数字化运营是工商银行“数字工行(D-ICBC)”战略的重要组成部分,在下一个五年,在银行业基本完成金融服务线上化建设后,竞争方向必将转向精细化运营,以运营促业务增长——顺应大数据、人工智能的技术发展趋势,各家银行将传统的粗放型、依赖人工的产品营销模型,转型升级为以用户为核心、以线上运营为主、以数据和AI决策替代人工决策为特点的精细化运营体系。基于此背景,工商银行围绕“数字工行”品牌目标打造数字化、智能化的企业级智慧运营管理能力,在传统产品营销的基础上引入数字化运营理念,解决产品与用户需求匹配不精准、产品触达客户反馈流程较长、产品优化方向把控不足等难题,并依托互联网智慧运营管理平台,在数字化运营转型方面迈出了探索的“第一步”。为做好面向业务拓展的运营工作,持续维护好客户关系,提升业务价值,工商银行总结近年来数字化运营探索的经验,形成符合自身业务发展诉求的数字化运营方法论,以此指导各业务线数字化运营的顺利开展,以达到“共享复用、百花齐放”的数字化运营建设效果。数字化转型网www.szhzxw.cn

一、数字化运营方法论研究背景

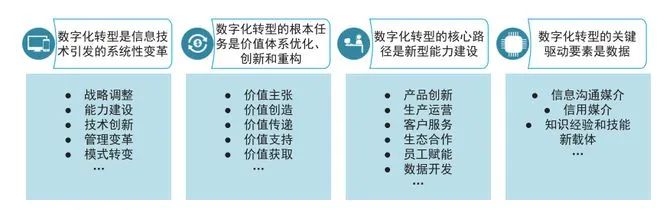

人民银行《金融科技发展规划(2022—2025年)》和银保监会《关于银行业保险业数字化转型的指导意见》均对数字化、营销、运营等内容给出说明与指导意见。工商银行在对上述指导文件中数字化、营销、运营的部分进行梳理和分析后,提炼出四个维度的关键字(如图1所示)。

从图1可以看出,运营与营销都围绕着“人、货、场”这三种银行在经营过程中涉及的核心资源开展工作。

“人”(洞察用户):关注用户的属性识别,了解用户特征与诉求。数字化转型网www.szhzxw.cn

“货”(解决方案):关注银行能够为用户提供的产品、服务、权益等形式。

“场”(经营环境):关注搭建用户参与的交易场景与流程(包括线上和线下)。

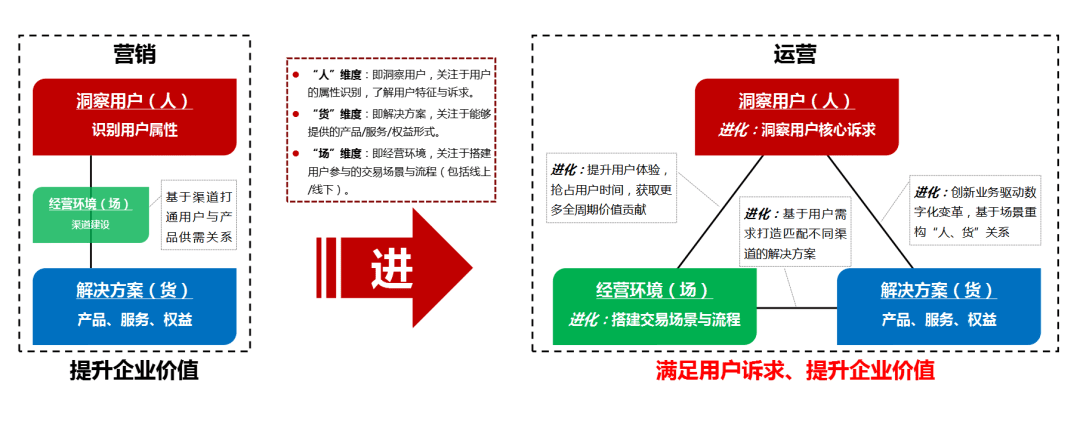

为进一步明确运营与营销的关系与区别,指导数字化运营业务有序开展,工商银行根据在长期经营过程中的探索与实践经验,逐步形成了符合自身发展需要的数字化运营理念(如图2所示):以用户价值为核心,基于以数据为依托的智能化分析方法,聚合银行全部业务能力与经营手段,为用户提供适用于当前经营环境的解决方案,在提升用户认同感的同时达成企业战略目标。

在这一理念的指导下,银行的经营过程可发生以下三点变化:数字化转型网www.szhzxw.cn

一是从单一的“提升企业价值”目标发展为“既满足用户诉求,又提升企业价值”。

二是不再单纯关注用户特征,而是注重分析用户诉求;强调渠道的重要性,并将渠道作为重要一环参与到业务建设中。

三是关注“人、货、场”之间的关系,任意两两关系都可能对业务开展产生影响。

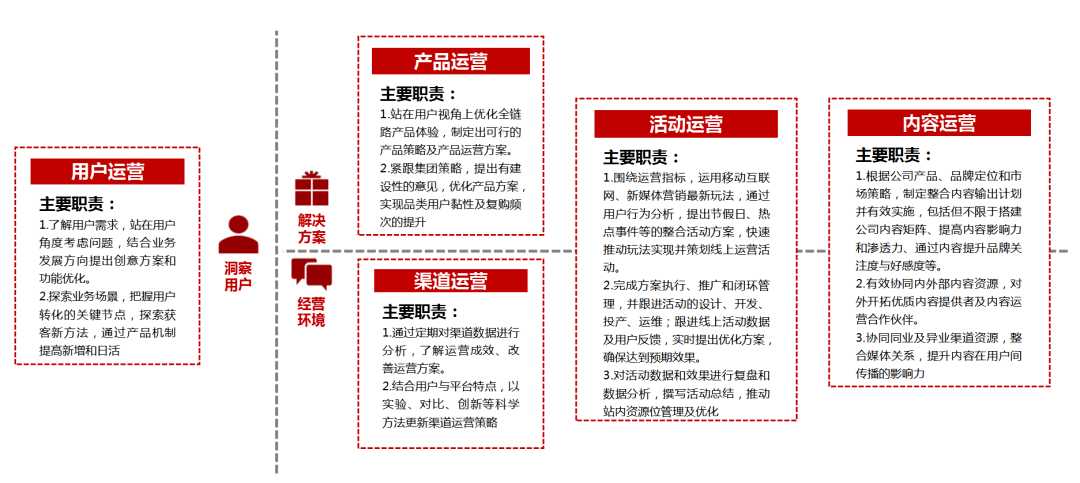

可见,通过数字化运营,用户与银行之间将不再是简单的产品交易及业务办理的关系,而是在满足业务诉求的基础上进一步认同银行理念,与银行相互理解、相互促进的关系。因此,每一种数字化运营的具体业务形式均会围绕着“人、货、场”维度展开,并在其中选择1~2个重点维度进行专项突破。通过概括总结近年来探索性开展的各项数字化运营工作内容,工商银行将数字化运营分为用户运营、渠道运营、产品运营、内容运营、活动运营五大运营形式(如图3所示)。

用户运营:根据运营业务指标的具体要求,通过多种分析模型了解当前用户特征与用户诉求,建立运营指标与“人、货、场”的关联关系,指导其他运营形式顺利开展,一般不独立构成业务场景。

渠道运营:在运营指标指导下将各渠道资源精细化匹配用户诉求。一方面,基于用户特征和全渠道、全场景为用户匹配合适的运营策略,即以“场”为中心的“人、货、场”关系;另一方面,基于埋点、AB测试、专家规则等技术对用户特征进行统一分析,形成统一的运营执行反馈机制。

产品运营:核心目标是提升资产管理规模(AUM),进而进一步提升用户的产品购买率和服务使用率等指标。因此,产品运营通常是在运营指标指导下基于各种方法模型(如漏斗模型)制定运营策略,建立产品与用户、渠道的关系,即以“货”为中心的“人、货、场”关系,满足用户全产品诉求的过程。

内容运营:注重打通用户与渠道、产品之间的社交关系,通过在自有和第三方社区投放用户互动参与内容对“人、货、场”进行优化迭代。

活动运营:是体量最大的运营形式之一,通常需要协同用户运营、渠道运营、产品运营、内容运营等的资源共同建设。相比于其他运营形式,活动运营更为注重对运营过程中“人、货、场”关系的建设、分析与迭代,特别是活动进行中基于用户行为进行数据反馈与策略调整。

通过上述分析可以发现,五大运营形式的主要职责与业务指标不尽相同,如果每一种形式均按独立能力分解落地的思路进行建设,不仅需占用大量的人力、物力资源,而且无法建立“人、货、场”维度之间的关系,未遵循“满足用户诉求、提升企业价值”的数字化运营核心理念,与最初的目标相悖。因此,工商银行需要一套标准的、可复用的、已被实践成果所论证的数字化运营方法论,从统一建设的角度保障上述运营能够正确、高效、快速地开展。

二、数字化运营方法论核心思路数字化转型网www.szhzxw.cn

如果将数字化运营理念中“满足用户诉求、提升企业价值”的描述视为数字化运营的战略目标,那么,“五大运营形式+‘人、货、场’运营资源”则可以看成支撑数字化运营战略目标的具体执行战术手段。在既定运营战略目标与战术手段的基础上,数字化运营方法论的主要目的是打通战略目标与战术手段的关联关系。具体来说,数字化运营对技术能力提出了以下要求:

一是为每一种运营形式提供必要的“人、货、场”运营资源,保障在运营业务落地时能够合理、快速搭建运营业务场景。

二是明确数字化运营理念与运营形式之间的关联关系,保障每一种运营形式都能满足数字化运营的要求。

工商银行对上述每一种运营形式的落地案例进行详细分析后发现,各运营形式在落地过程中都从用户生命周期和用户旅程两个维度分解用户诉求,然后将诉求与“五大运营形式+‘人、货、场’运营资源”进行精准匹配,以此形成工商银行数字化运营策略网。也就是说,无论业务人员以何种形式开展业务运营,数字化运营策略都是围绕“感知—决策—执行”的闭环模式综合展开,系统落地层面可使用一套高度抽象的数字化运营模型匹配上述诉求。工商银行对这套模型进行了建模并命名为数字化运营CJO流程模型(Customer-Journey-Operation Model)(如图4所示)。

在数字化运营CJO流程模型中,各运营形式围绕着“感知—决策—执行”的标准技术流程设计落地方案,通过数据让业务人员了解当前运营业务的开展状况与改进方向。因此,工商银行结合数字化运营中各种运营形式的业务目标与职责描述,以及自身实践成果、银行同业及互联网金融头部企业的先进经验,整理得到工商银行数字化运营核心业务能力(如图5所示)。

具体来说,为实现上述逻辑关系中各系统与平台的主体功能,工商银行数字化运营共计包含以下十点业务能力诉求:数字化转型网www.szhzxw.cn

一是运营策略管理(决策):明确运营目标,将目标拆分成不同的运营指标。在运营指标的指导下明确运营形式,制定运营策略并推送至策略执行方。

二是用户管理(决策):了解用户特征,根据用户特征对用户进行分类管理,形成不同的用户群体。

三是用户反馈(感知、决策):建立用户与企业的交互沟通方式,充分收集、听取用户反馈意见,并通过分析反馈意见明确下一步提升改进点。

四是营销管理(决策、执行):建立产品运营管理机制,提供丰富的产品营销方案,并监测营销执行情况,及时调整方案与形式。

五是权益管理(决策、执行):建立全行用户权益管理机制,对用户权益的创建、发放、使用、核销等进行统筹管理。

六是渠道触达(感知、执行):建立渠道运营体系,向渠道投放各种运营形式,全方位提升渠道运营能力。包括渠道管理、网点管理、消息互动三部分能力诉求。渠道管理主要针对各类用户使用的操作渠道(如手机银行、小程序、第三方App等)进行能力精细化打磨,在对渠道特征充分了解的基础上将用户向自有渠道进行引流;网点管理针对线下网点进行能力精细化打磨,目的是提升网点的友好性与易用性;消息互动针对各类推送消息(短信、邮件、外呼等)进行能力精细化打磨,提升获客引流能力。

七是活动管理(决策、执行):建立活动运营形式管理机制,提供丰富的活动类型与活动方案,并能够监测活动执行情况,及时调整方案与形式。

八是内容平台(决策、执行):建立内容运营形式管理机制,对各种用户互动内容进行整理筛选,并投放到各触客渠道中。

九是数据智能洞察(感知、决策):通过技术手段保障各种运营形式开展过程中的数据采集、数据整理、数据分析与计算过程顺利进行,主要包括数据中台、人工智能技术、AB测试、埋点收集等。

十是数字风控(决策、执行):监测并控制各类运营业务开展过程中的风险。

三、数字化运营方法论实践成果

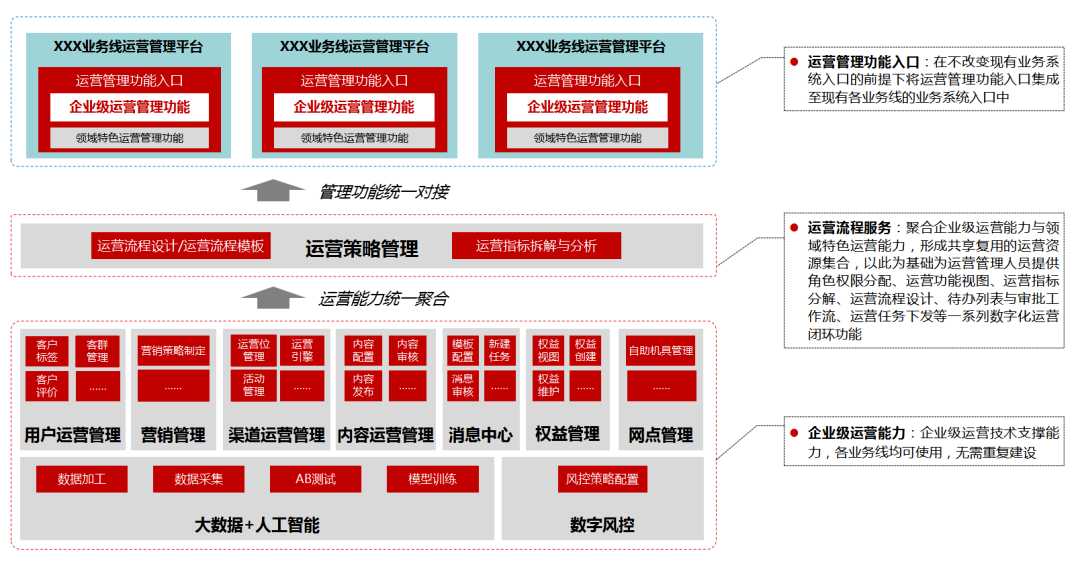

明确了上述十大核心业务能力,工商银行在数字化运营建设过程中积极利用实践成果对方法论进行有效补充与完善。通过对接以用户价值为核心的数字化运营形式,结合应用落地规划以及现有技术能力建设情况,工商银行在满足业务能力诉求的基础上基于数字化运营核心业务能力提炼形成企业级运营支撑能力(如图6所示),包括运营策略管理、用户运营管理、渠道运营管理、内容运营管理、消息中心、网点管理、权益管理、营销管理、“大数据+人工智能”、数字风控十大能力。

在具备支撑能力后,技术侧就需要考虑将运营支撑能力通过管理视图的形式向运营管理业务人员输出,使任一业务线的业务人员都能通过上述能力快速、低成本地开展数字化业务运营工作。为此,工商银行进一步结合数字化运营CJO流程模型、数字化运营各系统及平台逻辑关系结构等方法论内容,设计了符合各业务线数字化运营管理诉求的运营管理能力平台(如图7所示)。数字化转型网www.szhzxw.cn

在这一设计思路指导下建设的数字化运营支撑能力将具有如下优势:

一是聚合企业级/领域级核心运营能力,任何需要开展数字化运营的业务线均可通过聚合的能力复用,使各种形式的运营任务能够快速上线。

二是提供标准的可视化运营管理功能,各业务线运营管理人员可以通过“拖、拉、拽”操作快速设计业务运营流程,制定运营策略,保障运营任务能在短时间内快速配置上线,无需进行功能研发。

三是运营任务流程与用户操作流程完全一致,运营管理人员可直观感受到运营过程中用户发生的数据变化,实时调整运营策略。

四是对各业务系统侵入较小,各业务线投入的研发资源较少,可降低运营成本。

未来,工商银行将在充分利用好已有数字化运营支撑能力及运营管理平台的基础上,基于数字化运营方法论,从线上线下全渠道运营统筹、新技术支撑与企业级数据共享、一站式全流程平台服务等维度,整合现有各板块平台系统功能,进一步打磨各项运营支撑能力及运营管理平台,形成“以用户价值为核心”和“满足用户诉求、提升企业价值”的运营价值流闭环,实现全用户、全产品、全渠道、全旅程、全场景的智能化决策和数字化驱动。

翻译:

Digital operation is an important part of ICBC “Digital Industrial and Commercial Bank (D-ICBC)” strategy. In the next five years, after the banking industry has basically completed the online construction of financial services, the competition direction will shift to fine operation and promote business growth by operation — in line with the technological development trend of big data and artificial intelligence. Various banks have transformed the traditional extensive product marketing model that relies on human resources into a refined operation system that takes user as the core, focuses on online operation, and features data and AI decision-making instead of human decision-making.

Based on this background, Industrial and Commercial Bank of China builds digital and intelligent enterprise-level intelligent operation management ability around the brand goal of “digital ICBC”, introduces digital operation concept on the basis of traditional product marketing, and solves problems such as inaccurate matching between products and user needs, long feedback process of products reaching customers and insufficient control of product optimization direction. And relying on the Internet intelligent operation management platform, in the digital operation transformation has taken the “first step” of exploration. 数字化转型网www.szhzxw.cn

In order to do a good job of business expansion oriented operation, continuously maintain good customer relations, and enhance business value, ICBC summarizes the experience of digital operation exploration in recent years, and forms a digital operation methodology in line with its own business development demands, so as to guide the smooth development of digital operation of all business lines, so as to achieve the digital operation construction effect of “sharing and reuse and blooming of a hundred flowers”.

Research background of digital operation methodology

The Fintech Development Plan (2022-2025) of the People’s Bank of China and the Guiding Opinions on the Digital Transformation of the Banking and Insurance Industries of the China Banking and Insurance Regulatory Commission both give explanations and guiding opinions on digitalization, marketing and operation. After sorting out and analyzing the digitalization, marketing and operation parts of the above guidance documents, ICBC extracted four dimensions of keywords (as shown in Figure 1).

Figure 1 Keywords of digital operation of banks

As can be seen from Figure 1, operation and marketing are carried out around the three core resources involved in the operation of banks, namely “people, goods and fields”.

“People” (insight into users) : focus on user attribute identification and understand user characteristics and demands.

“Goods” (solutions) : focus on the products, services, rights and interests that banks can provide to users.

“Field” (business environment) : Focus on building transaction scenarios and processes (both online and offline) in which users participate.数字化转型网www.szhzxw.cn

In order to further clarify the relationship and difference between operation and marketing and guide the orderly development of digital operation business, ICBC has gradually formed a digital operation concept in line with its own development needs based on its exploration and practical experience in the long-term operation process (as shown in Figure 2) : With the user value as the core and the data-based intelligent analysis method, all the business capabilities and operation means of the bank are aggregated, so as to provide users with solutions suitable for the current business environment and achieve the strategic goals of the enterprise while enhancing the user identity.

Figure 2 Connotation of digital operation concept of ICBC

Under the guidance of this concept, the operation process of banks can undergo the following three changes:

The first is to develop from the single goal of “improving enterprise value” to “satisfying user demands and improving enterprise value”.

Second, it no longer focuses on user characteristics, but pays attention to the analysis of user demands; Emphasize the importance of channel, and channel as an important link to participate in business construction.

The third is to pay attention to the relationship between “people, goods and field”, any two relationships may have an impact on business development.

It can be seen that through digital operation, the relationship between users and banks will no longer be simple product transaction and business handling, but further identify with the bank concept on the basis of satisfying business demands, and have a mutual understanding and promotion relationship with the bank. Therefore, each specific business form of digital operation will be developed around the dimension of “people, goods and field”, and one or two key dimensions will be selected for special breakthrough. By summarizing the contents of various exploratory digital operations in recent years, ICBC classifies digital operations into five operating forms: user operation, channel operation, product operation, content operation and activity operation (as shown in Figure 3).

Figure 3 Forms of digital operations

User operation: According to the specific requirements of operation business indicators, it understands the current user characteristics and user demands through a variety of analysis models, establishes the correlation between operation indicators and “people, goods and fields”, and guides the smooth development of other operation forms. Generally, it does not constitute business scenarios independently.

Channel operation: Under the guidance of operational indicators, channel resources are refined to match users’ demands.

On the one hand, based on user characteristics, all-channel and all-scene, appropriate operation strategies are matched for users, namely, the relationship between “people, goods and fields” centered on “fields”. On the other hand, based on buried points, AB testing, expert rules and other technologies, unified analysis of user characteristics is conducted to form a unified operation and execution feedback mechanism.

Product operation: The core goal is to increase the asset management scale (AUM), and further increase the product purchase rate and service utilization rate of users. Therefore, product operation is usually a process of formulating operation strategies based on various method models (such as funnel model) under the guidance of operation indicators, establishing the relationship between products, users and channels, namely the relationship between “people, goods and fields” centered on “goods”, and satisfying users’ demands for the whole product.

Content operation: Pay attention to opening up the social relationship between users, channels and products, and optimize and iterate “people, goods and fields” by releasing interactive and participatory content of users in self-owned and third-party communities.

Activity operation: as one of the largest operation forms, it usually needs to cooperate with the resources of user operation, channel operation, product operation and content operation. 数字化转型网www.szhzxw.cn

Compared with other forms of operation, activity operation pays more attention to the construction, analysis and iteration of the relationship between “people, goods and field” in the operation process, especially the data feedback and strategy adjustment based on user behavior in the process of activity.

Through the above analysis, it can be found that the main responsibilities and business indicators of the five operation forms are not the same. If each form is constructed according to the idea of independent capability decomposition. It will not only occupy a lot of human and material resources. But also fail to establish the relationship among the dimensions of “people, goods and field”. It does not follow the core concept of digital operation of “satisfying user demands and enhancing enterprise value”. Which is contrary to the original goal. Therefore, ICBC needs a set of standard, reusable digital operation methodology that has been demonstrated by practical results to ensure that the above operations can be carried out correctly, efficiently and quickly from the perspective of unified construction.

Core ideas of digital operation methodology

If the description of “satisfying user demands and enhancing enterprise value” in the concept of digital operation is regarded as the strategic goal of digital operation, then “five operational forms + operation resources of” people. Goods and fields “can be regarded as the specific execution tactics to support the strategic goal of digital operation. On the basis of established operational strategic objectives and tactical means. The main purpose of digital operation methodology is to break through the correlation between strategic objectives and tactical means. Specifically, digital operations require the following technical capabilities:

The first is to provide necessary operation resources of “people, goods and fields” for each operation form. So as to ensure reasonable and rapid establishment of operation business scenarios when the operation business is landed.

The second is to clarify the correlation between digital operation concept and operation form to ensure that each operation form can meet the requirements of digital operation.

After a detailed analysis of the landing cases of each of the above operation forms

After a detailed analysis of the landing cases of each of the above operation forms. ICBC found that in the landing process of each operation form, user demands were decomposed from the two dimensions of user life cycle and user journey. And then the demands were accurately matched with the “five operation forms +” operation resources of people, goods and fields “. So as to form the digital operation strategy network of ICBC. That is to say, no matter in what form business personnel carry out business operations. The digital operation strategy is comprehensively developed around the closed-loop mode of “perception — decision — execution”. And a set of highly abstract digital operation model can be used to match the above demands at the system implementation level. Icbc modeled this Model and named it as the digital Operation CJO Process Model (Customer-Journey-Operation Model) (as shown in Figure 4).

Figure 4 CJO process model of digital operation

In the digital operation CJO process model, each operation form focuses on the standard technical process of “perception — decision — execution” to design the implementation scheme. Through the data, the business personnel can understand the development status and improvement direction of the current operation business. Therefore, ICBC integrates the business objectives and responsibility descriptions of various operational forms in digital operation. As well as its own practical results, advanced experience of its peers and leading Internet finance enterprises. And sorts out the core business capabilities of digital operation of ICBC (as shown in Figure 5).数字化转型网www.szhzxw.cn

Figure 5 Core business capability of digital operation of ICBC

To be specific, in order to realize the main function of each system and platform in the above logical relationship, ICBC digital operation includes the following ten business capability demands:

First, operation strategy management (decision-making) : clearly define the operation objectives, and divide the objectives into different operating indicators. Under the guidance of operational indicators, define operational forms, formulate operational strategies and push them to the strategy implementer.

The second is user management (decision) :. Understand the user characteristics, according to the characteristics of the user classification management, the formation of different user groups.

Third, user feedback (perception and decision) :. Establish interactive communication between users and enterprises, fully collect and listen to user feedback. And determine the next improvement point through analysis of feedback.

Fourth, marketing management (decision-making and implementation) :. Establish product operation management mechanism, provide rich product marketing programs, monitor marketing implementation, and timely adjust the programs and forms.

Fifth, rights and interests management (decision-making and implementation) :. Establish a user rights and interests management mechanism for the whole bank. And make overall management of the creation, issuance, use and verification of user rights and interests.

Sixth, channel access (perception and execution) :

Establish channel operation system, put various operation forms into channels, and comprehensively improve channel operation ability. Including channel management, network management, information interaction three parts of the ability to appeal. Channel management is mainly for the operation channels used by all kinds of users (such as mobile banking, small programs, third-party apps, etc.) to refine the ability. On the basis of a full understanding of channel characteristics to divert users to their own channels. Network management refined the ability of offline network, aiming at improving the friendliness and usability of the network. The ability of message interaction is refined for all kinds of push messages (SMS, email, outbound call, etc.) to improve the ability to attract customers.

Seventh, activity management (decision-making and implementation) :. Establish an activity operation form management mechanism, provide a wealth of activity types and programs. Monitor the implementation of activities, and timely adjust the program and form.

Eighth, content platform (decision-making and implementation) :. Establish a content operation form management mechanism, sort out and screen various user interaction contents. And put them into various customer contact channels.

Ninth, intelligent data insight (perception and decision) :. Ensure the smooth progress of data acquisition, data sorting, data analysis and calculation in various forms of operation through technical means. Mainly including data center desk, artificial intelligence technology, AB testing, buried point collection, etc.

The tenth is digital risk control (decision-making and execution) : monitoring and controlling risks in the development of various operational businesses.

Practical results of digital operation methodology

Having identified the above ten core business capabilities, ICBC actively utilized practical results in the process of digital operation construction to effectively supplement and improve the methodology. By connecting with the digital operation form with user value as the core. Combined with the application implementation planning and existing technical capacity building. ICBC has formed enterprise-level operation support capability based on the extraction of core digital operation capability on the basis of satisfying business capability demands (as shown in Figure 6). Including operation strategy management, user operation management, channel operation management, content operation management, message center, network management, rights management, marketing management. “Big data + artificial intelligence”, digital risk control ten capabilities.数字化转型网www.szhzxw.cn

Figure 6 Enterprise-level operation support capability of ICBC

After having the support capability, the technical side needs to consider the output of the operation support capability to the operation management business personnel in the form of management view, so that the business personnel of any line of business can carry out the digital business operation quickly and cheaply through the above capability. Therefore, ICBC further combined the CJO process model of digital operation. Logical relationship structure of each system and platform of digital operation and other methodological contents to design an operation management capability platform that meets the demands of digital operation management of each business line (as shown in Figure 7).

Figure 7 Operation management ability platform of ICBC

The digital operation support capacity built under the guidance of this design idea will have the following advantages:

One is the aggregation of enterprise-level/domain-level core operational capabilities. Any business line that needs to carry out digital operations can be reused through the aggregation capabilities. So that various forms of operational tasks can be quickly online.

The second is to provide standard visual operation management functions. The operation management personnel of each business line can quickly design the business operation process and formulate the operation strategy through the “drag, pull and drag” operation, so as to ensure that the operation tasks can be quickly configured and launched in a short time without the need for functional research and development.

Thirdly, the operation task process is completely consistent with the user operation process. The operation management personnel can intuitively feel the data changes occurring in the operation process and adjust the operation strategy in real time.

Fourth, the intrusion into each business system is smaller. And the R&D resources invested in each business line are less, which can reduce the operating cost.数字化转型网www.szhzxw.cn

In the future, on the basis of making full use of the existing digital operation support capability and operation management platform, based on the digital operation methodology, ICBC will integrate the functions of the existing platform system of various sectors from the aspects of online and offline omni-channel operation coordination. New technology support and enterprise-level data sharing, one-stop whole process platform service, etc. Further refine various operation support capabilities and operation management platforms. Form a closed loop of operation value stream that “takes user value as the core” and “meets user demands and enhances enterprise value”. And realize intelligent decision-making and digital driving of all users, all products, all channels, all journeys and all scenes.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:中国金融电脑;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。