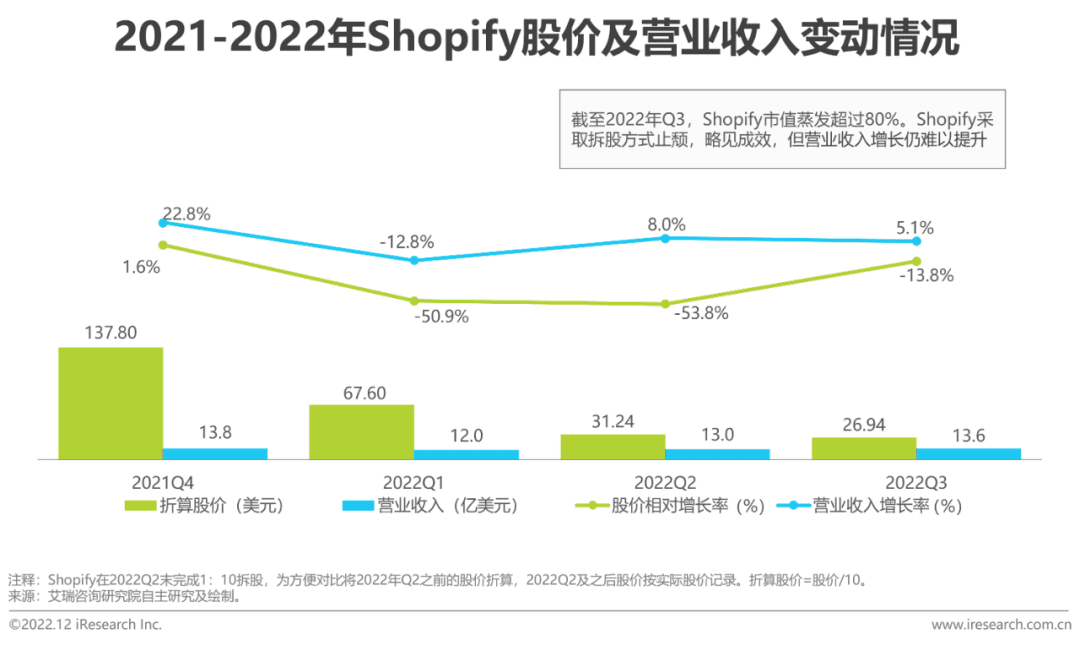

核心摘要:

中国SaaS市场的发展与全球市场进程不可分割而语,全球范围内SaaS行业的发展速度近一年有所放缓,美国SaaS巨头遭遇增长乏力、业绩亏损、股价低迷等问题。但新兴国家也有新的厂商逆势而为,如快速崛起的印度市场。对中国企业而言,境外上市不再是必胜打法,深耕国内企业数字化转型需求才是面对竞争的必修课。数字化转型网www.szhzxw.cn

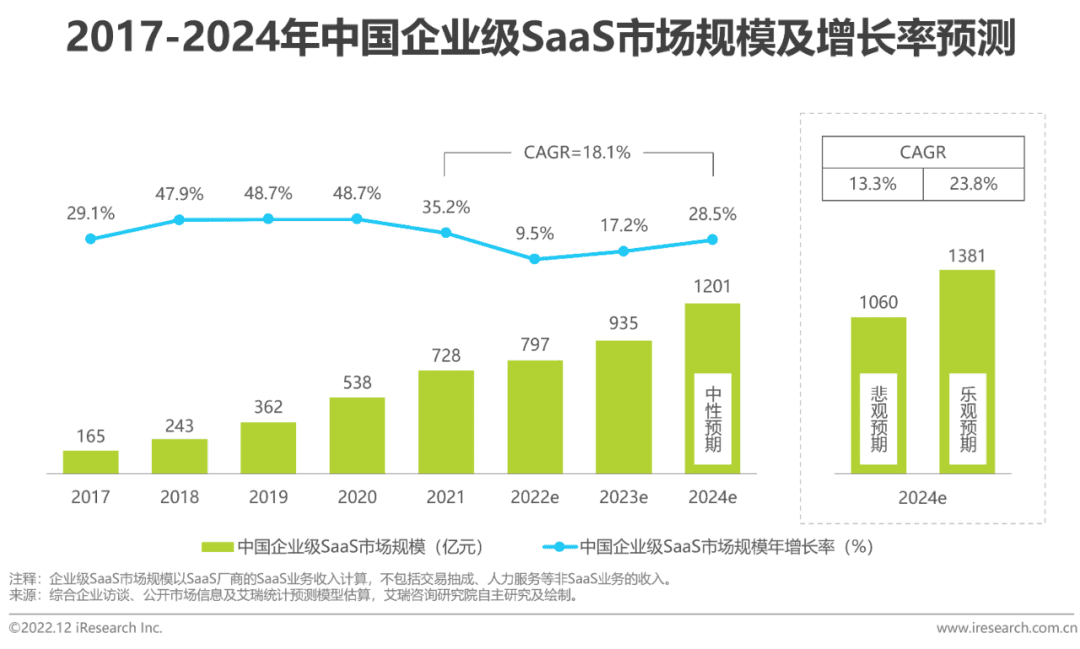

2021年中国企业级SaaS市场规模为728亿元,同比增速由2020年的48.7%下降到35.2%,相比于疫情爆发之初的乐观预期,目前认为宏观经济下行带来了更大的压力,企业SaaS总需求收缩将使得行业增速大幅下滑,预计2022年,SaaS行业的增速将首次下滑至10%以下。未来三年SaaS行业的增长也将与宏观经济恢复速度相挂钩,在中性预期下,到2024年中国企业级SaaS市场规模将有望达到1201亿元,2021-2024年的年复合增长率为18.1%。

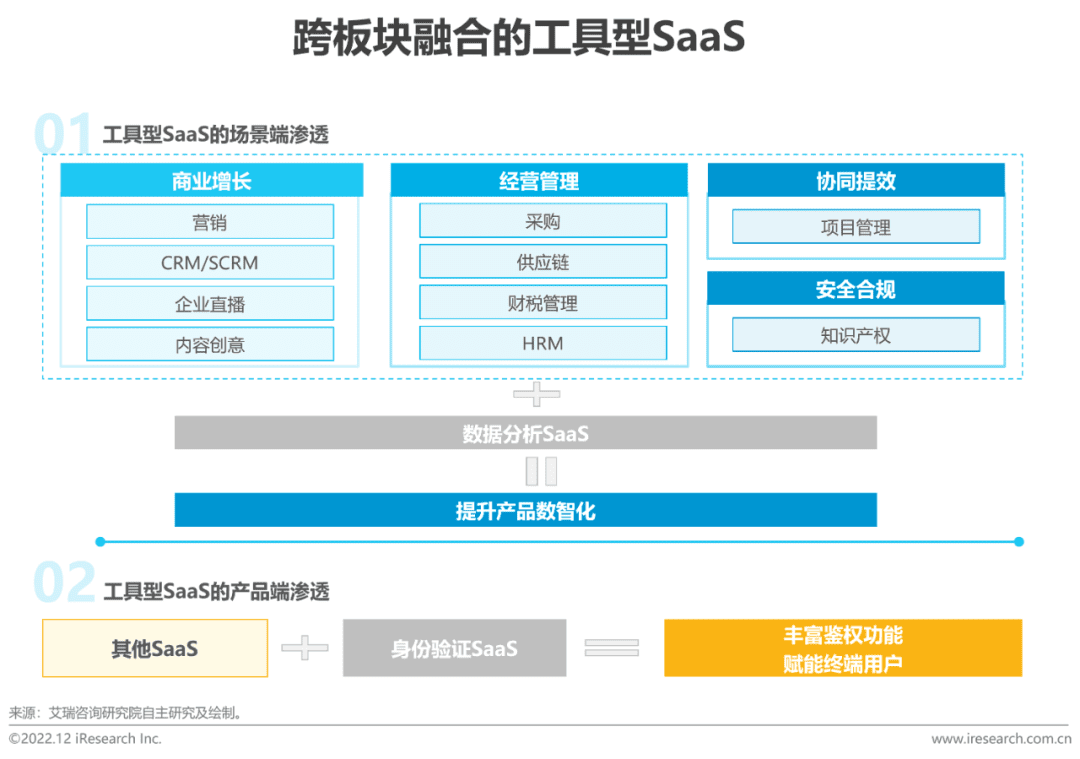

随着业务的深入和服务经验的积累,部分赛道的SaaS产品边界变得愈发模糊,SaaS厂商开始尝试同时布局多条产品线,拉通服务链路。商业增长SaaS厂商开始向营销和CRM拓展业务布局,财税与HRM赛道逐渐成熟,厂商由点及面加速一体化布局,工具型SaaS横向渗透并融合特定业务场景来发挥自身价值。

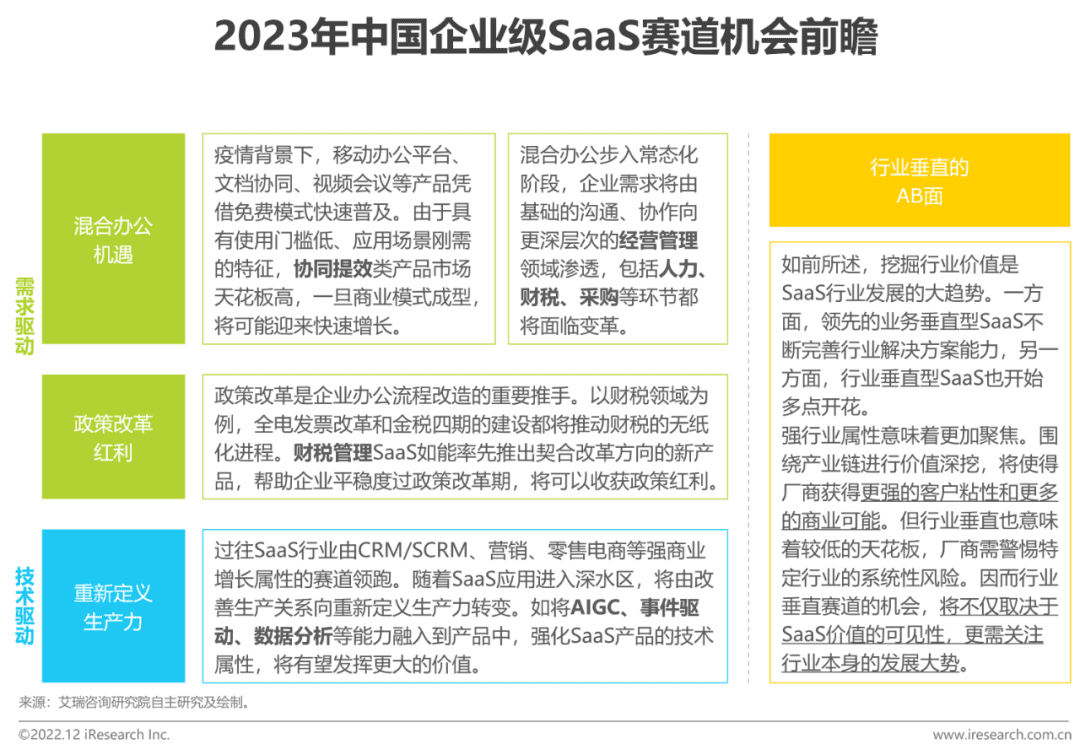

展望未来,SaaS赛道的机会在于挖掘需求与技术红利,借力混合办公、政策改革与生产力重塑。新冠疫情的到来使得企业协作、移动办公等产品快速普及,此类产品门槛低、应用场景刚性,一旦商业模式成型,未来将有望迎来快速增长。除了好风凭借力,SaaS厂商亦需关注提升自身竞争力,主要包括PLG减法思维、丰富销售形式、积累产业背景与发挥非规模化网络效应四方面。

一、中国与全球SAAS市场紧密相关

全球SaaS市场总览数字化转型网www.szhzxw.cn

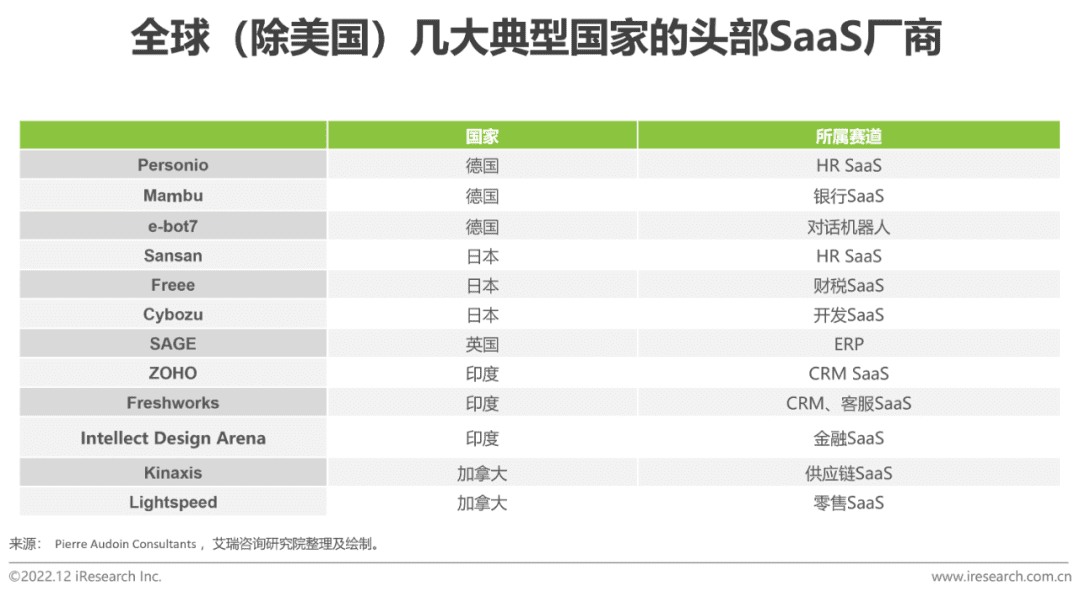

欧洲SaaS市场成长迅速,安全运维与开发类SaaS产品较多

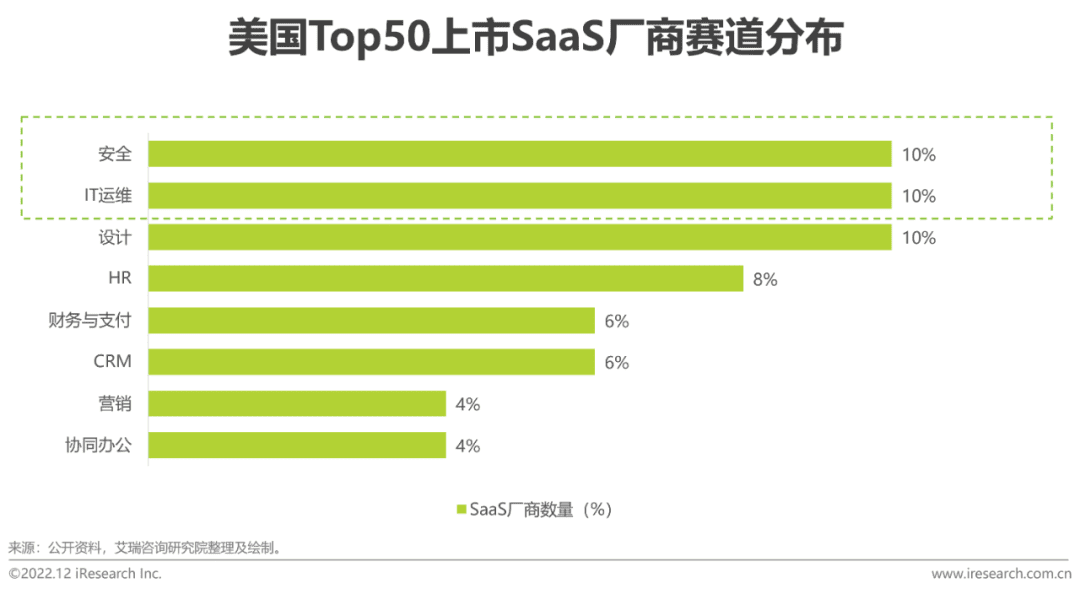

2022年是全球SaaS市场发展放缓的一年,相比于2021年热门赛道厂商动辄数十倍的估值,厂商估值如今普遍已下降至5-10x P/S,甚至低于2020年疫情前的水平。这与整体经济式微有关,也是前一年热度激增后的理性回归,但长期看软件仍是经济发展最重要的动力之一,基于云的商业模式会持续为产业带来长期增长。美国一直被认为是全球SaaS市场的风向标,占全球软件市场36%,但占据全球SaaS市场60%的市场份额,整体来看,国内SaaS市场总量依然不及欧美发达市场,且从品类分布上看,安全运维、开发类产品发展偏弱。数字化转型网www.szhzxw.cn

美国SaaS市场现状

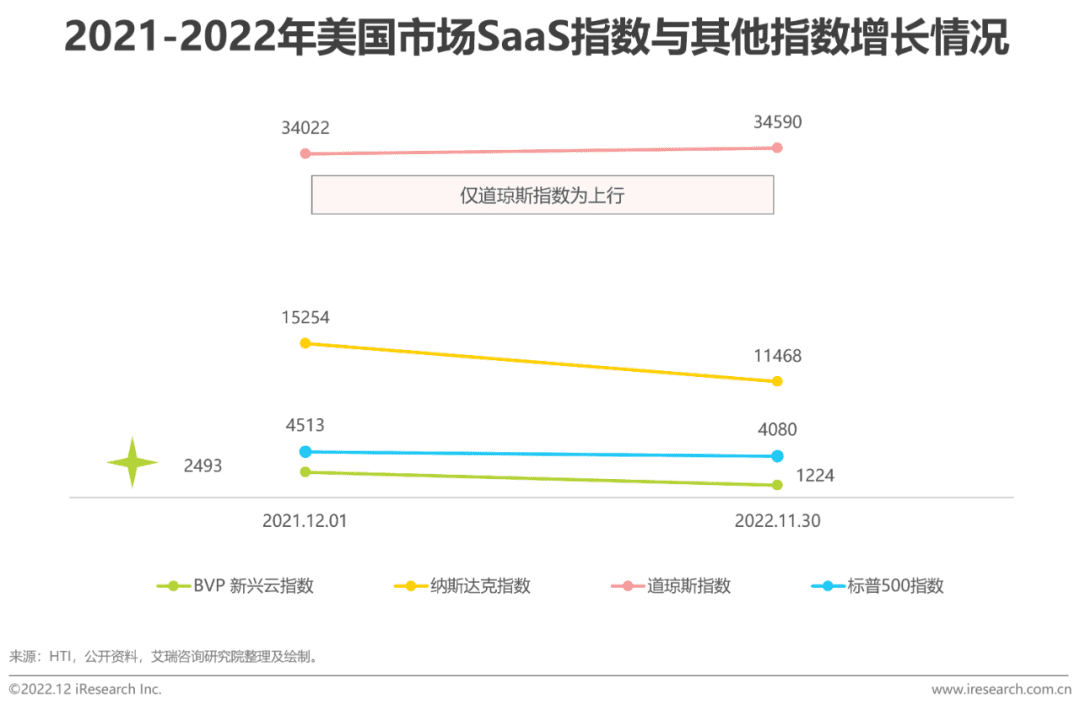

短周期内市场遇冷,SaaS厂商股价与估值回落明显

美国是全球SaaS发展最成熟的市场,上市厂商数量、SaaS化程度与覆盖场景数量都处于绝对领先地位。但在过去一年,其SaaS市场却出现了负增长,BVP新兴云指数为-50.9%,缩水程度远高于大盘。对比来看, SaaS公司的估值倍数已经降到了低于大部分历史水平的程度:比5年平均水平的12.9倍低32%,相比10年平均水平的9.4倍也低了7%。这意味着一些SaaS厂商过去“低利率、快扩张”的打法目前受到强烈挑战,而国内的SaaS厂商亦同样受到波及。

中国SaaS厂商发展的全局观

SaaS是企业全面数字化的关键切入口和场景孵化器

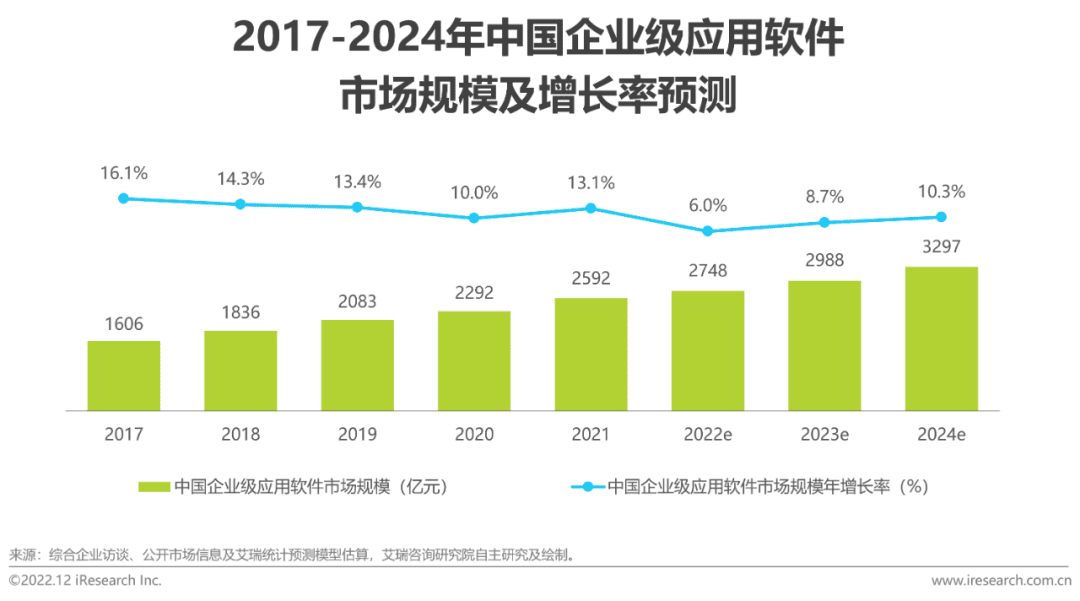

数字化转型已然成为当代企业应对生存竞争的必修课,但如何切实有效的实施数字化转型,对于大部分企业来说仍然是一个问号。从顶层设计到落地执行,数字化转型面临着高投入、高风险、长周期等的诸多困难,具有订阅付费、敏捷部署、快速验证特性的SaaS无疑是一个有意义的尝试。根据艾瑞咨询测算,2021年中国企业级应用软件市场规模达到2592亿元,SaaS在其中占比达到28.1%。在企业数字化转型的全景图中,SaaS扮演着应用场景层面的关键作用,往往是企业特定环节数字化的直接切入口。同时,千行百业中的无数企业,正是在实际业务场景中不断发现数字化技术/工具的落地可用之处,从而使SaaS最大程度地承接了数字化“场景孵化器”的重任。数字化转型网www.szhzxw.cn

二、产业链核心解读之中国SAAS行业洞察

中国企业级SaaS市场规模及预测

SaaS市场受宏观经济下行压力波及,行业增速逐渐放缓

根据艾瑞咨询测算,2021年中国企业级SaaS市场规模达到728亿元,同比增速由2020年的48.7%下降到35.2%。与疫情爆发之初受益于远程办公的利好形势不同,宏观经济下行、总需求收缩的影响开始逐渐传导到SaaS行业。预计2022年,SaaS行业的增速将首次下探至10%以下。未来三年SaaS行业的增长也将与宏观经济恢复速度相挂钩,在中性预期下,到2024年中国企业级SaaS市场规模将有望达到1201亿元,2021-2024年的年复合增长率为18.1%。

中国企业级SaaS细分市场规模

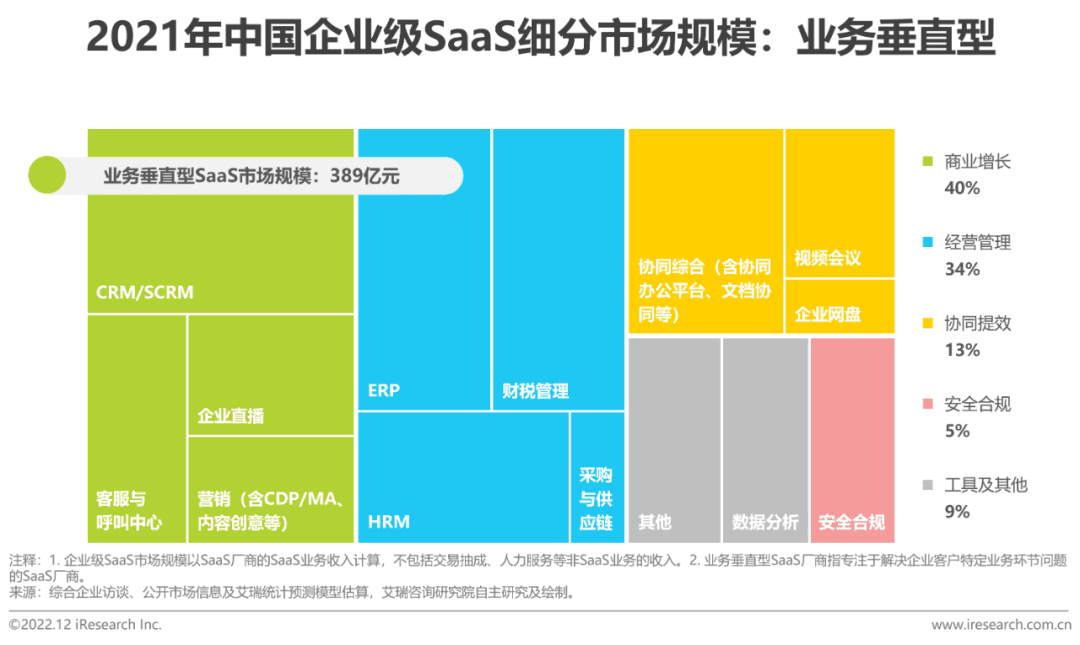

业务垂直型SaaS市场规模389亿元,其中商业增长+经营管理类占比超70%

2021年,中国业务垂直型SaaS市场规模达到389亿元,同比增长33.2%。其中,商业增长类中的CRM/SCRM得益于企业的开源需求与效益直观可见的优势,经营管理类中的财税管理受到财税无纸化相关政策的利好,协同办公类中的协同综合由免费铺量进入到商业变现阶段,均有不错的增长表现,高于业务垂直型的平均增速。

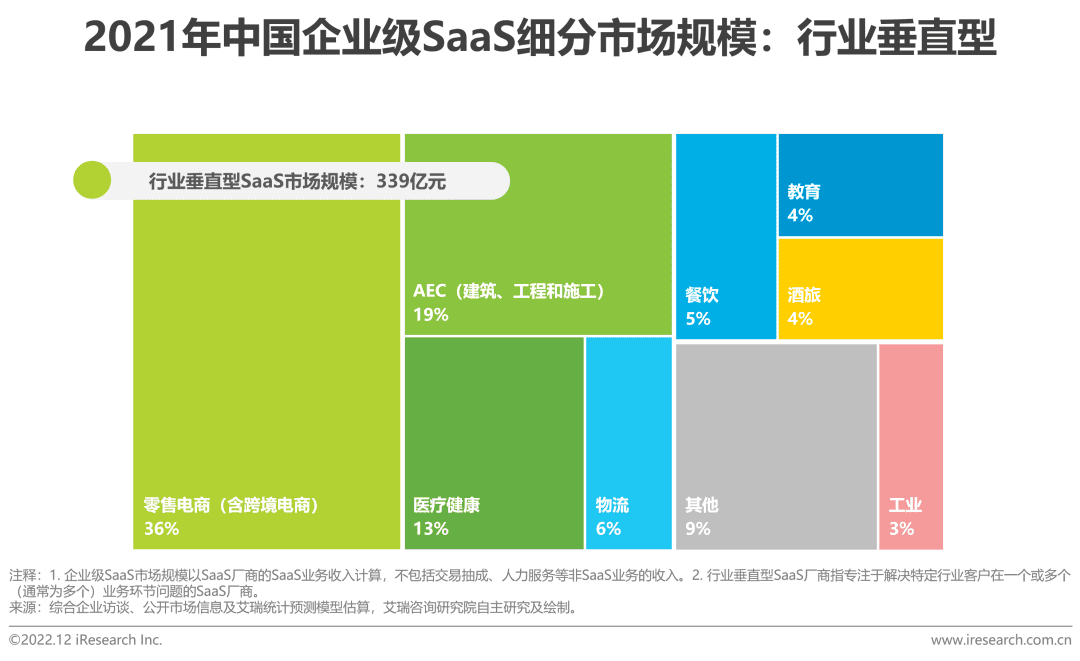

行业垂直型市场规模339亿元,零售电商SaaS增速持续领跑

2021年,中国行业垂直型SaaS市场规模达到339亿元,同比增长37.6%。其中,微商城、电商ERP等SaaS产品继续保持稳定增长,加之跨境电商SaaS异军突起,零售电商领域增速领跑行业垂直型SaaS,市场规模占比进一步提升,达到36%。教育SaaS受到“双减”政策的影响,规模出现一定的收缩,相关厂商也纷纷从K12向教育信息化、素质教育转型。此外,随着企业接受程度的持续攀升,SaaS开始进入到更多的垂直行业,其他类SaaS占比增加至9%,呈现出百花齐放的态势。

中国企业级SaaS市场结构及预测

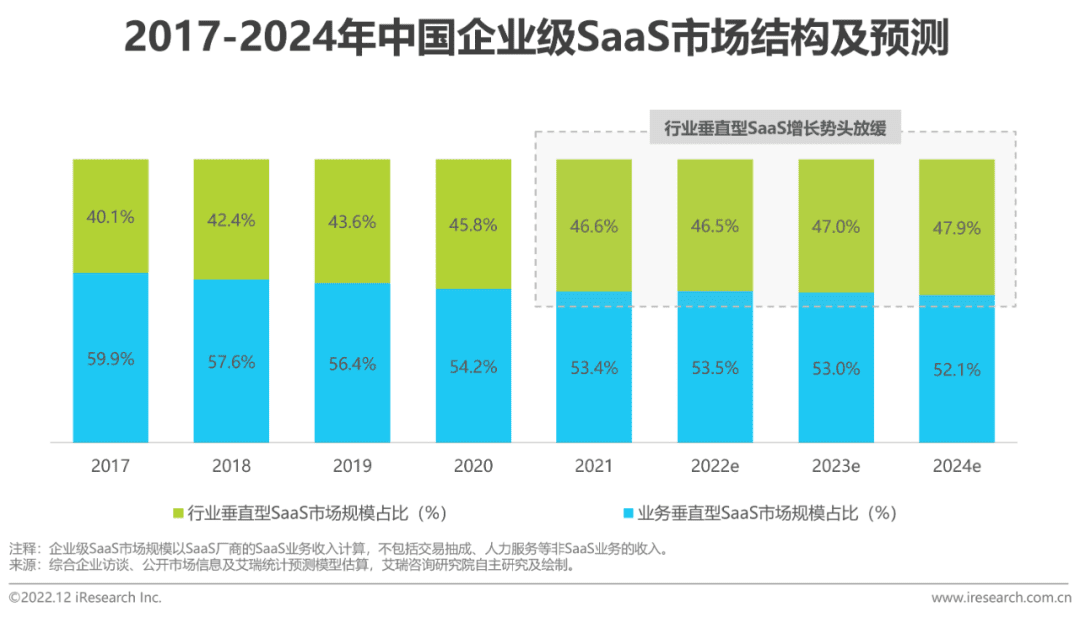

2021年业务垂直型占比为53.4%,行业垂直型增长势头放缓

根据艾瑞咨询测算,2021年中国企业级SaaS市场规模中,业务垂直型与行业垂直型的占比分别为53.4%和46.6%。相比2017年的40.1%,行业垂直型的占比已有明显增长。随着宏观经济的不确定性增强,2021年以来,部分行业或受疫情影响或受政策影响,出现了较大的波动。相比业务垂直型产品在不同行业间具有较强的通用性,行业垂直型SaaS在对抗系统性风险方面的能力稍弱。预计在未来的三年中,尽管行业垂直型的占比仍将呈现上升趋势,但增长势头将有所放缓。

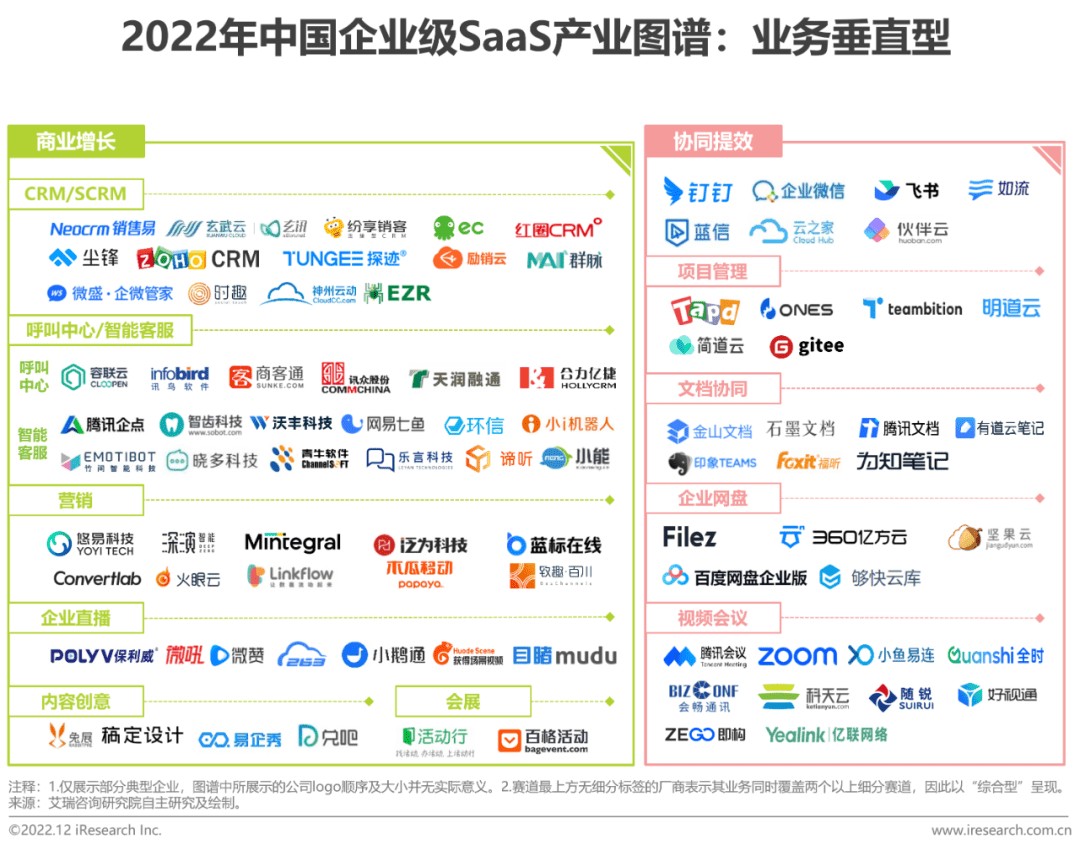

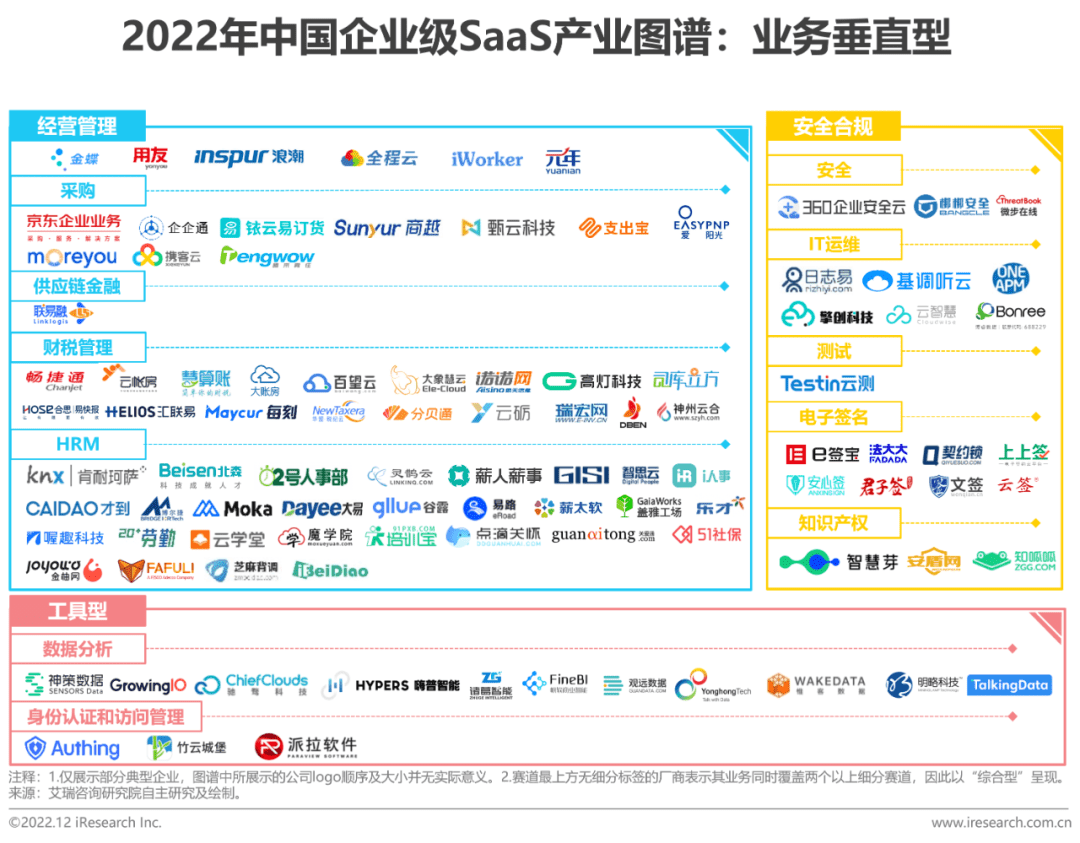

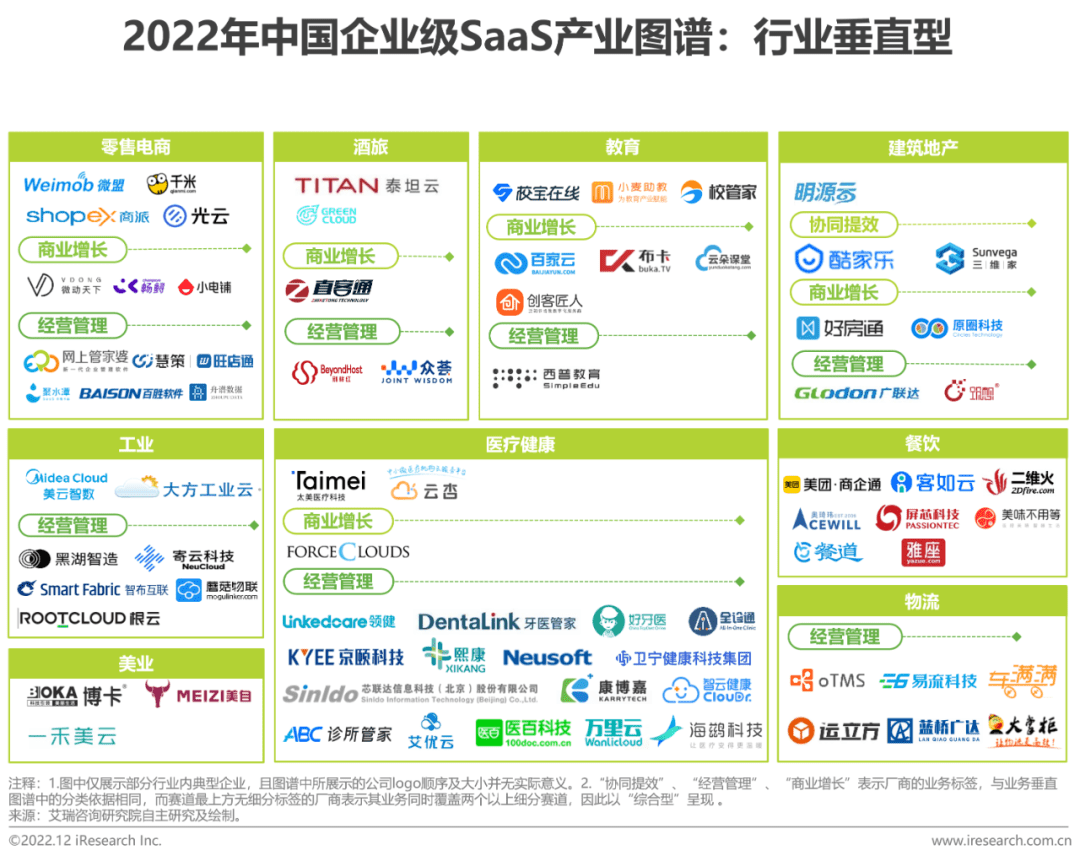

中国企业级SaaS产业图谱

中国企业级SaaS产业图谱

中国企业级SaaS产业图谱

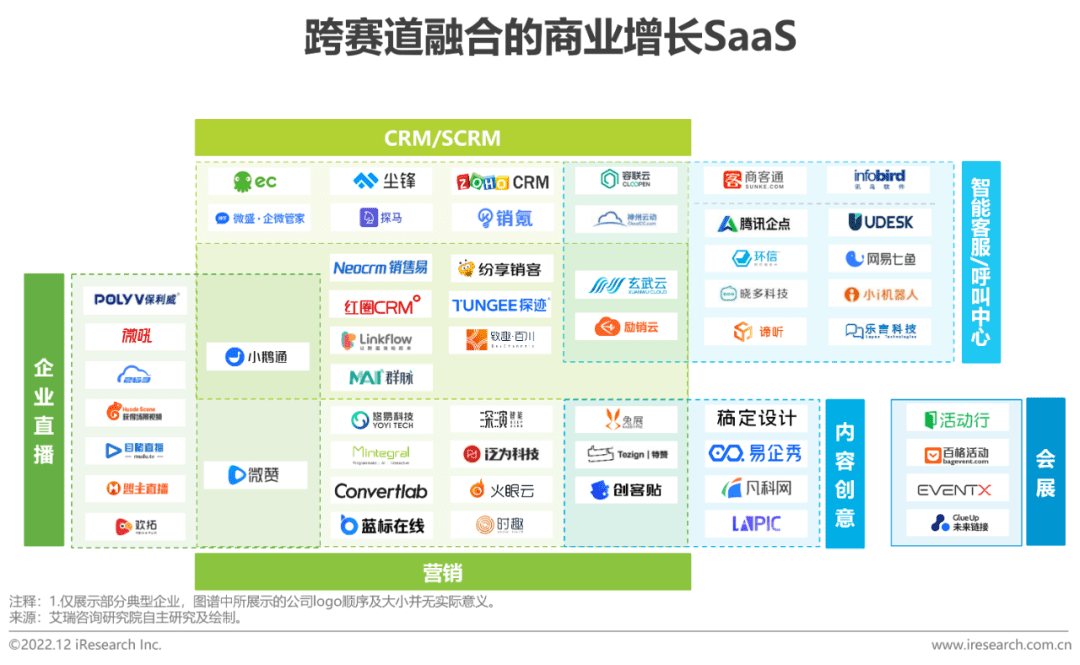

SaaS赛道的融合趋势

商业增长SaaS厂商开始向营销服务和CRM拓展业务布局

随着业务的深入和服务经验的积累,部分赛道的SaaS产品边界变得愈发模糊,SaaS厂商开始尝试同时布局多条产品线,拉通服务链路。由于商业增长SaaS成熟度较高,且多以直接或间接提升销售转化率为目的,因此这种跨赛道布局产品线的形式在商业增长SaaS厂商中较为明显。如部分CRM、SCRM、企业直播和内容创意厂商向营销领域拓展业务版图,也有CRM厂商发展了智能客服或呼叫中心业务,提升客户触达率。

财税与HRM赛道逐渐成熟,厂商由点及面加速一体化布局;工具型SaaS横向渗透并融合特定业务场景来发挥自身价值

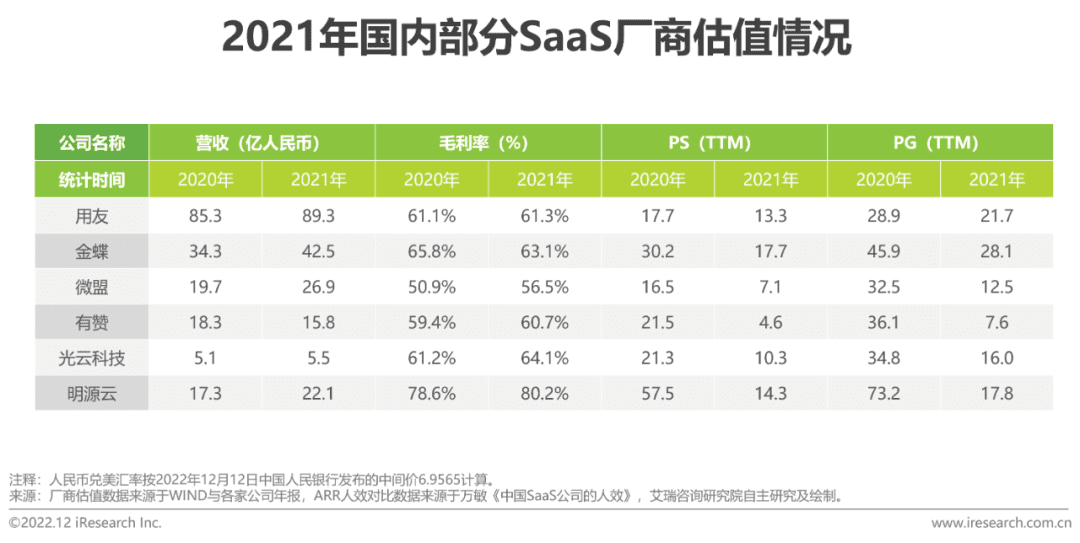

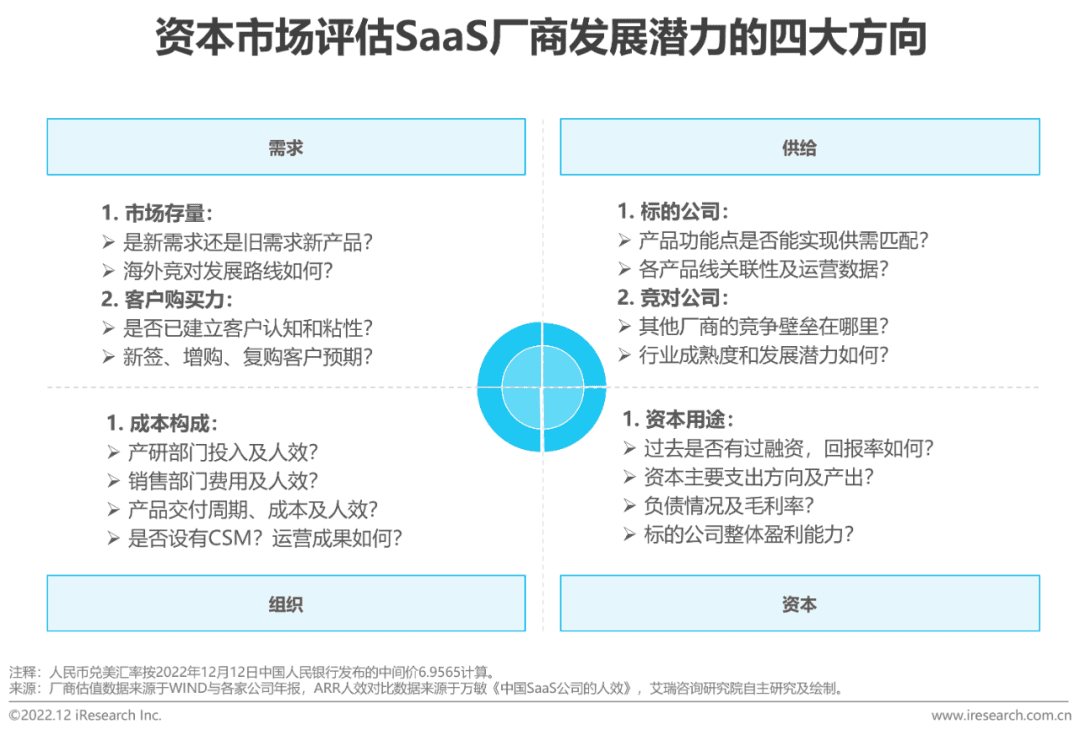

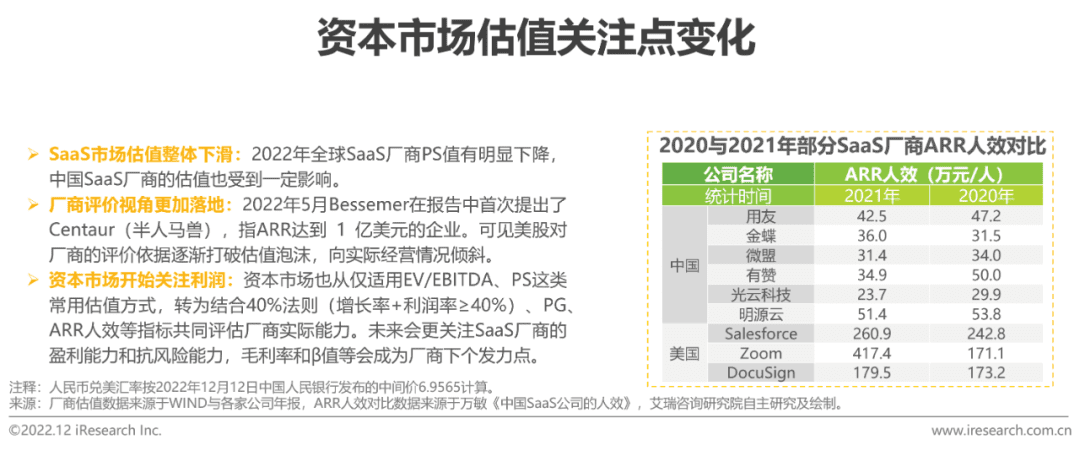

中国企业级SaaS的估值方向

估值有所回落,资本市场重心向盈利能力和抗风险能力倾斜

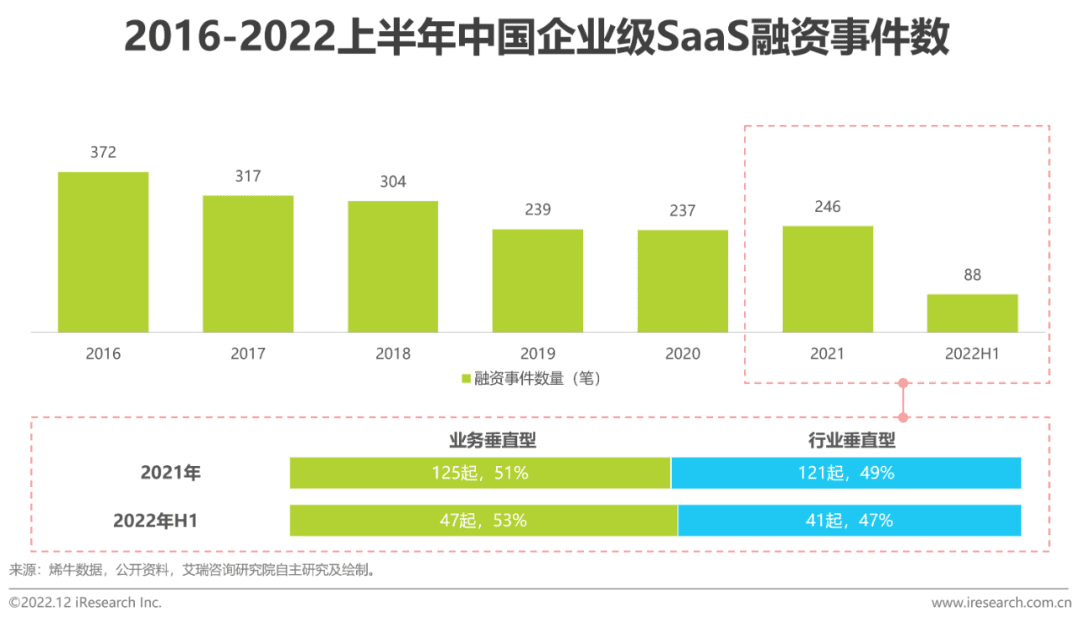

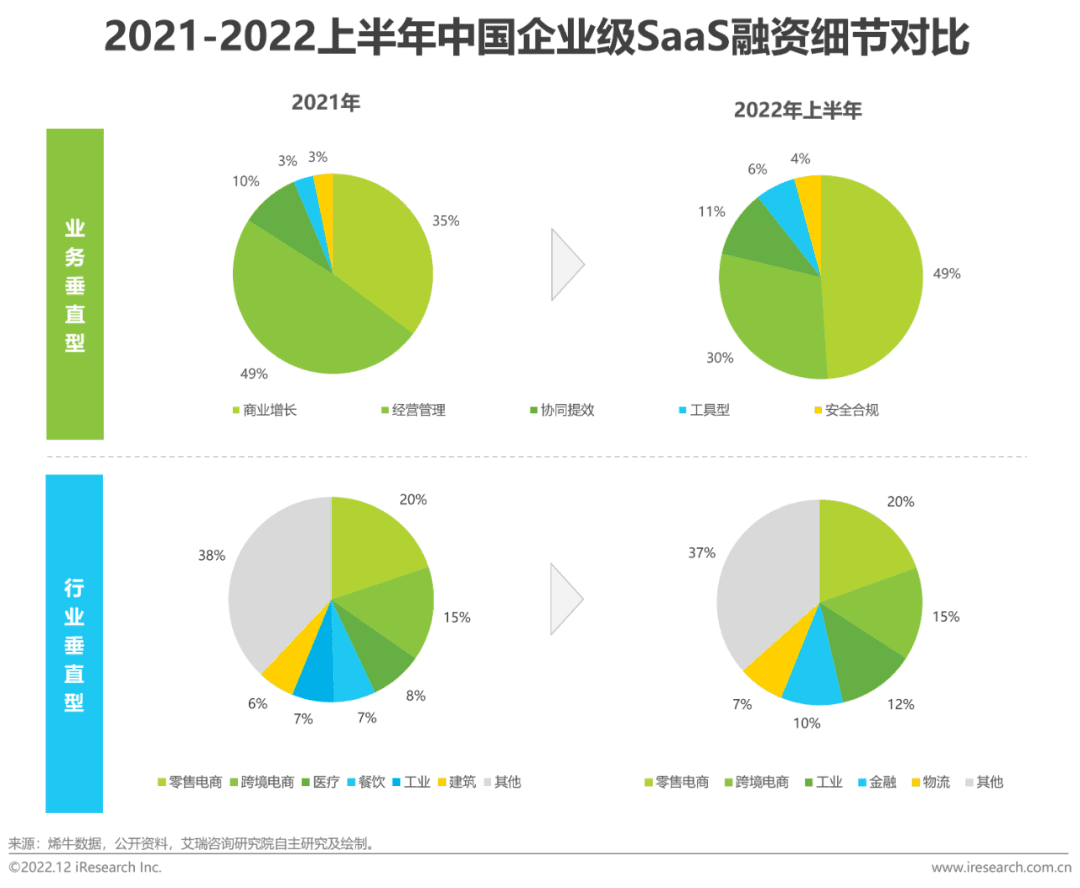

中国企业级SaaS投融资梳理

业务垂直中市场重视开源节流,行业垂直中电商热度高

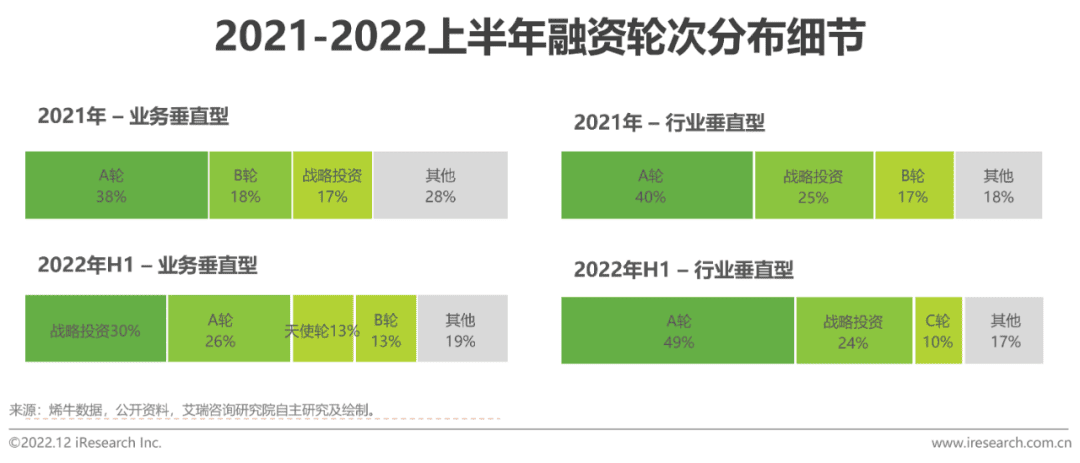

中国企业级SaaS投资热度在2021年有小幅回暖,而后受疫情影响在2022年有所回落。从2021年至今的融资细节上看,有以下特点:(1)业务垂直型与行业垂直型SaaS投资比重维持稳定,投资数量分别占比约50%;(2)业务垂直型SaaS投资商业增长和经营管理类SaaS占比近80%,且受疫情影响,企业需要更多开源软件,因此2022年H1商业增长类SaaS投资数量增加;(3)行业垂直型SaaS投资数量中,电商相关SaaS占比最高,近35%。CAD云端设计及渲染、工厂管理等工业领域SaaS也较受关注。同时,由于疫情影响,部分与线下业务联系紧密的业务如餐饮管理类SaaS热度明显降低。数字化转型网www.szhzxw.cn

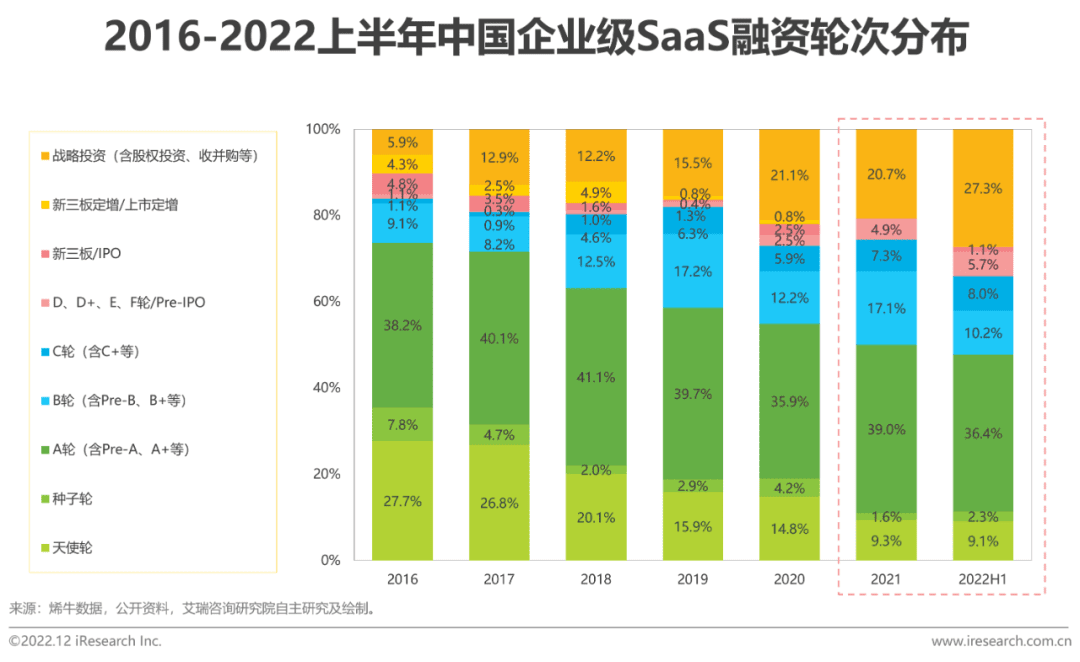

资本关注产品成型的“潜力股”和商业路径成型的“蓝筹股”

相比2016年,2022年上半年的股权投资、收并购等战略投资比重增加了21.4个百分点,而天使轮与种子轮占比下降了18.6个百分点,可见中国企业级SaaS市场走向成熟的同时,资本市场对“概念热度”的态度更加理性,目光分别向产品初具形态的厂商及商业路径相对成熟的厂商侧倾斜。就2021年和2022年上半年融资结构上看,商业模式成熟的业务垂直型SaaS更受关注,而产品成型、潜力较大的行业垂直型SaaS更受青睐,但整体没有呈现太大差异。

三、产业链核心角色解读

SaaS厂商渠道体系的价值定位

破除二元对立关系,借渠道商之手快速拓展市场

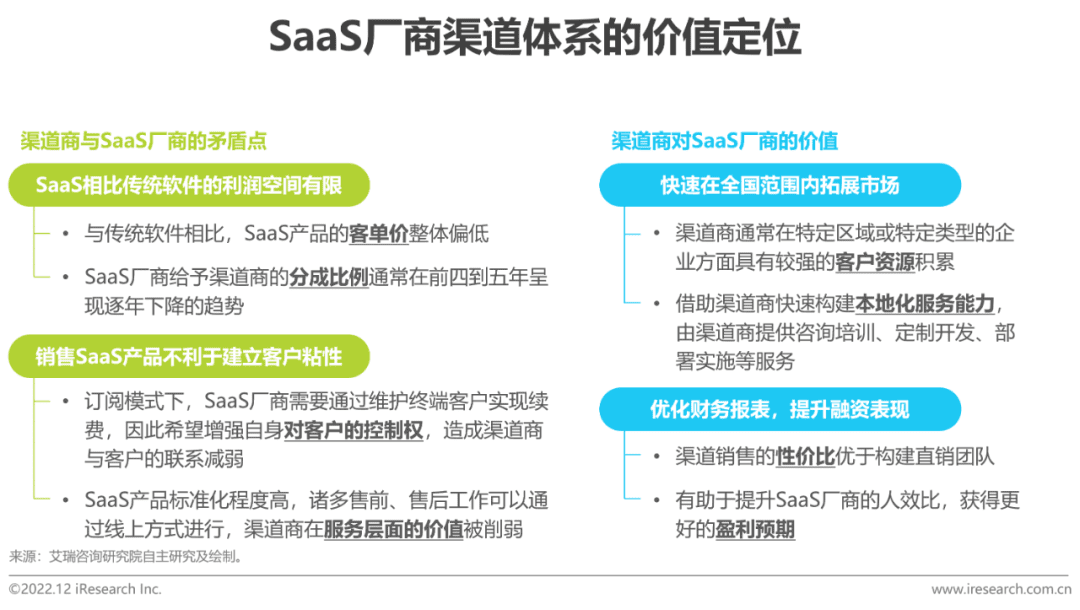

渠道是传统软件重要的销售方式之一,但对于SaaS产品是否应同样采用渠道销售,业内一直存在诸多争议。一方面,销售SaaS产品无法赋予渠道商与传统软件一样足够的利润空间;另一方面,订阅模式必然要求SaaS厂商加强对客户的持续性服务,因而在客户的归属和权责分界上,厂商与渠道商间更容易存在利益冲突。

而随着中国SaaS市场规模的快速增长,渠道商为维持自身竞争力,开始从传统软件转向SaaS销售。同时SaaS行业步入买方市场,规模化扩张与销售转化的价值被放大,渠道商快速拓展市场的能力凸显。SaaS厂商与渠道商的关系趋于缓和,双方逐步合作探索SaaS时代下的渠道销售模式。

SaaS厂商与渠道商的合作思路

结合产品特性选择伙伴类型,双向赋能稳固渠道合作关系

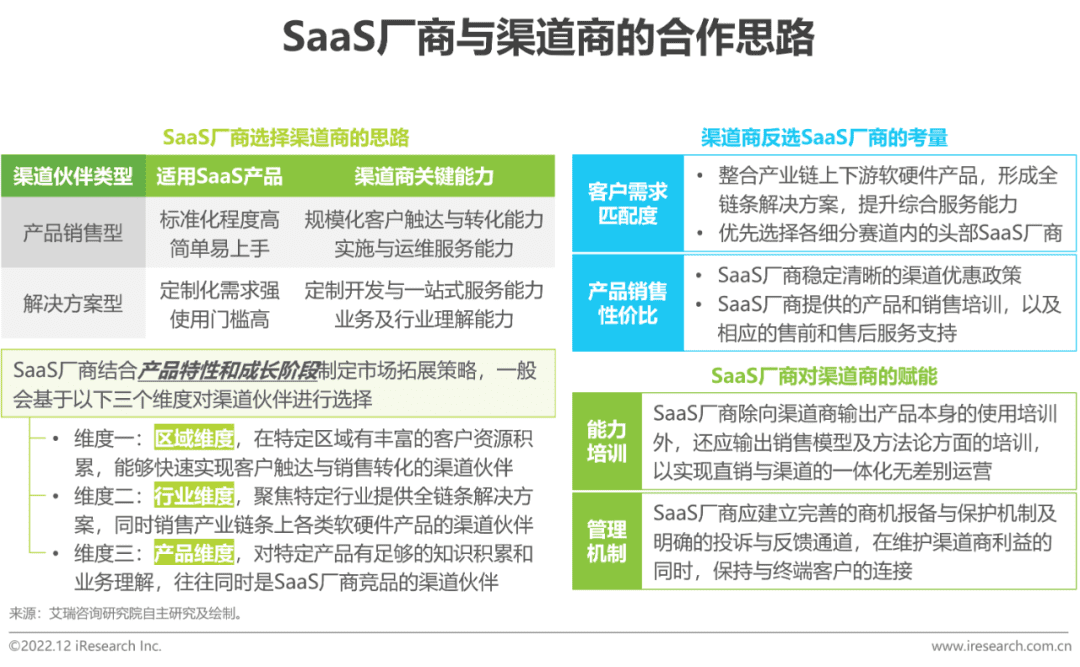

根据渠道伙伴承担的职能不同,可以将渠道商简单划分为产品销售型、解决方案型两类,SaaS厂商应根据自身产品的标准化程度和使用门槛,考虑选择触达能力更强还是服务能力更强的渠道伙伴。由于SaaS厂商与渠道商之间是双向选择,除了提供有竞争力的渠道优惠政策外,SaaS厂商面向渠道商的能力培训和管理机制同样至关重要,只有与渠道商建立起稳定的合作关系,才能有效发挥渠道的价值,向终端客户输出一致的服务体验。

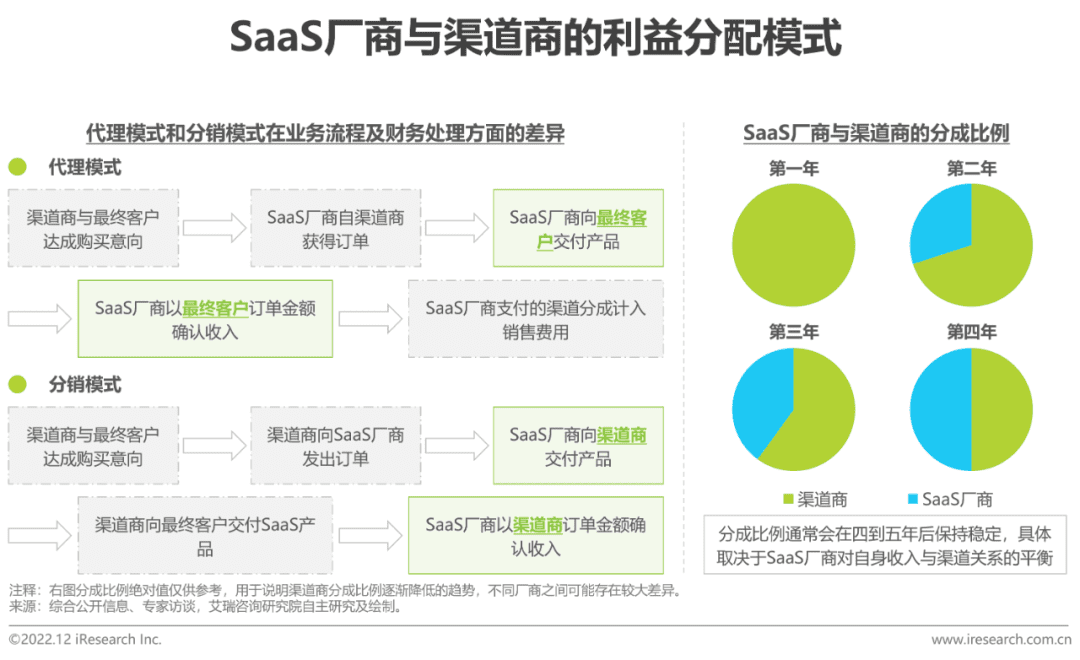

SaaS厂商与渠道商的利益分配模式

渠道商分成比例通常会在前4-5年呈现逐年降低的态势

渠道销售存在代理和分销两种模式。在代理模式下,SaaS厂商对终端客户有较强的主导权,以最终客户订单金额确认收入,渠道分成计入销售费用;而分销模式赋予了渠道商更大的自主性,SaaS厂商向渠道商交付产品,并以渠道商的订单金额确认收入。由于渠道商在前期的拓客中投入较多精力,通常SaaS厂商会在产品销售的前几年给予渠道商更多的分成,以激励渠道商,随着时间的推移,渠道商收获的分成比例将会逐步降低,后期基本稳定在50%左右。

云市场中的SaaS应用

构建SaaS应用市场,企业可一站式选配产品与构建环境

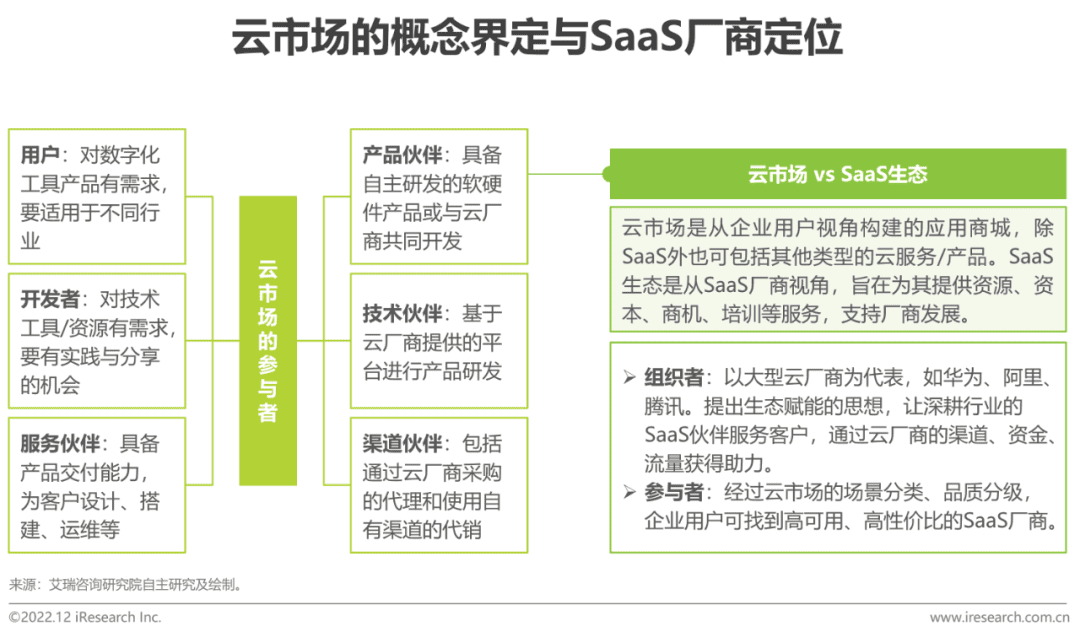

云市场本身是由大型云厂商搭建的聚焦于服务企业客户的第三方软件与服务交易平台,通过连接用户、开发者、产品、技术、服务、渠道等不同伙伴,聚合云领域的产品与服务,包括云主机资源、运行环境、产品应用等板块。云市场生态中,SaaS厂商多作为产品伙伴,而云市场类似于综合应用商店,涵盖了适用于各垂直场景、各行业场景的SaaS应用,企业用户可以一站式选购并快速使用。目前,诸多互联网大厂均在积极布局云市场建设,试图打造更加一站式的综合数字化平台。

云市场模式解读

广泛覆盖企业场景,发挥云市场、SaaS厂商与企业三方合力

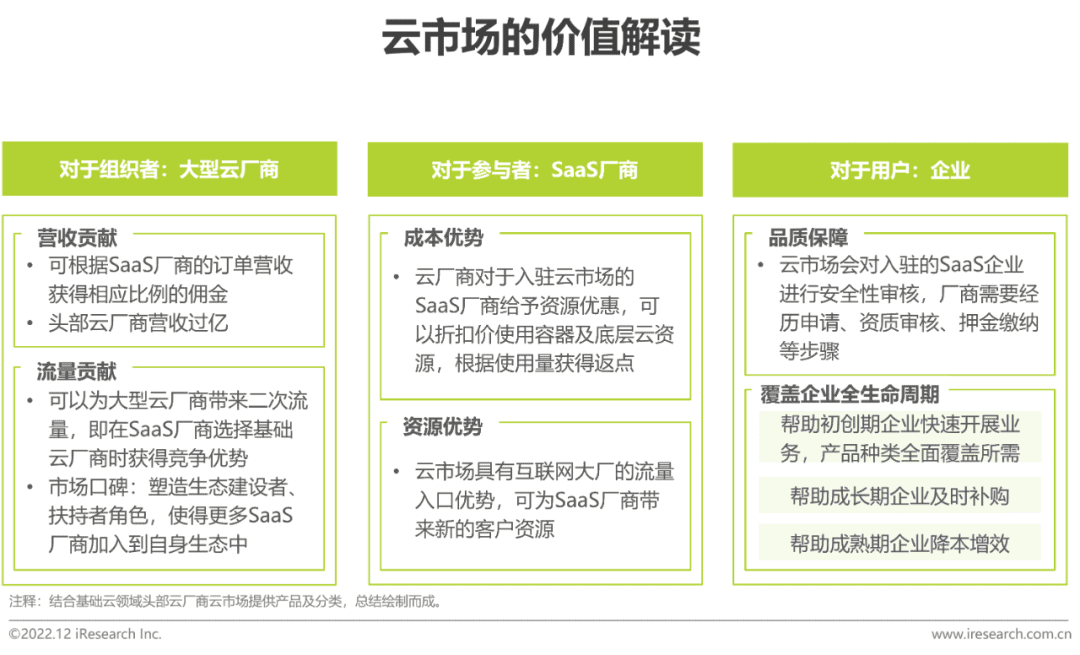

云市场能够帮助SaaS厂商触达更多用户,塑造企业品牌,借助大型云厂商的资源更好地与客户建立联系、增强信心;对于企业用户而言,经过筛选与分级的SaaS厂商也更有质量保障。云市场往往会对ISV进行分级,并负责引流推广,目前营销、HR、零售电商、建栈类SaaS在几大云市场中关注度较高。除了综合性云市场,垂直办公场景中同样出现了类似的玩法(如“云钉一体”)。

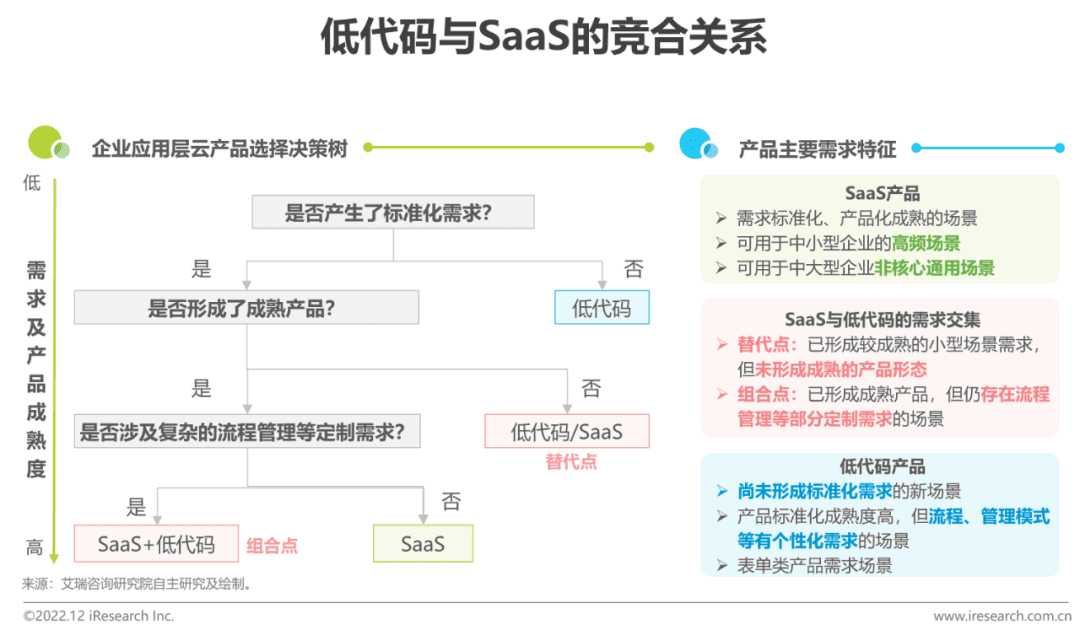

SaaS与低代码的替代关系

从场景上看,低代码与SaaS的市场有小幅重叠但无正面竞争

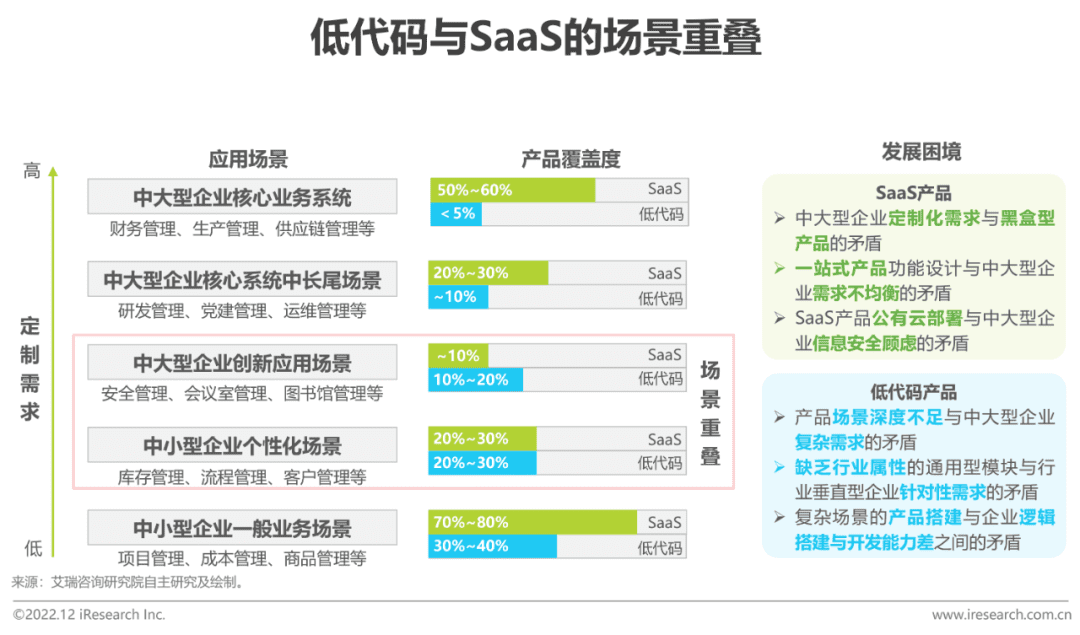

发展至今SaaS和低代码产品均渗透了大中小企业的各业务场景,一定程度上造成了二者存在替代关系的“竞争错觉”。其中,SaaS产品的特点有:①通用场景和行业性垂直场景发展较快,个性化程度高、使用频率低和创新性高的场景发展较慢;②标准化程度过高,难以适应中大型企业复杂的应用场景。低代码的特点有:①适用中小型企业通用业务场景及企业个性化需求高的低频场景;②复杂场景下,企业仍需要厂商将应用搭建完成后,以SaaS的形式交付。事实上,在不同场景下,SaaS和低代码的产品成熟度(覆盖度)存在明显差异,通常企业更偏好相对成熟的产品。但在中小型企业个性化场景和中大型企业创新应用场景这类定制需求较高的场景中覆盖程度相似,SaaS与低代码存在一定竞争关系。

从产品上看,低代码与SaaS在特定场景下存在替代和组合机会数字化转型网www.szhzxw.cn

企业在不同需求和产品成熟度环境下,对SaaS与低代码的选择会有所偏好,二者的少量交集可归类为以下两种情形:(1)场景需求标准化但尚未形成成熟产品时,存在替代关系:由于产品研发存在滞后性,在需求成型与产品化成熟之间存在时间区隔,该时间内企业选择使用功能不够完善的SaaS产品,和选择通过低代码平台自行完成系统搭建的意愿是均等的。(2)已形成成熟产品但仍存在复杂的流程管理等定制需求时,存在组合关系:对于部分已形成成熟产品的场景,由于不同企业流程管理逻辑存在差异,可以通过SaaS+低代码的形式,以“整体标准,局部定制”的产品形态满足企业场景需求。

四、中国SAAS行业发展趋势前瞻

SaaS赛道机会前瞻

挖掘需求与技术红利,探索混合办公、政策改革、生产力重塑的机会点

翻译:

Enterprise SaaS Research Report

Core summary:

The development of China’s SaaS market is inseparable from the process of the global market. The development speed of the global SaaS industry has slowed down in the past year, and the US SaaS giants have suffered from problems such as weak growth, loss of performance and low stock price. But new players in emerging countries are bucking the trend, such as the fast-growing Indian market. For Chinese enterprises, overseas listing is no longer a must-win method, but a compulsory course to face the competition is to deepen the digital transformation needs of domestic enterprises.

In 2021, the scale of China’s enterprise SaaS market is 72.8 billion yuan, the year-on-year growth rate decreased from 48.7% in 2020 to 35.2%. Compared with the optimistic expectation at the beginning of the outbreak of the epidemic, it is believed that the macroeconomic downturn has brought greater pressure, and the contraction of the total demand for enterprise SaaS will lead to a sharp decline in the industry growth rate. It is estimated that in 2022, For the first time, growth in the SaaS industry will fall below 10%. In the next three years, the growth of SaaS industry will also be linked to the speed of macroeconomic recovery. Under the neutral expectation, the scale of China’s enterprise SaaS market is expected to reach 120.1 billion yuan by 2024, with a compound annual growth rate of 18.1% from 2021 to 2024.

With the deepening of business and the accumulation of service experience, the boundaries of SaaS products in some circuits become more and more blurred.

SaaS manufacturers begin to try to arrange multiple product lines at the same time and connect service links. Business growth SaaS manufacturers begin to expand business layout to marketing and CRM, and the finance and tax and HRM track is gradually mature. Manufacturers accelerate the integration layout from point to point, and tool SaaS horizontal penetration and integration of specific business scenarios to play their own value.数字化转型网www.szhzxw.cn

Going forward, the opportunity for the SaaS circuit is to tap into demand and technology dividends, leveraging a mix of office, policy change and productivity reinvention. The arrival of the novel coronavirus pandemic has made enterprise collaboration, mobile office and other products rapidly popular. Such products have low threshold and rigid application scenarios. Once the business model takes shape, it is expected to usher in rapid growth in the future. In addition to relying on good wind power, SaaS vendors also need to focus on improving their competitiveness, which mainly includes PLG subtraction thinking, enriching sales forms, accumulating industrial background and giving play to non-scale network effects.

China is closely related to the global SAAS market

Overview of the global SaaS market

The SaaS market in Europe is growing rapidly, and there are many SaaS products related to security operation and maintenance and development

In 2022, the development of the global SaaS market slowed down. Compared with the tens of times valuation of the hot track vendors in 2021, the valuation of the vendors has generally dropped to 5-10x P/S, even lower than the pre-pandemic level in 2020. This is related to the overall economic slowdown, and it is also a rational return after the surge of heat in the previous year.

However, in the long term, software remains one of the most important drivers of economic development, and the cloud-based business model will continue to bring long-term growth to the industry. The United States has always been regarded as the bellwether of the global SaaS market, accounting for 36% of the global software market, but accounting for 60% of the global SaaS market. On the whole, the total domestic SaaS market is still less than the developed markets in Europe and the United States, and from the category distribution, the development of security, operation and development products is weak.

Status of the SaaS market in the US

In a short period of time, the market is cold. And the stock price and valuation of SaaS manufacturers fall back significantly

The United States is the most mature SaaS market in the world, with the number of listed vendors. The degree of SaaS and the number of coverage scenarios in an absolute leading position. However, in the past year, its SaaS market has seen negative growth. BVP emerging cloud index of -50.9%, shrinking far more than the broader market. By contrast, valuation multiples for SaaS companies have fallen below most historical levels:. 32% below the five-year average of 12.9 times, and 7% below the 10-year average of 9.4 times. This means that some SaaS vendors in the past “low interest rate, fast expansion” approach is now strongly challenged. And domestic SaaS vendors are also affected.

A holistic view of the development of Chinese SaaS vendors

SaaS is a key entry point and scenario incubator for full digitization of enterprises

Digital transformation has become a required course for contemporary enterprises to cope with the survival competition. But how to effectively implement digital transformation is still a question mark for most enterprises. From top-level design to implementation, digital transformation faces many difficulties such as high investment, high risk and long cycle. SaaS with the features of subscription payment, agile deployment and fast verification is undoubtedly a meaningful attempt. According to iResearch, China’s enterprise-level application software market size reached 259.2 billion yuan in 2021, of which SaaS accounted for 28.1%. 数字化转型网www.szhzxw.cn

In the overall picture of enterprise digital transformation. SaaS plays a key role at the application scenario level and is often the direct entry point to the digitalization of specific aspects of the enterprise. At the same time, countless enterprises in thousands of industries continue to find the application of digital technologies/tools in actual business scenarios. So that SaaS can undertake the responsibility of digital “scene incubator” to the greatest extent.

Insight into China’s SAAS industry from the core interpretation of the industrial chain

China’s enterprise SaaS market size and forecast

The SaaS market is affected by the downward pressure of macro economy, and the industry growth is slowing down gradually

According to iResearch, China’s enterprise-level SaaS market scale reached 72.8 billion yuan in 2021. With a year-on-year growth rate of 35.2%, down from 48.7% in 2020. Unlike at the beginning of the pandemic, which benefited from telecommuting. The impact of the macroeconomic downturn and aggregate demand contraction is gradually spreading to the SaaS industry. In 2022, growth in the SaaS industry is expected to dip below 10% for the first time. In the next three years, the growth of SaaS industry will also be linked to the speed of macroeconomic recovery. Under the neutral expectation, the scale of China’s enterprise SaaS market is expected to reach 120.1 billion yuan by 2024. With a compound annual growth rate of 18.1% from 2021 to 2024.

China’s enterprise SaaS market segment size

Vertical business SaaS market size of 38.9 billion yuan. Of which business growth + operation and management accounted for more than 70%

In 2021, the vertical SaaS market scale in China reached 38.9 billion yuan, with a year-on-year growth of 33.2%. Among them, CRM/SCRM in the category of business growth benefits from the advantages of open source demand and visible benefits of enterprises; fiscal and tax management in the category of operation management is benefited by the related policies of paperless fiscal and tax; collaborative comprehensive in the category of collaborative office enters the stage of commercial realization from free shop volume, with good growth performance, higher than the average growth rate of vertical business.

The vertical market size of the industry is 33.9 billion yuan. And the growth rate of retail e-commerce SaaS continues to lead

In 2021, China’s vertical SaaS market reached 33.9 billion yuan, up 37.6 percent year on year. Among them, SaaS products such as micro mall and e-commerce ERP continue to maintain stable growth. Coupled with the sudden emergence of cross-border e-commerce SaaS. The growth rate of retail e-commerce leads the vertical SaaS industry, and the market size has further increased to 36%. Influenced by the “double reduction” policy, the scale of educational SaaS has shrunk to a certain extent. And relevant manufacturers have also transformed from K12 to education informatization and quality education. In addition, as enterprise acceptance continues to climb, SaaS begins to enter more vertical industries. With other SaaS categories accounting for 9% of the total, showing a blossoming trend.

China’s enterprise SaaS market structure and forecast

In 2021, the vertical business accounted for 53.4%, and the vertical growth momentum of the industry slowed down

According to the estimates of iResearch, in China’s enterprise-level SaaS market size in 2021. The proportion of business vertical and industry vertical is 53.4% and 46.6% respectively. Compared with 40.1% in 2017, the proportion of vertical industry has increased significantly. With increased macroeconomic uncertainty, some industries have experienced significant fluctuations since 2021. Either because of the epidemic or because of policies. Compared with business vertical products, which have stronger versatility across different industries. Industry vertical SaaS is less able to combat systemic risk. It is expected that in the next three years. Although the vertical proportion of the industry will still show an upward trend, but the growth momentum will slow down.

China enterprise SaaS industry map

China enterprise SaaS industry map

China enterprise SaaS industry map

Convergence trend of SaaS track数字化转型网www.szhzxw.cn

Business Growth SaaS vendors are branching out into marketing services and CRM

With the deepening of business and the accumulation of service experience. The boundaries of SaaS products in some circuits become more and more blurred. SaaS manufacturers begin to try to arrange multiple product lines at the same time and connect service links. This cross-track layout of product lines is evident among commercial growth SaaS vendors due to the maturity of commercial growth SaaS and the direct or indirect goal of increasing sales conversion. For example, some CRM, SCRM, enterprise live streaming and content creative manufacturers expand their business territory to the field of marketing. And some CRM manufacturers develop intelligent customer service or call center business to improve the customer reach rate.

Finance and HRM track gradually mature, manufacturers from the point and surface accelerated integration layout. Instrumental SaaS horizontally penetrates and integrates specific business scenarios to achieve its value

The valuation direction of enterprise SaaS in China

Valuations have come down and the focus of capital markets has tilted towards profitability and resilience

Chinese enterprise SaaS investment and financing review

Business vertical in the market attaches importance to open source and reduce expenditure, industry vertical e-commerce heat

China’s enterprise-level SaaS investment rebounded slightly in 2021, and then declined in 2022 due to the impact of the epidemic. From the financing details since 2021, there are the following characteristics:

(1) The proportion of business vertical SaaS investment and industry vertical saas investment remains stable, accounting for about 50% respectively;

(2) Business vertical SaaS investment business growth and management SaaS accounts for nearly 80%. And due to the impact of the epidemic, enterprises need more open source software. So the number of H1 business growth SaaS investment increases in 2022;

(3) Among the vertical SaaS investment in the industry, e-commerce related SaaS accounts for the highest proportion, nearly 35%. CAD cloud design and rendering, factory management and other industrial SaaS also attracted more attention. At the same time, due to the impact of the epidemic, the popularity of some businesses closely related to offline business. Such as SaaS catering management, has decreased significantly.

Capital focuses on “potential stocks” of product molding and “blue chip stocks” of business path molding

Compared with 2016, in the first half of 2022, the proportion of strategic investment such as equity investment, revenue merger and acquisition increased by 21.4 percentage points. While the proportion of angel round and seed round decreased by 18.6 percentage points. It can be seen that while China’s enterprise SaaS market is becoming mature. The capital market has a more rational attitude towards “concept heat”. The eye is tilted to the manufacturers whose products are taking shape and the relatively mature commercial path. In terms of financing structure in 2021 and the first half of 2022, business vertical SaaS with mature business model attracts more attention, while vertical SaaS in industries with formed products and greater potential is favored, but the overall difference is not too great.

Interpretation of the core role of the industrial chain

The value proposition of the SaaS vendor channel system

Break the binary opposition relationship and expand the market quickly through the hand of channel suppliers

Channel is one of the important ways to sell traditional software. But there is a lot of controversy in the industry about whether SaaS products should also use channel sales. On the one hand, selling SaaS products does not give distributors the same profit margin as traditional software. On the other hand, the subscription model inevitably requires SaaS vendors to strengthen continuous service to customers. So in the ownership of customers and the boundary between rights and responsibilities, vendors and channel operators are more likely to have conflicts of interest.

With the rapid growth of SaaS market size in China, the channel providers have begun to shift from traditional software to SaaS sales in order to maintain their competitiveness. At the same time, as the SaaS industry enters the buyer’s market. The value of scale expansion and sales transformation is amplified. And the ability of channel providers to rapidly expand the market is highlighted. The relationship between SaaS vendors and channel providers tends to ease, and the two sides gradually cooperate to explore the channel sales model in the SaaS era.

Cooperation ideas between SaaS vendors and channel providers

Select the partner type according to the product characteristics, and strengthen the two-way channel cooperation relationship数字化转型网www.szhzxw.cn

According to the different functions of channel partners, they can be simply divided into product sales type and solution type. SaaS vendors should consider choosing channel partners with stronger reach ability or service ability according to the degree of standardization and usage threshold of their products. Due to the two-way choice between SaaS vendors and channel providers, in addition to providing competitive channel preferential policies, the ability training and management mechanism of SaaS vendors for channel providers is also crucial. Only by establishing stable cooperative relations with channel providers, can the value of channels be effectively played and the consistent service experience be exported to end customers.

Profit distribution model between SaaS vendors and channel providers

In the first 4-5 years, the distribution ratio of channel providers usually decreases year by year

There are two modes of channel sales: agent and distribution. In the agent mode, SaaS vendors have strong dominance over the end customers, and recognize the revenue according to the order amount of the end customers, and include the channel sharing into the sales expenses. The distribution model gives more autonomy to the channel providers. SaaS vendors deliver products to the channel providers and recognize revenue based on the order value of the channel providers. As the channel operators invest more effort in the early stage of the development, usually SaaS manufacturers will give the channel operators more share in the first few years of product sales, in order to encourage the channel operators. As time goes by, the share proportion of the channel operators will gradually decrease, and in the later stage, it will basically stabilize at about 50%.

SaaS applications in the cloud marketplace

To build SaaS application market, enterprises can choose products and build environment in one stop

Cloud market itself is a third-party software and service trading platform built by large cloud manufacturers focusing on serving enterprise customers. By connecting users, developers, products, technologies, services, channels and other partners, products and services in the cloud field are aggregated, including cloud host resources, operating environment, product applications and other sectors. In the cloud market ecosystem, SaaS vendors are mostly product partners, while the cloud market is similar to an integrated application store, which covers SaaS applications applicable to various vertical scenarios and various industry scenarios. Enterprise users can purchase and use saas applications in a one-stop shop. At present, many big Internet companies are actively layout cloud market construction, trying to create a more one-stop comprehensive digital platform.

Cloud market model interpretation

Extensive coverage of enterprise scenarios, play the cloud market, SaaS vendors and enterprises

The cloud market can help SaaS vendors reach more users, build corporate brands, and better connect with customers and enhance confidence with the help of the resources of large cloud vendors. For enterprise users, SaaS vendors that have been screened and graded also have better quality assurance. Cloud markets tend to classify ISVs and take charge of drainage and promotion. At present, SaaS such as marketing, HR, retail e-commerce, and stack construction have attracted high attention in several cloud markets. In addition to the integrated cloud market, the vertical office scene also has a similar play (e.g. “cloud nails”).

The SaaS alternative relationship with low code

From a scenario perspective, the low-code and SaaS markets overlap slightly but do not compete head-on数字化转型网www.szhzxw.cn

Up to now, SaaS and low-code products have permeated all business scenarios of large, small and medium enterprises, resulting in the “competition illusion” of substitution relationship between them to a certain extent. Among them, the characteristics of SaaS products are as follows: (1) The development of general scenarios and industrial vertical scenarios is fast, while the development of scenarios with high degree of personalization, low frequency of use and high innovation is slow; (2) The degree of standardization is too high, which is difficult to adapt to the complex application scenarios of medium and large enterprises.

The characteristics of low code are as follows: (1) It is suitable for common business scenarios of small and medium-sized enterprises and low frequency scenarios with high personalized requirements of enterprises; (2) In complex scenarios, enterprises still need vendors to deliver applications as SaaS after they are built. In fact, there is a significant difference in product maturity (coverage) between SaaS and low-code in different scenarios, with enterprises generally preferring relatively mature products. However, in scenarios with high customization requirements, such as small and medium-sized enterprise personalized scenarios and medium and large enterprise innovative application scenarios, the coverage degree is similar, and SaaS has a certain competitive relationship with low code.

From a product perspective, there are substitution and combination opportunities between low code and SaaS in specific scenarios

Under different requirements and product maturity environments, enterprises will have a preference for SaaS and low code, and a small amount of intersection between the two can be classified into the following two scenarios: (1) When scenario requirements are standardized but mature products have not been formed, there is a substitution relationship: Due to the lag in product development, there is a time gap between demand formation and product maturity.

During this time, enterprises are equally willing to use SaaS products with inadequate functions, and choose to complete system construction by themselves through low-code platforms. (2) When mature products have been formed but complex process management and other customized requirements still exist, there is a combination relationship: for some mature products, due to the differences in the process management logic of different enterprises, the form of SaaS+ low code can be used to meet the requirements of enterprise scenarios in the form of “overall standard, local customization”.

Prospect of the development trend of China’s SAAS industry

SaaS track opportunity foresight数字化转型网www.szhzxw.cn

Explore the demand and technology dividend, and explore the opportunities of mixed office, policy reform and productivity remodeling

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:艾瑞 ;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。