一、世界正在发生变化

1973年的第一次能源危机至今已过去了半个世纪,世界能源格局已经历了多轮重塑,不断发生着深刻变化。诞生于1952年的《世界能源统计年鉴》,就是为世界能源市场提供优质、客观且全球标准化的数据。近年来,在地缘政治浩劫、气候变化、汇率波动、导致能源消费量激增等多重因素影响下,全球能源安全不确定性依然存在。全球能源系统正在面临着近50年以来最严峻的挑战,燃料短缺、企业倒闭、经济运行放缓等负面连锁反应严重损害了全球健康与福祉,迫使相关国家和世界组织调整能源政策。《世界能源统计年鉴》总结了全球能源状况,包括各国及地区能源供求情况、能源结构、使用、变化趋势以及能源投资的相关数据和趋势,可以帮助政府、机构及企业了解全球能源状况,从而更好地制定政策、调整供求关系。它还能够帮助发展中国家制定更加实用的能源政策,推动可持续发展。到今天,《世界能源统计年鉴》已成为媒体、学术界、各国政府和能源企业的必备参考年鉴是能源经济学领域内广受推崇且具权威性的出版物之一。 数字化转型网www.szhzxw.cn

就在今年,毕马威有幸成为能源研究院的合作伙伴,参与发布了第72版《世界能源统计年鉴》,并且首次将该年鉴编译成中文。《世界能源统计年鉴》提供2022年完整的全球能源数据,以能源系统适应不断升级的地缘政治和环境危机的高端视角,分析了全球市场对推动能源转型加快步伐,提供清洁、负担得起和安全的能源的前所未有的强力需求。

二、主要内容

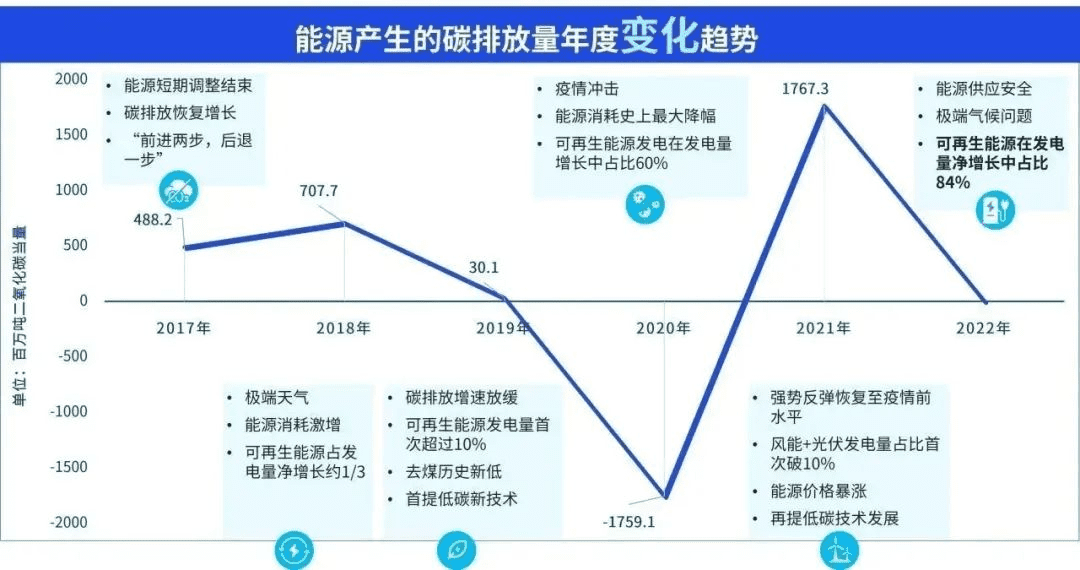

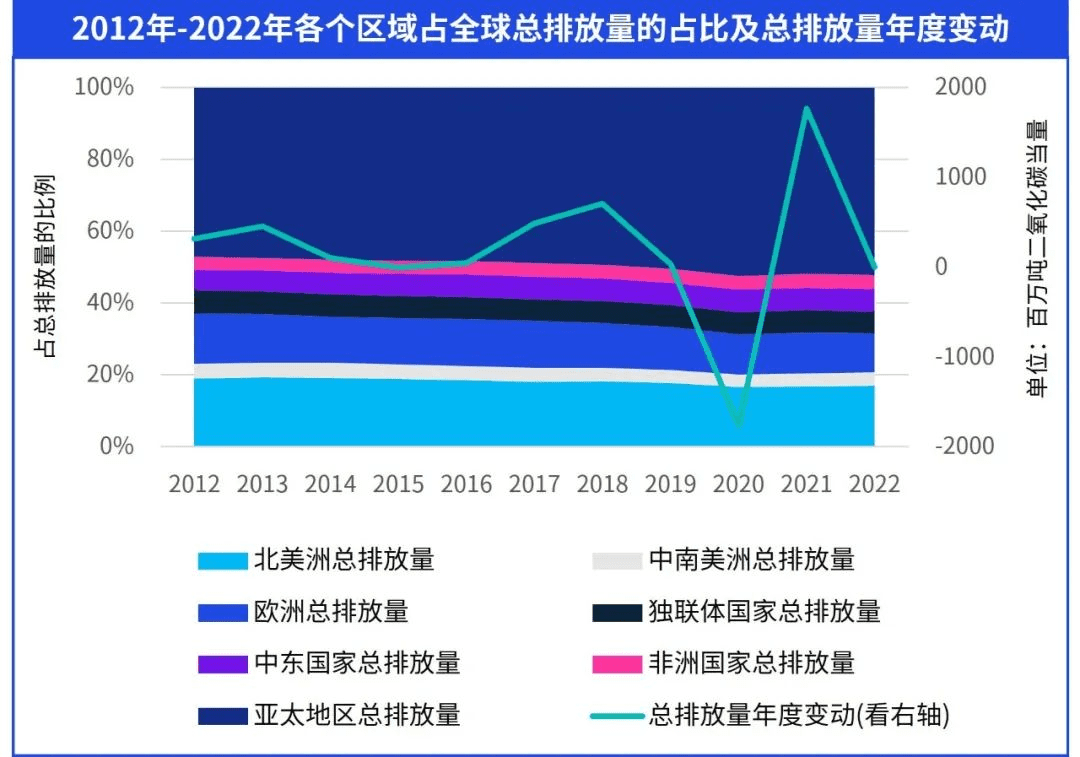

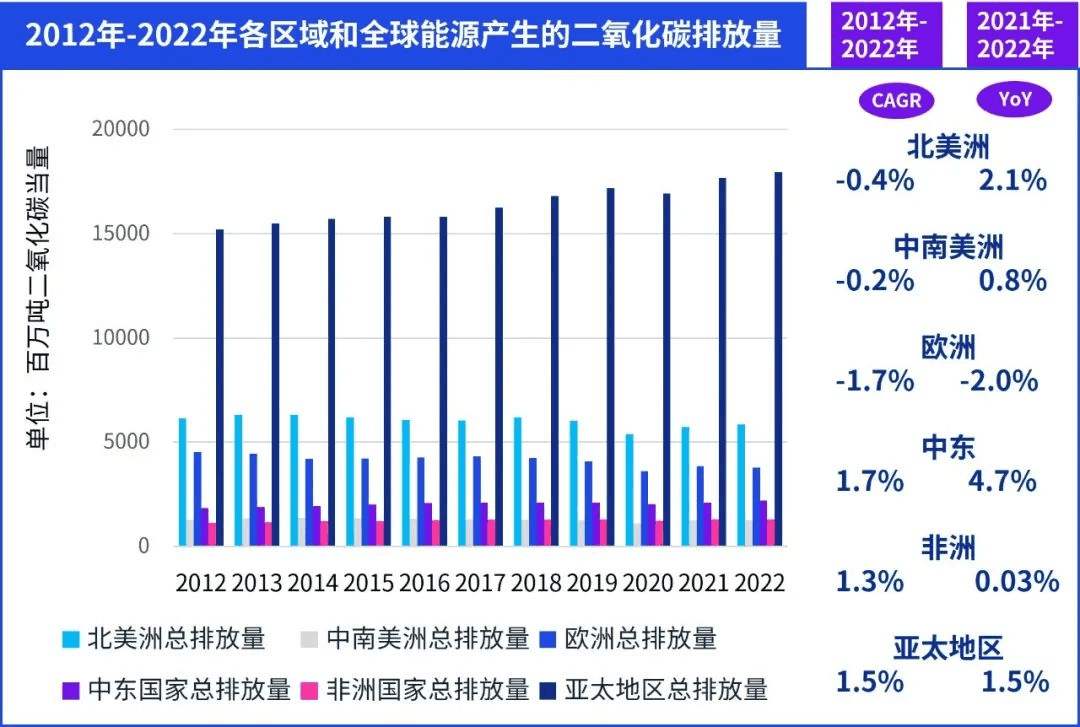

2022年产生的二氧化碳排放量(以二氧化碳当量计) 增长了0.8%。其中,亚太区在全球碳排放中占比增加,中国大陆在2022年碳排放量小幅回落0.1%。与2019年疫情前的水平相比,非经合组织国家占增量的大部分,一次能源消费量增长了20.5艾焦。经合组织国家的一次能源需求与2019年的水平相比略有下降。2022年欧洲碳排放量仍然延续下降。 数字化转型网www.szhzxw.cn

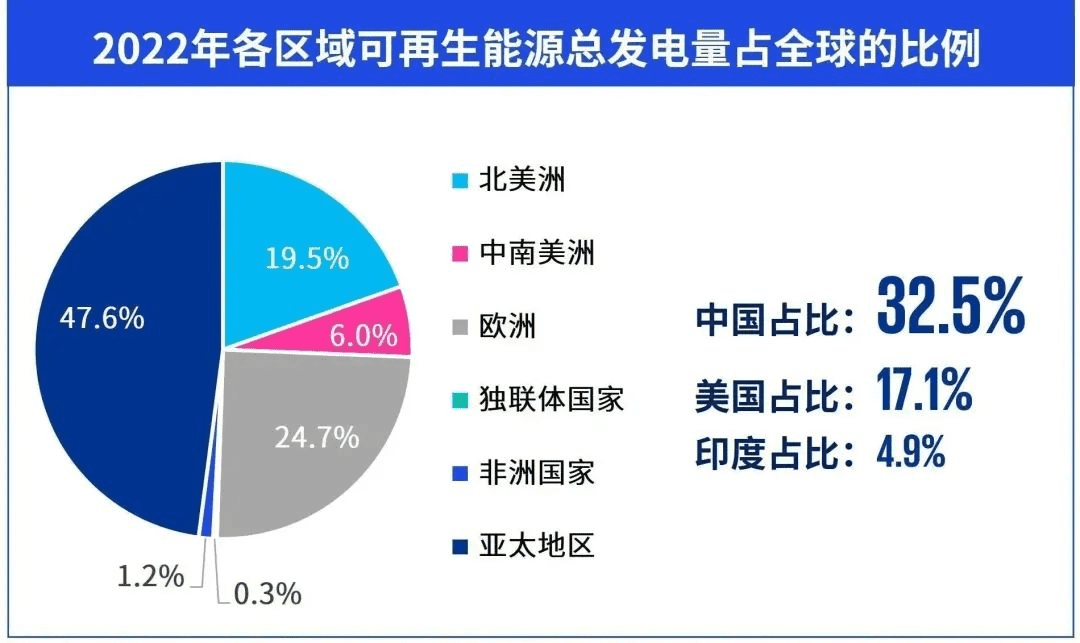

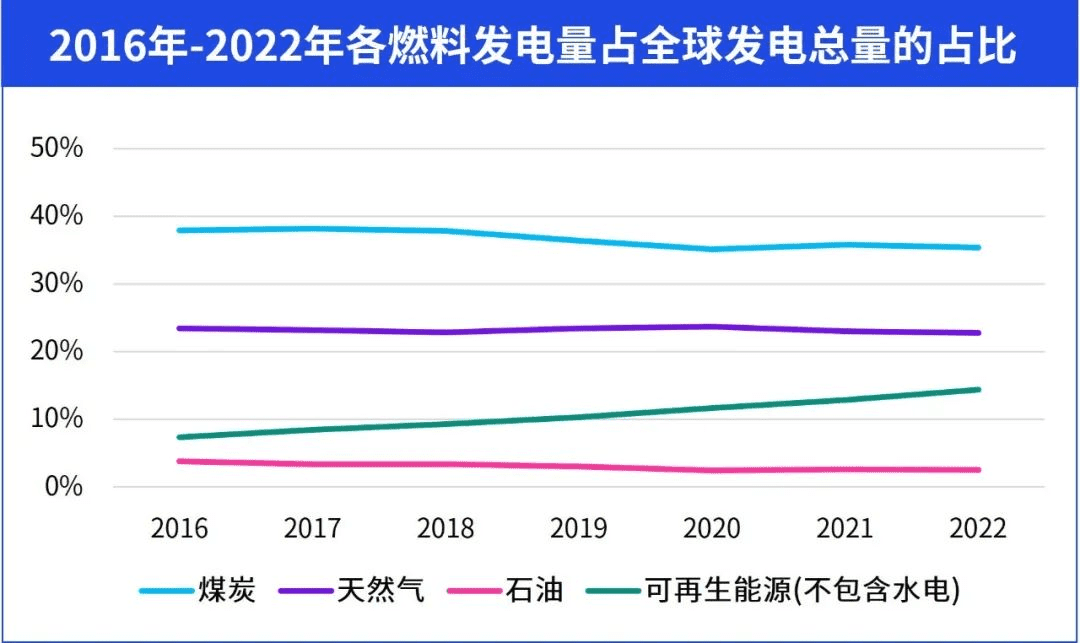

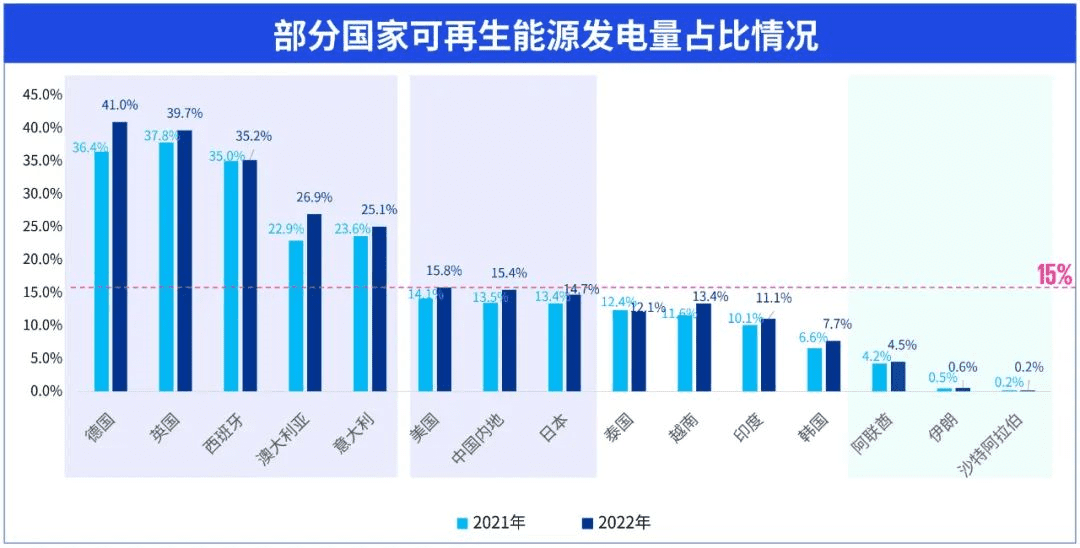

数据显示,2022年全球发电量增长2.3%,但至今煤炭仍是主要发电燃料。美国的风能和太阳能发电量增长势头迅猛,能源机构和战略也在持续调整优化。就2022年来说,美国可再生能源发电量已超过煤电发电量,中国的可再生能源发展速度同样保持较快趋势,可再生能源发电量较上年提高1.7个百分点,其在保障能源供应方面发挥的作用越来越明显。而目前印度由于处于GDP快速增长期,2022年,印度电力供应中燃煤发电占比仍超过70%,对煤炭的依赖更是有增无减。

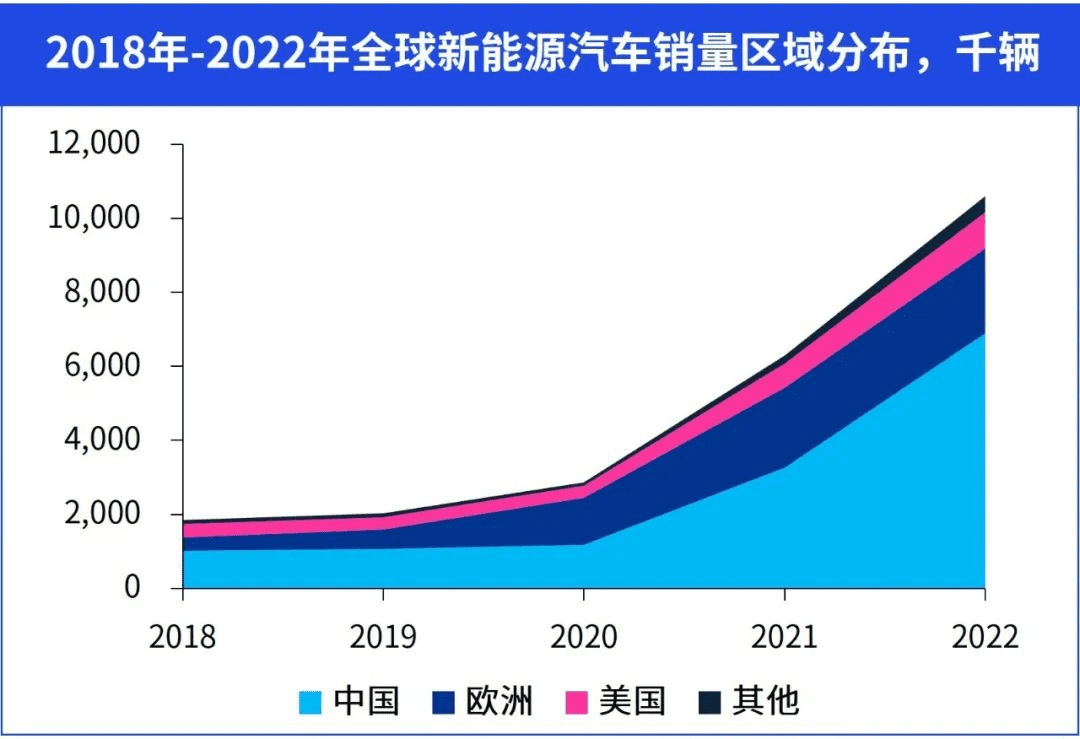

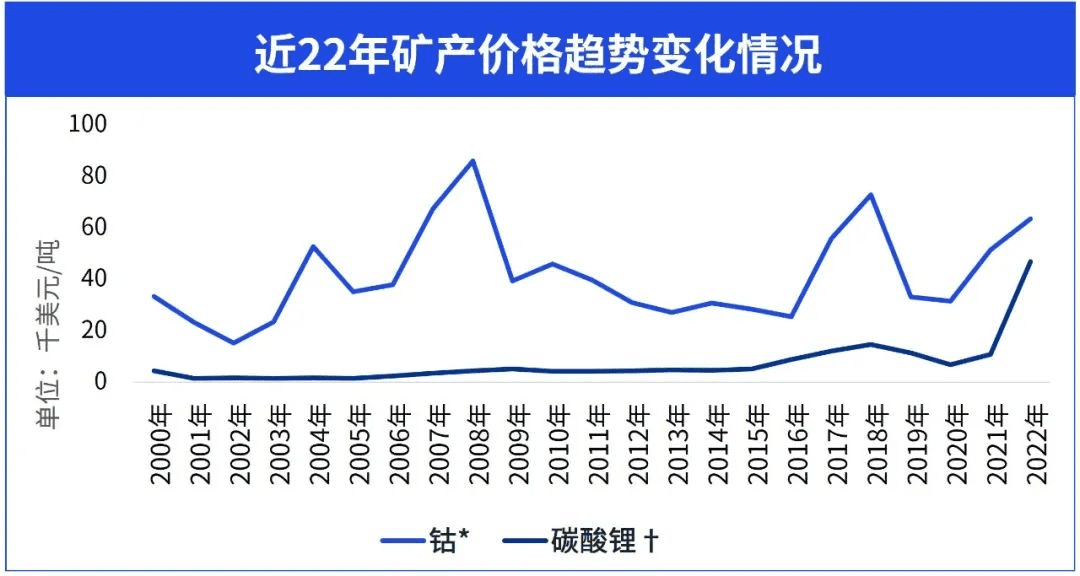

2022年,全球新能源汽车销售量区域分布,中国占比最大。碳酸锂价格上涨335%,均价创下47,000美元/吨的历史新高。同样,钴价2021年上涨了24%,均价达到64,000美元/吨。

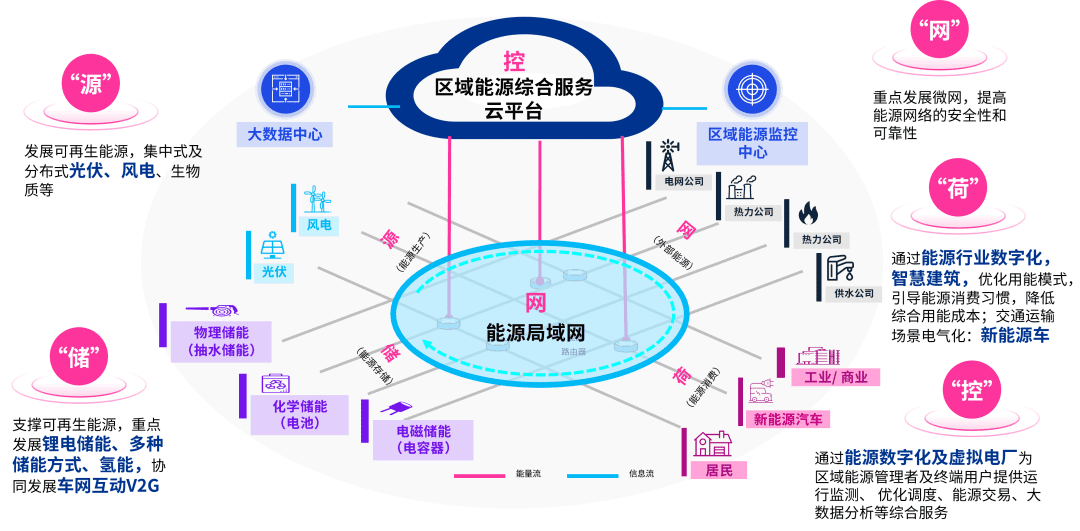

三、能源转型“向新而变” 产业升级“向绿而行”

(一)从“源-网-荷-储-控”多方面推进新型能源体系建设:

开展常规能源、新能源、分布式能源等多能互补,高效、互动、融合的智慧能源体系。本着高端化、绿色化和集约化的思路,由“源-网-荷-储-控”五部分推进。

(二)新型储能整体发展确定性强,国内储能经济性逐步验证中,锂电储能供需待关注:

新型储能经历三年快速发展后,2023年出现短期海外市场增速放缓,一方面受欧洲户储库存积压影响,另外美国表前储能并网缓慢也影响储能系统发货。供给方面,2020-2023年锂电池及上游材料投资扩产规划迅速,需关注实际产能投建,供需关系变化。商业模式上,海外储能率先实现经济性,国内部分独立储能电站、工商业储能项目初具经济性,各地政策及商业模式仍有待持续探索。差异化海外储能、工商业储能,以及液流、钠离子储能及材料是近期重点关注领域。 数字化转型网www.szhzxw.cn

(三)氢能是脱碳的重要方式,各国差异化布局氢产业链,国内技术有待突破:

随着绿氢技术、工业低碳技术的突破,氢产业链降本,碳交易市场有序推进,将极大推动氢能在交通、储能、工业的广泛应用。各国纷纷加码布局氢能,布局方向各有侧重:欧洲全产业链布局,发挥欧盟优势形成跨国氢能集群,德国、英国技术领先。亚太地区,日本着力氢储运存及下游燃料氨应用;澳洲大规模建设绿氢设施,计划成为主要氢出口国;同时,中东、中亚等地区2023年也加速绿氢建设。中国则进行全产业链布局,中短期内中国绿氢制备及燃料电池材料研发能力有待提升。 数字化转型网www.szhzxw.cn

四、总结

为了实现碳达峰和碳中和的目标,能源企业的参与至关重要。过去71年,《世界能源统计年鉴》为各国的能源企业提供了能源最新动态,为能源企业的未来投资方向提供帮助。今年,《统计年鉴》以高层次视角,审视了全球能源系统、全球能源市场在压力之下的表现以及能源转型进展,前所未有地深入洞察能源系统如何适应不断恶化的环境和地缘政治危机,数据可以为企业揭示能源行业在危机之下的境况。

英文翻译:

First, the world is changing

Half a century has passed since the first energy crisis in 1973. And the world energy pattern has undergone several rounds of reshaping and has been undergoing profound changes. The Statistical Yearbook of World Energy was created in 1952 to provide high-quality, objective and globally standardized data on the world’s energy markets. In recent years, under the influence of multiple factors such as geopolitical havoc, climate change, exchange rate fluctuations. And surging energy consumption, global energy security uncertainties still exist.

The global energy system is facing its most serious challenge in nearly 50 years, with negative chain reactions such as fuel shortages, business closures and economic slowdowns taking a toll on global health and well-being, forcing countries and world organizations to adjust their energy policies. The World Energy Statistical Yearbook summarizes the global energy situation, including national and regional energy supply and demand, energy structure, use, change trends and energy investment related data and trends, which can help governments, institutions and enterprises to understand the global energy situation, so as to better formulate policies and adjust the supply and demand relationship.

It can also help developing countries develop more practical energy policies and promote sustainable development.

Today, the Statistical Yearbook of World Energy has become a must-have reference for the media, academia, governments and energy companies. And is one of the most respected and authoritative publications in the field of energy economics.数字化转型网www.szhzxw.cn

Just this year, KPMG was fortunate to partner with the Energy Institute to launch the 72nd edition of the Statistical Yearbook of World Energy, which was translated into Chinese for the first time. The Statistical Review of World Energy provides complete global energy data for 2022 with a high-end perspective of energy systems adapting to escalating geopolitical and environmental crises, analyzing the global market’s unprecedented demand to accelerate the energy transition and provide clean, affordable and secure energy.

Main contents

Co2 emissions produced in 2022 (in CO2 equivalent terms) increased by 0.8%. Compared to pre-pandemic levels in 2019, non-OECD countries accounted for most of the increase. With primary energy consumption increasing by 20.5 exajoules. Primary energy demand in OECD countries declined slightly compared to 2019 levels. Europe’s carbon emissions will continue to decline in 2022.

According to the data, global power generation will increase by 2.3% in 2022. But coal is still the main fuel for power generation. Wind and solar power generation in the United States is growing rapidly. And energy institutions and strategies continue to adjust and optimize. In terms of 2022, the United States renewable energy generation has exceeded coal power generation. China’s renewable energy development speed also maintained a faster trend, renewable energy generation increased 1.7 percentage points over the previous year. Its role in ensuring energy supply is becoming more and more obvious. At present, India is in a period of rapid GDP growth. And in 2022, coal-fired power generation in India’s power supply will still account for more than 70%, and its dependence on coal is increasing.

In 2022, the global sales volume of new energy vehicles will be distributed regionally, with China accounting for the largest proportion. Lithium carbonate prices rose 335% to a record high average price of $47,000 / ton. Similarly, cobalt prices rose 24% in 2021 to an average of $64,000 per ton.

Third, energy transformation “to the new and change” industrial upgrading “to green”

(1) from the “source – network – load – storage – control” to promote the construction of a new energy system:

We will develop an efficient, interactive and integrated smart energy system featuring multi-energy complementarity, such as conventional energy, new energy and distributed energy. In line with high-end, green and intensive ideas, by the “source – network – load – storage – control” five parts to promote.

(2) The overall development of new energy storage has a strong certainty, and in the gradual verification of domestic energy storage economy, the supply and demand of lithium energy storage should be paid attention to:

After three years of rapid development of new energy storage, short-term overseas market growth slowed down in 2023. On the one hand, affected by the backlog of European household storage inventory. And the slow grid connection of pre-table energy storage in the United States also affects the delivery of energy storage systems. On the supply side, 2020-2023 lithium battery and upstream material investment expansion planning is rapid, need to pay attention to the actual capacity investment. And construction, the relationship between supply and demand changes.

In terms of business model, overseas energy storage has taken the lead in achieving economy, while some independent energy storage power stations and industrial and commercial energy storage projects in China have begun to be economical, and local policies and business models still need to be continuously explored. Differentiated overseas energy storage, industrial and commercial energy storage, as well as liquid flow, sodium ion energy storage and materials are the focus areas in the near future.

(3) Hydrogen energy is an important way to decarbonize, countries differentiated layout of hydrogen industry chain, domestic technology to be broken:

With the breakthrough of green hydrogen technology and industrial low-carbon technology, the cost of hydrogen industry chain will be reduced. And the orderly promotion of carbon trading market will greatly promote the wide application of hydrogen energy in transportation, energy storage and industry. Countries have increased the layout of hydrogen energy, and the layout direction has its own focus. The layout of the whole industrial chain in Europe, giving play to the advantages of the EU to form transnational hydrogen energy clusters, and Germany and the UK are leading technology.

In the Asia-Pacific region, Japan focuses on hydrogen storage and storage and downstream fuel ammonia applications. Australia is building green hydrogen facilities on a large scale and plans to become a major hydrogen exporter. At the same time, the Middle East, Central Asia. And other regions will also accelerate the construction of green hydrogen in 2023. China has carried out the layout of the whole industrial chain, and China’s green hydrogen preparation and fuel cell material research. And development capabilities need to be improved in the short and medium term.

Summary

In order to achieve the goal of carbon peak and carbon neutrality, the involvement of energy companies is essential. For the past 71 years, the Statistical Review of World Energy has provided energy companies in each country with the latest developments in energy and helped energy companies to invest in the future. This year, the Statistical Yearbook takes a high-level look at the global energy system, the performance of global energy markets under stress, and the progress of the energy transition, providing unprecedented insight into how the energy system is adapting to a deteriorating environment and geopolitical crisis, data that can reveal how the energy industry is faltering under crisis.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源于 毕马威KPMG ;编辑/翻译:数字化转型网小汤圆。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。