技术,而产业互联网的兴起又将带来更多的可能。由此可见,要通过数字化转型取得竞争优势,需要放宽视野,密切跟踪技术的最新发展和应用,研究外部生态和行业的变化和趋势。数字化转型网szhzxw.cn

三、一个真实的故事数字化转型网szhzxw.cn

大致在10年前,支付宝和财富通不断扩大支付业务市场占比,一家国有大行的行长曾经给各家银行写了一封信,倡议各行切断与第三方支付的连接,推进线上支付互通,联合起来夺回属于银行的市场。事实上,支付宝和财富通之所以能够不断扩大业务规模,是客户做出的选择,在互联网电商兴起过程中第三方支付为用户创造了银行未能提供的价值:在日益丰富的线上场景提供安全便利的支付功能,以及快捷的转账服务。可以断言,如果某家银行切断了与支付宝和财富通的连接,客户会选择另外一家支持转账的银行开户,高度同质化的银行卡服务不具有黏性,而第三方支付提供的价值不能舍弃。在当时,银行理性的选择只能是顺势而为,继续保持与第三方支付的合作,同时自我革新,转变为真正以客户为中心、充满活力的创新型组织。

数字时代,牌照和许可保护不了僵化和保守,看似强大的堡垒也会在意想不到的地方被攻破。对于第三方支付,银行经历了瞧不上、看不懂,再到追不上的过程。在数字经济开启的新一轮数字化转型进程中,商业银行仍应对那场过去不久的支付战争进行反思。数字化转型网szhzxw.cn

翻译:

The background of digital transformation of commercial banks数字化转型网szhzxw.cn

With the industrialization of digital technology and the digitalization of traditional industries, the rapid development and wide application of digital technology have gradually changed the operating environment and mode of society and economy. While the consumer Internet is still evolving and the level of e-government continues to improve, the development of industrial Internet and industrial Internet makes the business decisions, production operations and external cooperation of a large number of traditional enterprises become highly digital and intelligent, forming a new economic form of digital economy. Digital economy has three main characteristics: first, data has become a key factor of production to promote economic development; Second, digital infrastructure becomes a new economic infrastructure; Third, demand and supply are increasingly coordinated. Digital economy optimizes the efficiency of resource allocation and significantly reduces the cost of social transactions. Therefore, it has become an economic form of higher quality development.

In 2017, Oxford Economics and Huawei jointly released a research report on the digital economy called Digital Spillover.

According to the analysis of the report, the long-term return of investment in ICT digital technology is 6.7 times that of non-ICT investment. In addition to the industries highly dependent on digital technology such as finance and communication. The compound growth rate of digital technology investment in traditional industries including real estate, agriculture and mining has exceeded 10% since 2000. Meanwhile, it is predicted that by 2025, the global digital economy will account for as much as 24.3 percent. The logic behind these three numbers is clear:. Digital technology has become a major driver of productivity and innovation in companies and industries.

Having witnessed the disruption brought by the Internet in the fields of retail, social networking and financial payment. It may be easier to understand that “digital transformation will be a change related to the survival and development of commercial banks”. Compared with the information construction in the past, in which banks fully control products and delivery. Focus on internal functions and local processes, and take improving efficiency and convenience as the main goal. Digital transformation is under the background of society and economy moving towards the digital age.

A leapfrog evolution of digital technology-driven banking products and services. Customer management, risk control, operational models, and relationships with external partners and ecosystems. The global outbreak of the novel coronavirus pandemic has made commercial banks pay more attention to the Internet and digital technology, increasing the urgency of digital transformation. At the same time, transformation will not happen naturally and achieve success. Banks need to put digital transformation at the core of their strategy. By analyzing the form of future digital economy, banks need to find the right position, determine the goal and path of transformation starting from the end, and promote the implementation with firm execution force.数字化转型网szhzxw.cn

Five focuses of digital transformation of commercial banks数字化转型网szhzxw.cn

Digital transformation requires the entire organization to embrace technology数字化转型网szhzxw.cn

Science and technology are the primary productive forces. Looking back at history, no matter the agricultural revolution brought by cultivation technology. Or the three industrial revolutions brought by steam technology, electric technology, computer and information technology. All of them are epoch-making changes triggered by major technological breakthroughs. Today, the new generation of digital technologies, represented by big data, cloud computing, artificial intelligence. Internet of Things and blockchain, is creating a new era of digital society and digital economy.

With the development of information technology and the popularization of Internet application. Some commercial banks have put forward the strategy of leading by science and technology. Increasing the investment of resources to improve the efficiency and quality of operation by means of science and technology. However, in reality, there are still deviations and misunderstandings in understanding what is “leading by science and technology”. Behind the proposal of science and technology leading strategy is the recognition that science and technology has become the most critical variable to promote the development of banks. Undoubtedly, the understanding of the status promotion for the purpose of salary and the number of cadres. Or the distribution of the right of discourse about who is strong and who has the final say is too biased and narrow.

The connotation of technology leadership is to use digital technology to restructure banks数字化转型网szhzxw.cn

The connotation of technology leadership is to use digital technology to restructure banks. Not only to improve efficiency or reduce costs. But more importantly to realize their own evolution to adapt to the extensive and profound changes in the external environment. Science and technology leadership requires the whole organization to embrace science and technology. And all personnel to form the way of thinking and behavior habits to optimize, change and innovate by means of science and technology. The effective implementation of the strategy of leading science and technology requires the deep integration of science and technology and business, and the two-wheel drive of technology and business.

Technical personnel have an advantage in understanding what problems can be solved by technology. While business personnel have a more comprehensive understanding of financial products, risks and operations. Only through close collaboration, mutual inspiration and promotion can they give full play to the full potential of digital technology to create business value. The implementation of the strategy of leading science and technology also requires that science and technology be more advanced, go deeper into the business planning and decision-making. And share the responsibility of business development with the business.

Agility is a necessary organizational capability for digital transformation数字化转型网szhzxw.cn

At present, what we can see clearly is the direction and general picture of the future development of digital society and digital economy. However, the formation of micro-structure and concrete form of the future is highly uncertain, even beyond our imagination today. Influenced by many factors such as the development of technology itself, the exploration of new business models, the cooperation and competition among many participants, the adjustment of policies and the change of behavior habits, the development of digital society and digital economy is bound to be a process of continuous innovation, trial and error, and iterative evolution. Therefore, the agile ability to sense changes and respond quickly in the unpredictable dynamic environment has become a necessary ability for digital transformation. For commercial banks, agile organization becomes the organizational and institutional guarantee for the integration of technology and business.

There are many drawbacks in traditional banking management mode of science and technology. 数字化转型网szhzxw.cn

On the one hand, centralized management of science and technology resources leads to too much emphasis on unified planning and construction. And it is difficult to optimize technology to match the differences of businesses. A large number of cross-business lines and cross-department coordination makes actions slow. On the other hand, the project-driven system construction mode under the department bank leads to a large number of system islands, data separation and repeated construction. In addition, the line consciousness under the old governance model has invisibly widened the distance between science and technology and business. Digital transformation requires new S&T governance models to build business agility capabilities that incorporate S&T elements (see Figure 1).

In terms of resource allocation

In terms of resource allocation, the R & D team responsible for the construction of channels, products, risks and operational systems related to the business line is assigned to the business line. And the performance indicators are shared with the business personnel. The science and technology leader reports to the president of the business director and the CIO. The rest of the R&D resources are responsible for the middle and background system construction tasks. While providing basic technology platform and shared application support capacity for all R&D teams. Key science and technology functions such as architecture management. Data standards and information security are managed in a unified manner. And all science and technology teams are required to comply with the institutional processes and technical specifications in these areas.

In terms of operation mechanism数字化转型网szhzxw.cn

In terms of operation mechanism, the R&D personnel assigned to the business line work in the office with the business. And the backbone of science and technology participates in daily business planning and business activities, giving more project planning and decision-making rights to the science and technology personnel with business thinking. At the same time, the project-driven system construction mode has changed to the product-driven and operation-driven mode. Which enables science and technology investment to focus more on the delivery of business value.

In terms of R&D mode

In terms of R&D mode, it promotes the transformation from traditional waterfall mode to agile mode. And establishes an organization-level R&D system combining agile method and CMMI practice. With agile methods for fast delivery, CMMI provides a complete organization-level process and framework that enables agile business response while effectively ensuring software quality and controlling risk on large projects.

Data is the core resource of digital transformation

Data has always been vital, and the Internet has played an important role in making society aware of the value of data. The Internet platform promotes the generation and convergence of massive data, and shows amazing value through the use of data. In April 2020, the central government’s first document on market-based allocation of factors listed data as a new type of production factor, alongside land, labor, capital and technology. Indicating that data has become a key factor of production in the digital economy.

The application of data by domestic banks can be roughly divided into three stages. Early attention to limited customer data, account data, accounting data. And financial data of credit customers in order to meet accounting and financial needs. As regulatory requirements change and competition becomes increasingly fierce, banks begin to collect and use more comprehensive business data. In addition to customer analysis and precision marketing, mainly to serve internal refined management. Fund transfer pricing, management accounting, balance sheet and capital management needs. When Internet and technology companies began to penetrate into the financial business field. Along with the increasing maturity and popularity of big data technology. Banks gradually expanded the application of various kinds of external data. With the support of internal and external data. They carried out customer management and risk management in a new mode combining online and offline (see Figure 2).数字化转型网szhzxw.cn

The business of banks revolves around information collection and processing, which naturally has the characteristics of data-driven business.数字化转型网szhzxw.cn

The business of banks revolves around information collection and processing, which naturally has the characteristics of data-driven business. In order to realize digitalization and intelligentization of operation and management. Banks need to make greater efforts in data governance and infrastructure platform construction.

At present, data quality, data island, data security and other problems are still common in the whole industry. Overcoming these obstacles requires data governance as an important foundation to continue to grasp. In addition to the establishment of system, process, standards and norms and other conventional governance work, we should focus on the following work:

First, beyond the technical perspective to establish a business-oriented asset management system. So that business personnel and algorithm engineers to data assets and information of various dimensions at a glance;

The second is to classify the data, and realize the data sharing in the whole bank by clarifying the use rights and establishing efficient approval procedures; 数字化转型网szhzxw.cn

Third, the establishment of integrated data governance platform and tools. Enabling data analysis and system design and development, data governance closed-loop management; 数字化转型网szhzxw.cn

Fourth, we should pay equal attention to awareness education, institutional norms and technical means. And comprehensively strengthen data security and personal information privacy protection.数字化转型网szhzxw.cn

Banks need to establish more powerful data capabilities against leading Internet technology companies.

The technical system dominated by traditional data warehouse, data mart and business intelligence tools cannot support the mining and analysis of all kinds of unstructured and semi-structured data. So banks need to establish more powerful data capabilities against leading Internet technology companies.

First, artificial intelligence (AI) technology is introduced to improve the application ability of data mining with the help of machine learning and deep learning algorithms. Customer marketing and risk management based on big data insight. Security authentication based on facial biometric identification, automated services based on voice recognition. And application scenarios such as license, document and contract text element extraction.

The second is the platform of big data capability, that is. Through the integration and integration of the relevant technical components and frameworks of the big data technology stack. The online and automated complex data processing process can be realized. So that the personnel input can focus on the mining of data business value. And the efficiency and effectiveness of the future normal data analysis can be greatly improved.

Cloud computing is the technical direction of digital transformation数字化转型网szhzxw.cn

In the era of digital economy

In the era of digital economy, various economic entities and ecology. Including commercial banks, have formed extensive digital connections. And financial services have shown significant characteristics of diversification, digitalization and scenario-based. Extreme experience has become the basic requirement for service selection, values and emotions have evolved into influencing factors. And event-based financial needs will become normal. For commercial banks with a certain scale and seeking balanced business development. They need to adopt new technical routes and framework systems to build future-oriented business systems. The mainstream direction of technology and Architecture transformation is Cloud Native and Masa-Mesh App and Service Architecture.

In terms of cloud computing technology system数字化转型网szhzxw.cn

In terms of cloud computing technology system, the infrastructure cloud based on virtualization and container technology is mature and stable. Cloud native is the technology and concept of system construction on the infrastructure cloud. Cloud native implies the trend judgment that future applications will run on the cloud. Whether it is public cloud, private cloud or hybrid cloud. The concept of Cloud Native Computing was formally proposed in 2013. After the establishment of The Cloud Native Computing Foundation (CNCF) in 2015. With the continuous participation of more manufacturers and the implementation of more projects. The cloud native technology system and engineering methods are gradually improved and mature.

Gradually formed a group of de facto industrial standards, leading the development direction of technology. Cloud-native technologies include containers, service grids, microservices, immutable infrastructure, and declarative apis, as well as DevOps tools and processes. Based on the cloud original technology system, a loose-coupled system with good fault tolerance, elastic scalability and easy maintenance can be built, which not only enables enterprises to obtain the agile innovation capability of continuous delivery and rapid response, but also ensures the high availability and security of the system, which is the technical capability only possessed by leading Internet companies in the past. Cloud native is a technical system and engineering method with organic combination of internal elements. Single and local applications cannot achieve comprehensive improvement of capabilities.

In terms of application architecture

In terms of application architecture, Gartner provides the best reference for the new application architecture of banks by refining and summarizing many practices and combining with the latest development of digital technology and application ecology, Grid and Service Architecture (MASA). This is a new three-tier architecture: a variety of front-end application layers developed for different scenarios with experience at the core; With the goal of business agility, the traditional single application is deconstructed and reorganized, and the multi-granularity service is released through the application program interface (API). 数字化转型网szhzxw.cn

And decouple the front and rear ends, providing an intermediate parsing layer for flexibility and security. In fact, the middle desk, which is often referred to in the last two years, can be seen as the integration of multi-grained services by application domain within this architecture. The grid and service architecture can meet the dual goals of improving user experience and achieving business agility, support the incremental transformation of the application architecture, and support open banking and hybrid cloud deployment models. For commercial banks with many business varieties, complex processing, large number of customers and partners, and a large number of traditional applications, grid and service architecture fit the requirements of digital transformation (see Figure 3).

Business value is the only goal of digital transformation

All the efforts made by commercial banks for digital transformation should ultimately focus on business value creation. The business value created by digital technologies can be divided into three categories, from small to large.

The first is the business operation model unchanged, through the use of digital technology in local links, processes or areas to achieve efficiency gains or cost savings. 数字化转型网szhzxw.cn

It is relatively easy to identify and implement new technologies to solve specific problems. After a period of time, it will be popularized in the whole industry and improve the operation efficiency and quality of the whole industry. For example, the use of face recognition technology to assist security authentication, the use of OCR (optical character recognition) technology to automatically identify all kinds of certificates and documents, RPA(robot process automation) technology to manual operation.

The second type is digital technology innovation methods and models, to achieve significant improvement in the operating performance of existing businesses. 数字化转型网szhzxw.cn

This kind of value creation is more difficult and will lead to the loss of competitiveness within the industry. For example, the risk management ability based on big data can significantly reduce business losses or develop new asset business, enter more business scenarios by opening banks to reach more customer groups, export enterprise financial management ability through cloud mode to enhance customer stickiness and become the host bank, export supply chain financial platform ability to achieve online bulk customer acquisition.数字化转型网szhzxw.cn

The third level is to create new business value and open up new revenue sources through innovation and disruption, which often involves cross-industry penetration, new value chain and platform building.

The output of risk assessment and pricing capability based on big data by algorithms, the provision of enterprise risk assessment services by combining external data with a large amount of accumulated data, and the construction of industrial Internet platform dominated by the integration of external resources by banks all belong to this kind of value creation.

The three types of value creation are related but have significant differences. One kind of value creation may be the foundation of another, or it may rise to another level as quantity accumulates to produce qualitative changes. The second and third types of value creation are related to whether banks can seize the opportunity to survive and develop in the process of stepping into the era of digital economy and become the main battlefield of competition among banks and between banking and other industries. The Internet of Things and blockchain are the most promising digital technologies in this kind of competition, and the rise of the industrial Internet will bring more possibilities. Thus, to achieve competitive advantages through digital transformation, we need to broaden our vision, closely track the latest development and application of technology, and study the changes and trends of external ecology and industry.数字化转型网szhzxw.cn

A true story

About 10 years ago, when Alipay and Fortune.com were expanding their market share in payment services, the president of a state-owned bank wrote a letter to all banks, calling for them to cut off their connection with third-party payment, promote online payment interconnection, and join forces to regain the market belonging to banks. In fact, the reason why Alipay and Fortuntong can continuously expand their business scale is the choice made by customers. During the rise of Internet e-commerce, third-party payment has created the value for users that banks have failed to provide: providing secure and convenient payment functions and fast transfer services in increasingly rich online scenarios.

It can be asserted that if a bank cuts off its connection with Alipay and Fortune Connect, customers will choose another bank that supports transfer to open an account. Highly homogeneous bank card services are not sticky, and the value provided by third-party payment cannot be abandoned. At that time, the rational choice for banks was to follow the trend, continue to cooperate with third-party payment, and at the same time, innovate themselves and transform into truly customer-centric, dynamic and innovative organizations.

In the digital age, licences and permits cannot protect rigidity and conservatism, and seemingly strong fortresses can be breached in unexpected places. For third-party payment, banks have gone through the process of not looking at, not understanding, and then unable to catch up. In the process of a new round of digital transformation initiated by the digital economy, commercial banks should still reflect on the payment war of the recent past.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:当代金融家,作者:张斌;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。

{kind=link}