导语:

本报告聚焦国内大型企业的数字化转型市场,报告第一章从实证角度综述我国大型企业数字化市场,并分析了各行业大型企业近年来的主要数字化战略;报告第二章结合单个企业内部数字化发展的步骤和数字化产业演化的整体路径,对国内大型企业开展数字化转型升级的方式、路径和结构进行了解析;报告第三章列举了大型企业数字化市场的代表性特征,以及对市场形态和行为的影响;报告第五章结合二十大政策,对我国企业数字化市场未来发展趋势进行了展望。

一、中国大型企业数字化市场概览(节选)

1、市场规模

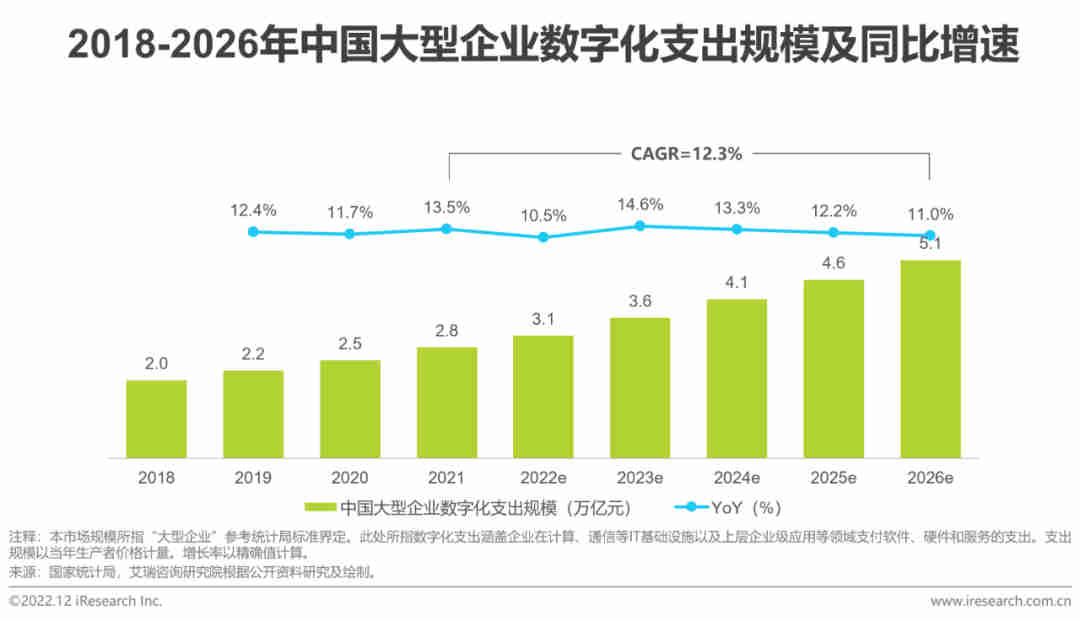

2021年大型企业数字化支出约2.8万亿元,预计未来5年复合增速为12.3%

经艾瑞咨询核算,2021年中国大型企业数字化支出规模约为2.8万亿元,估算2021-2026年中国大型企业数字化支出平均复合增速将达到12.3%。受疫情和宏观经济增长状况影响,2020和2022年大型企业数字化支出增速有所波动,预计2023年市场景气度将有所恢复。整体来看,由于大型企业数字化转型需求具备相对刚性,且大型企业自身扛风险能力较强,市场增速整体平稳。

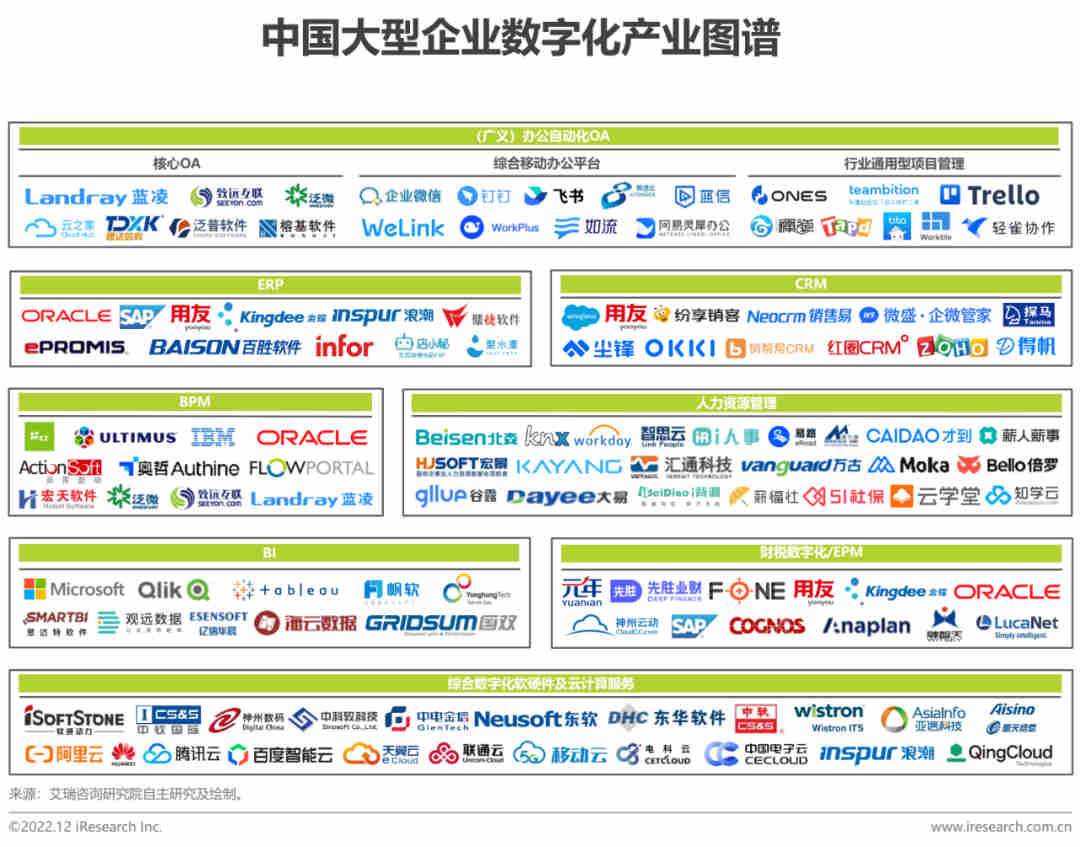

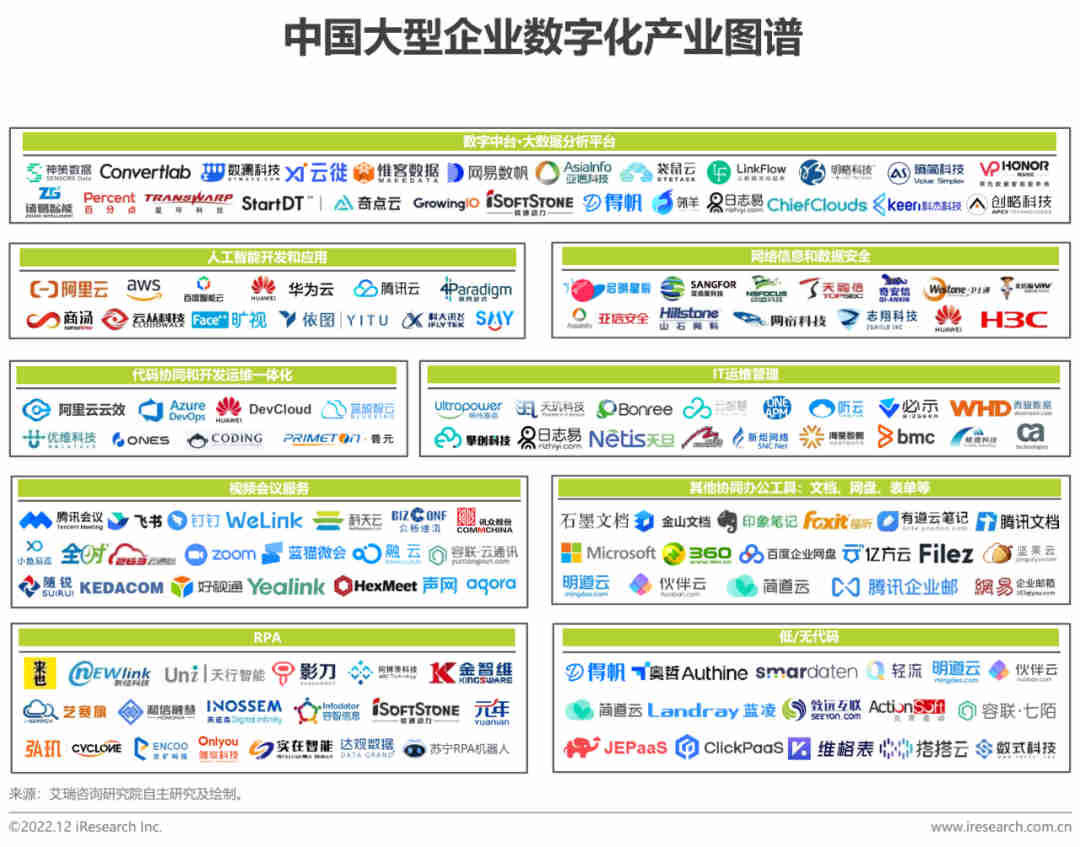

2、产业图谱

二、大型企业数字化升级的结构与路径(节选)

1、大型企业数字化升级的结构

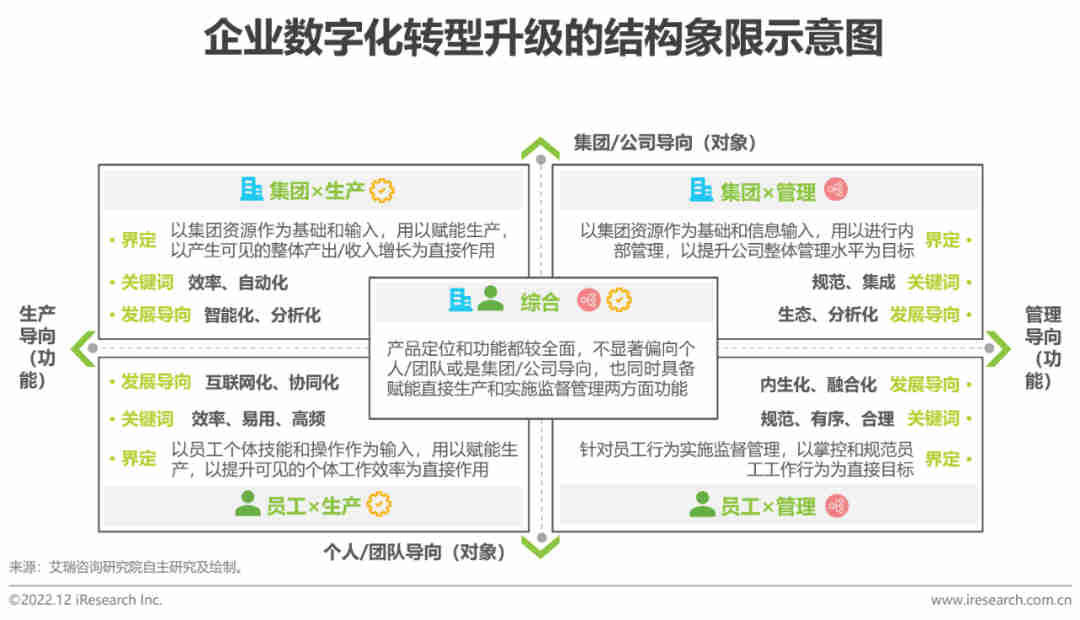

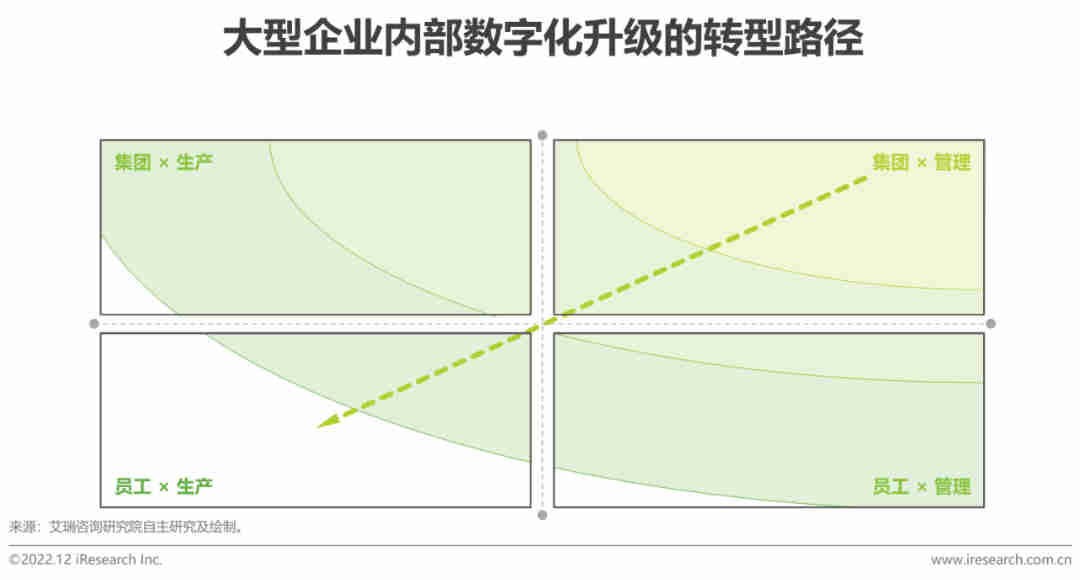

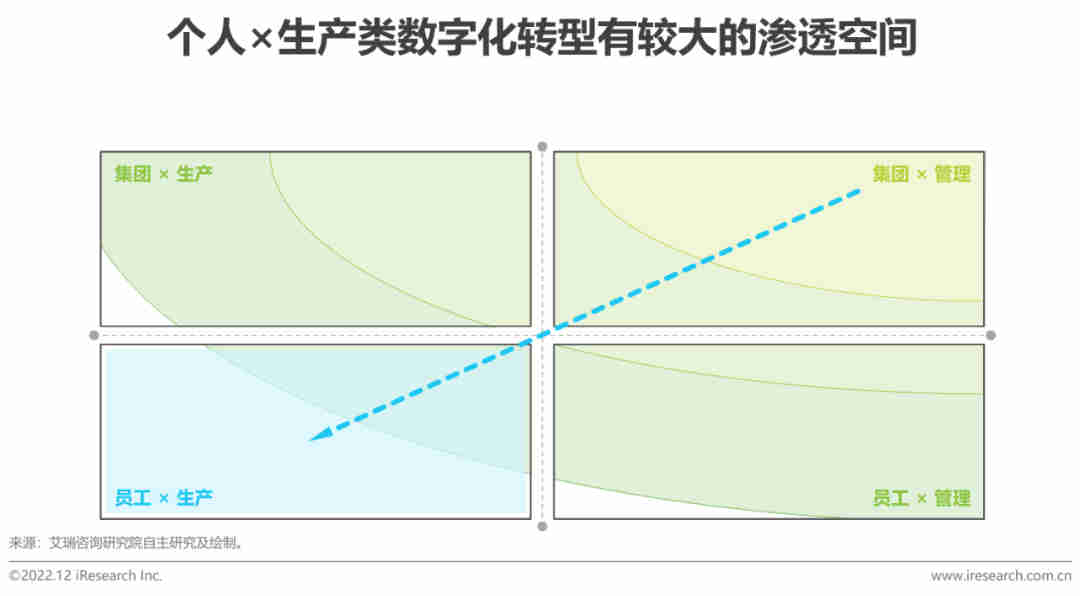

根据需求的对象和功能属性,数字化结构可分为四象限

根据数字化需求面向的直接对象与核心功能两方面的属性,企业数字化需求的结构可分为四个象限。在对象属性上,数字化升级可能是面向集团/公司或者面向个人/团队(统称员工),二者的核心区别在于使用的信息来源,例如:企业财务信息软件所收集和分析的是企业经营活动中产生的财务数据,因此属于面向集团/公司的产品,而IM的信息来源是员工个人的沟通和交流,因此属于面向员工的产品。在功能属性上,数字化升级或是服务于管理,或是服务于生产,二者的核心区别在于前者以提升可见的产出收入或工作效率为目标,而后者的核心功能通常是提升管理水平、降本增效等。

2、大型企业数字化升级的内部路径

数字化升级以“集团×管理”为基础呈波状路径渗透

站在甲方视角上看,大型企业内部的数字化历程普遍以“集团×管理”象限为基础和起点,向“集团×生产”和“员工×管理”两个象限扩散,最后向“员工×生产”渗透的“波状”路径。“集团×管理”象限的转型工作是大型企业数字化的基础,核心是集团业务流程、管理流程的数字化和数据化;企业在打好数字化基础之后,以“集团”和“管理”两大关键词为核心,分别将集团层面的数字化转型由管理拓展到生产流程,并将企业的管理工作由集团层面向员工个体层面细化和下沉,无论是从数字化产品的功能扩展路径还是从企业的组织流程适配上,都是水到渠成、顺理成章。本报告所示的路径图代表大型企业在逐步完善数字化建设过程中的一种普遍方式,对于特定的企业或者行业可能存在别的方式,例如,早期开展数字化转型的制造企业,属于集团×生产的工业软件升级可能是与管理的数字化升级同步开启的。

3、大型企业数字化产业历程

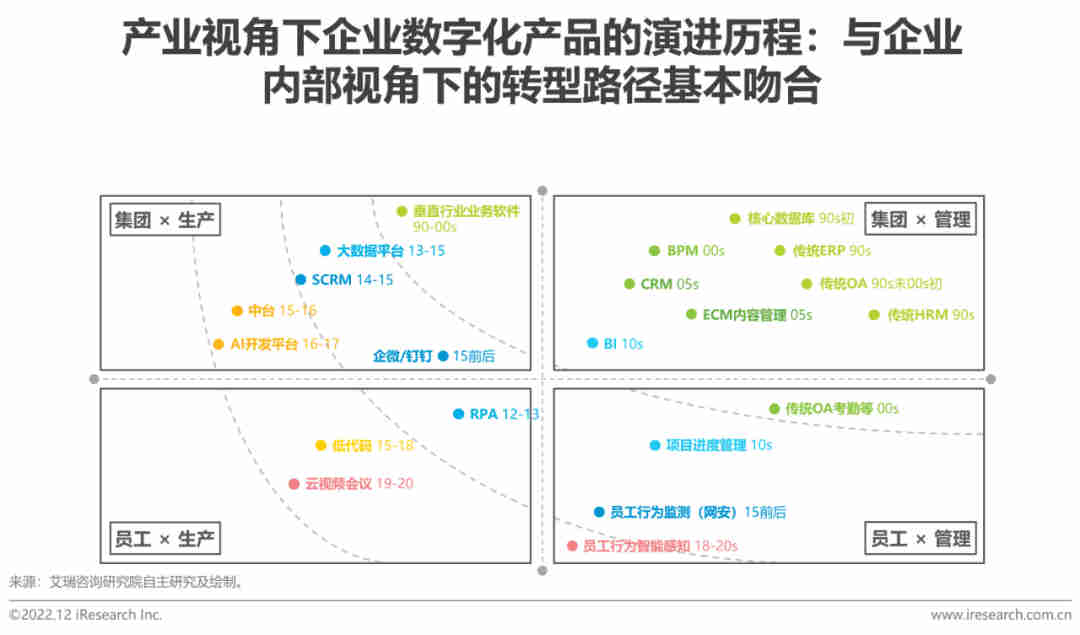

数字化产业的演进历程与企业内部的转型升级路径基本吻合

如果将中国数字化产业的发展历程按照产品、分类和应用时间进行匹配,可以显示30年来中国企业数字化需求的演进,如下图所示。前文已经论述,在国内市场上,大型企业是数字化转型的需求主体,因此,产业视角下市场需求的演进某种程度上也反映了国内大型企业整体的需求演进。将宏观视角的数字化产业历程和微观视角下的企业内部转型路径进行比对,可见二者的波状渗透路径非常相似,均为从“集团×管理”象限向“集团×生产”并“员工×管理”两象限推进,最后向“员工×生产”渗透的过程——这也印证了前文所描述的大型企业数字化转型升级路径的合理性。值得注意的是,本页所示路径主要列示的是不同大类的数字产品应用的时间,对于产品本身的演化升级并没有重新列出,近年来在AI、大数据等技术的驱动下,许多数字产品的形态、功能都出现了明显的变化,对于这些变化的原因和表现,本报告后文会有所涉及。

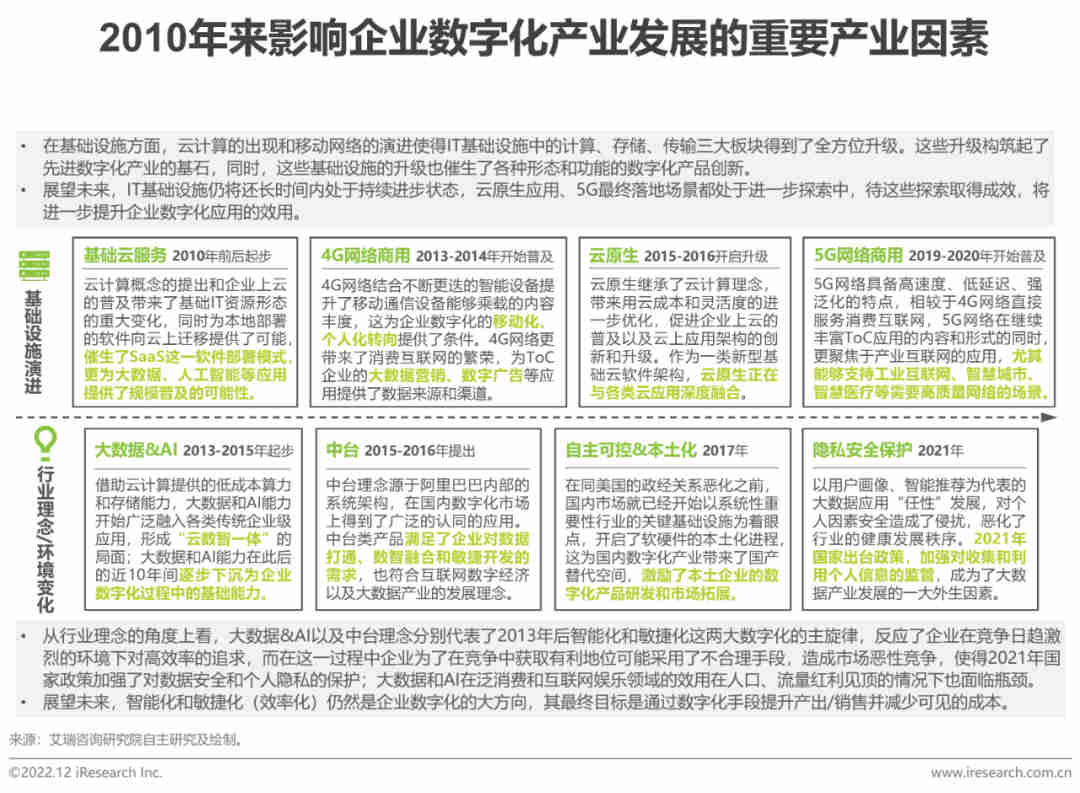

基础设施与行业理念的推陈出新影响数字化发展方向

电子化 / 数据化 / 智能化代表了国内数字化理念和目标演进

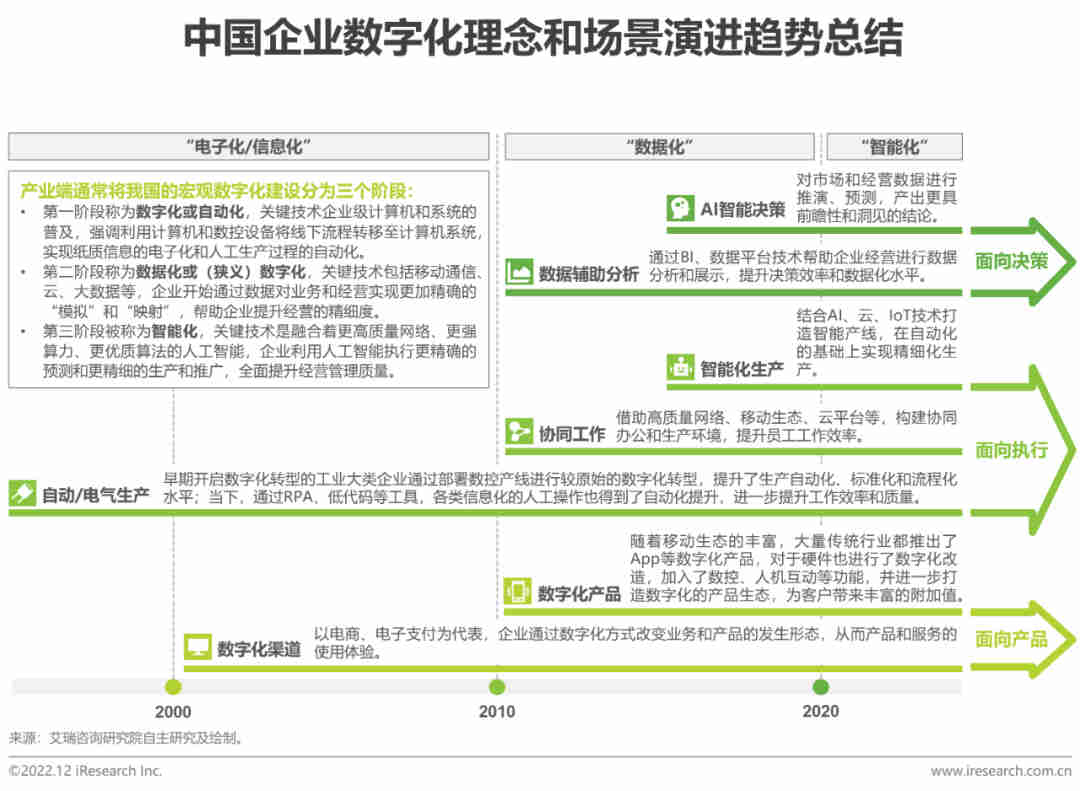

4、数字化路径走向

生产力导向的数字化工具将收获更多重视

建议关注“员工×生产”类数字化转型板块

基于本节内容描述的大型企业数字化转型结构和路径,从市场整体上看,国内的大型企业在过去20年间基本上已经完成了集团层面以及管理导向的数字化部署。如果将前文描述的波状路径理解为大型企业数字化转型的一个周期,那么在这样一个周期内的后期,结合当前的宏观经济环境,我们认为企业将在现有基础上继续夯实集团×生产类的应用和转型,并将结合业务形态深入强化员工×生产类的工具升级,2022年受到海外一级市场广泛关注的Figma、Notion等均可看做这一领域的代表性产品,在国内市场上,一方面,我们认为未来市场上将会出现越来越多的协同工具和员工生产力平台;另一方面,对于现有的数字化产品而言,为了满足企业需求,参考员工×生产类工具的选型要素,着重提升产品的协同性、可操作性以及提效水平也将成为升级更迭的重要方向。

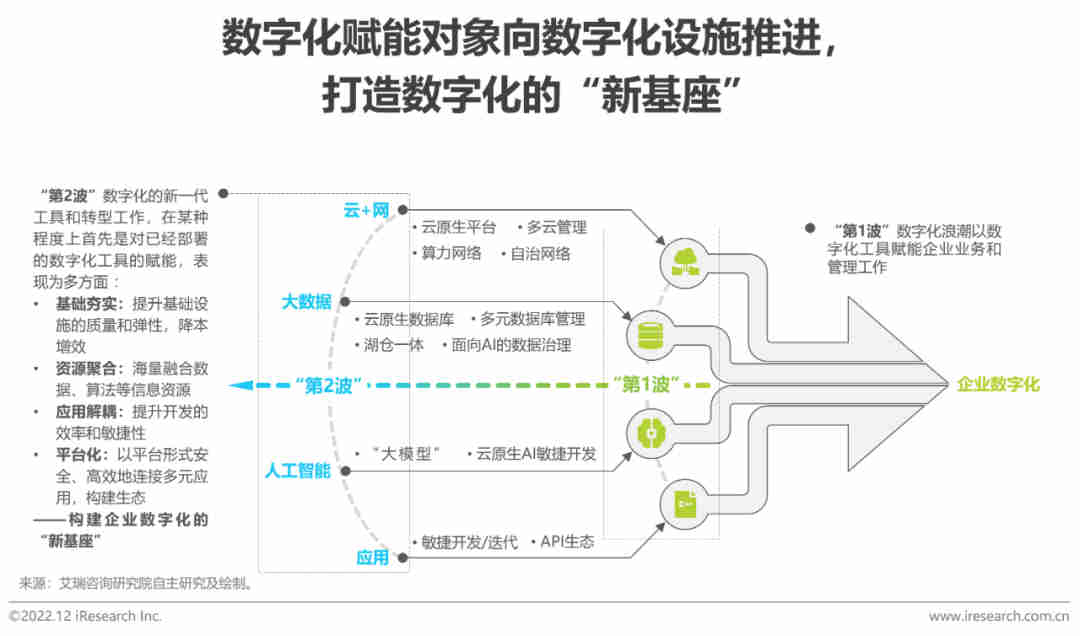

新兴技术迭代沉降,构建大型企业的数字化“新基座”

将前文所述的从“集团×管理”象限向“集团×生产”并“员工×管理”两象限推进,最后向“员工×生产”渗透的波状路径界定为大型企业数字化的一个周期,国内大型企业数字化转型工作大多已经来到“第1波”的中后期,而数字化进程领先的企业正在开启“第2波”。2020年前后,国家政策企业数字化各领域的头部服务商频繁提及 “新基建”、“新基座”、“数字化底座”、“智慧大脑”一类的概念,强调数字化服务更加体系化、数据化、智能化,我们认为这正对应着数字化工作较为领先的大型企业在新周期中的需求:进一步发挥数据对经营管理的“映射”能力,并将复合、零散的IT资源和应用有机聚合起来,并能够根据企业灵活的需求进行实时的开发、优化和迭代——要具备这些能力,大型企业正需要一个大容量、高弹性、生态开放的数字化“新基座”。

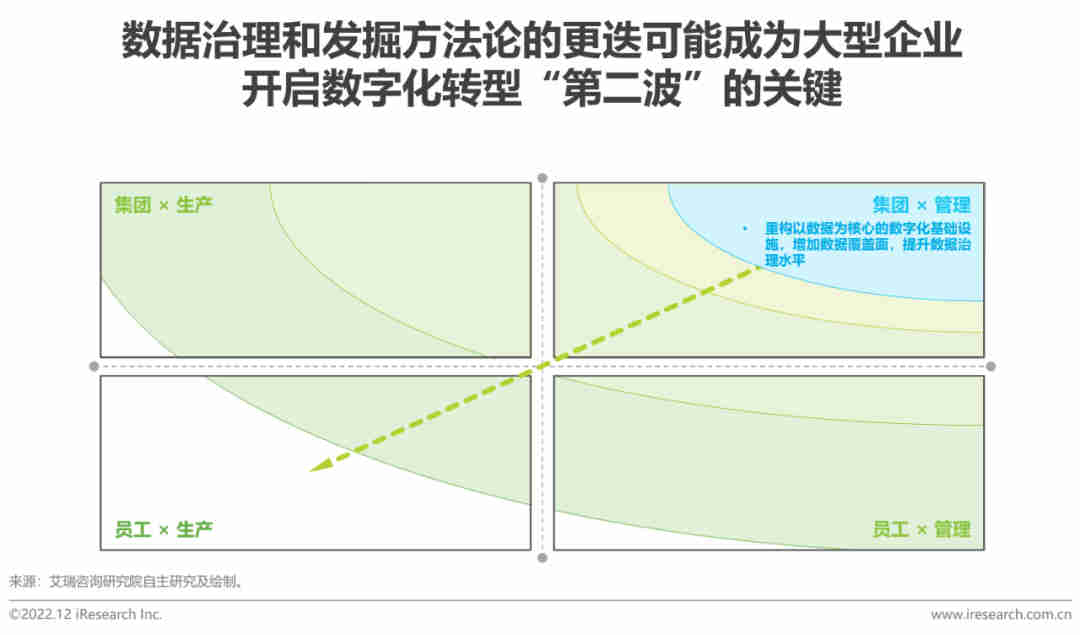

“新基座”的建设以数据治理和发掘方法论的更迭为起点

对照前文所述的大型企业数字化产业历程,我们认为大型企业数字化的“第一波”是电子化/信息化建设,并开始向全面数据化靠拢,而“第二波”代表的必然是智能化的深入,这也是国家政策及产业端推广数字化“新基建”的核心关键。正如“数据化”衔接着数字化产业的电子化/信息化阶段和智能化阶段,数据治理和挖掘方法论的转变也代表着企业数字化从“第一波”走向“第二波”的深化,企业对待数据的态度更多地从“存”转变为“用”,数据治理的方法论从面向人到面向机器(AI),这将在数据收集、数据存储、数据治理、数据开发等方面表现出来,企业会对AIoT基础设施、赋能AI的数据存储和治理平台、具备实时分析能力的经分工具产生更加明确的需求。

三、大型企业数字化产业的市场特征(节选)

本节内容站在数字化市场的乙方和产业市场视角,列举大型企业在购买数字化产品、开展数字化转型的过程中表现出的通用特征,阐明这些特征对国内数字化产业形态、发展方式带来的影响,并为准备面向大型企业客户进行拓客的乙方企业提出了一些建议。

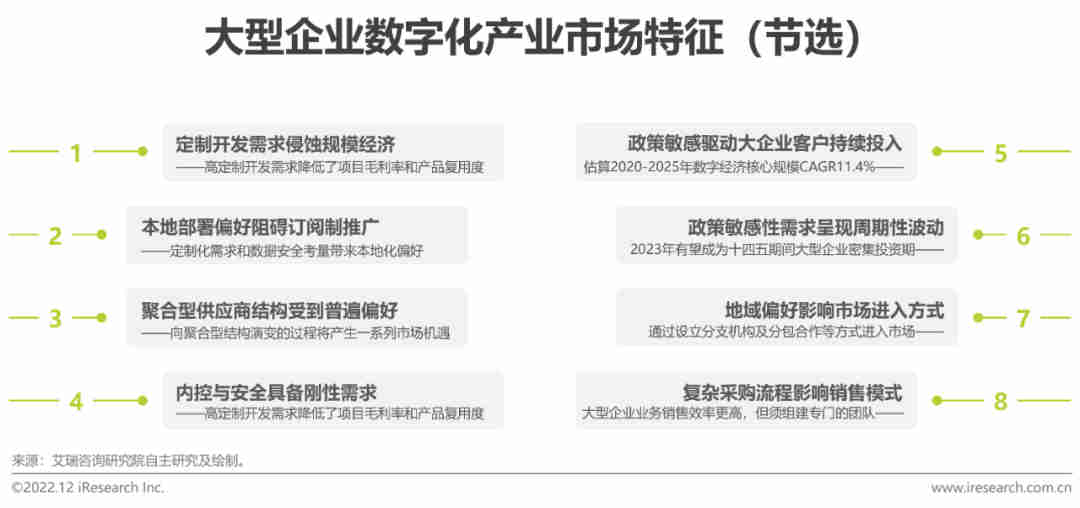

1、本地部署偏好阻碍订阅制推广

定制化需求和数据安全考量带来了大型企业的本地化偏好

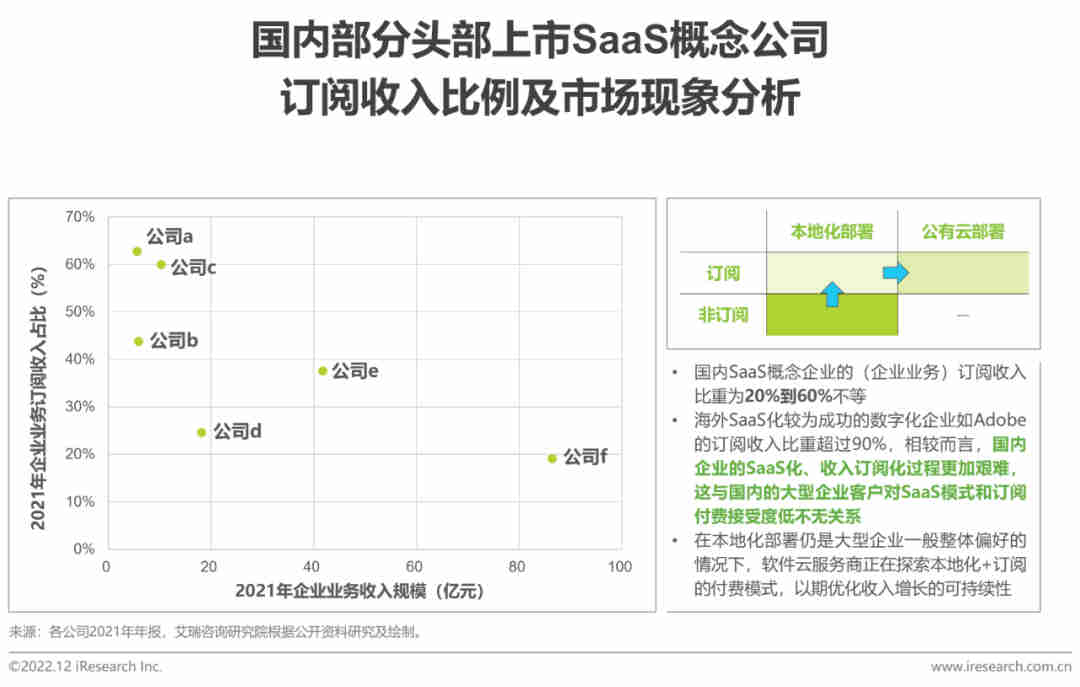

大型企业客户偏好软件进行本地化部署而非SaaS部署,这是大型企业数字化领域相对中小企业的重要差异。大型企业的本地化偏好首先来源于前文所述的定制化开发需求,其次也是大型企业看重数据安全的结果。相较于海外的头部SaaS公司的以及SaaS化转型较为成功的软件公司,国内SaaS概念公司在扩大订阅收入比重方面面临相当困难,这与国内大型企业客户对SaaS模式和订阅付费接受度低不无关系,并且这一现状在短时间内预计不会发生改变,为了优化软件业务收入的可持续性,部分软件企业正在开始尝试在本地化部署基础上推行订阅制收费。

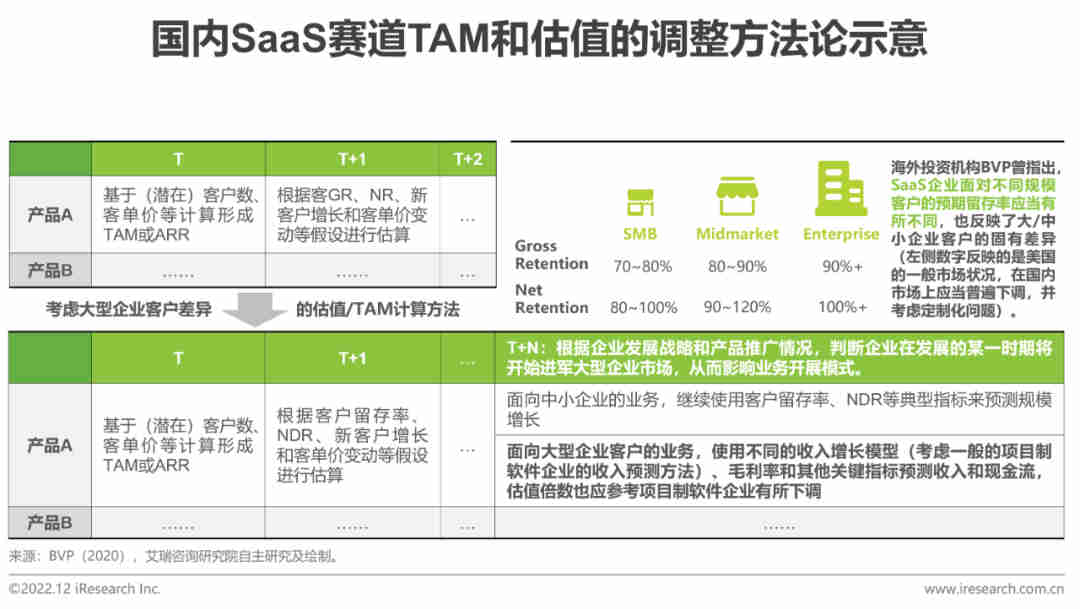

国内SaaS赛道TAM和估值应在对标海外市场的基础上调整

国内大型企业对本地化部署的偏好也应当影响一级市场的分析和估值。以企业级SaaS行业为例,一级市场对SaaS企业的估值普遍对标美国市场选取可比财务指标和估值倍数,我们认为这种方法没有充分考虑中美数字化市场的差异。下图展示了一种针对这两个市场的差异进行企业估值/赛道TAM计算的调整思路,其核心思想是:(除非企业管理层完全没有做大型企业业务的规划)默认SaaS企业在增长的某一时期会转向服务大型企业,此后将中小企业和大型企业的增长分别估算,对后者,应类比项目制软件企业的采用与纯SaaS企业不同的增长模型、财务指标和估值指标,避免在经典SaaS模型下高估企业收入前景和市场天花板(导致国内外SaaS市场差异的应有其他关键因素如企业付费意愿等,此处不做详细讨论)。

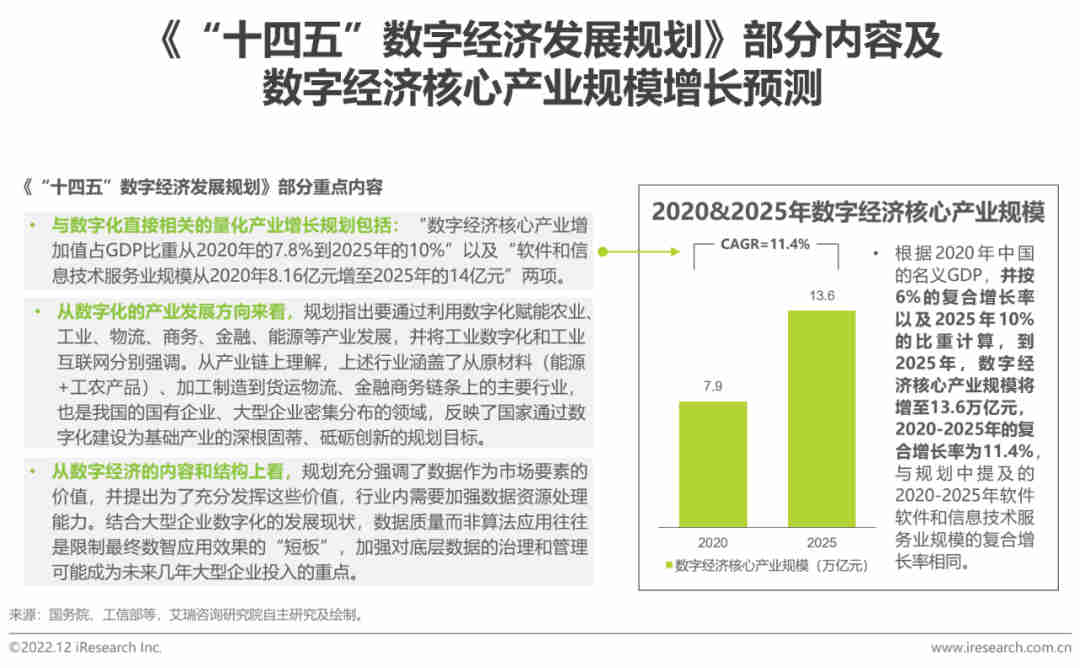

2、政策敏感驱动大企业客户持续投入

估算2020-2025年数字经济核心产业规模目标CAGR为11.4%

大型企业——尤其是国资企业对政策风向较为敏感,包括数字化在内的政策会优先给大型企业的数字化转型形成激励,驱动大型企业持续进行数字化投入,典型行业包括金融、工业制造等。2021年,我国首次发布聚焦数字经济领域的五年规划,可见数字经济正在受到政策规划部门更多的重视。下图展示了规划的部分重点内容,并对规划中提及的数字经济量化指标进行了明确:根据规划目标计算,2020-2025年数字经济核心产业规模的复合增速为11.4%,这在一定程度上也可以反应大型企业数字化投入的平均增速。

3、政策敏感性需求呈现周期性波动

2023年有望成为“十四五”期间大型企业密集投资期

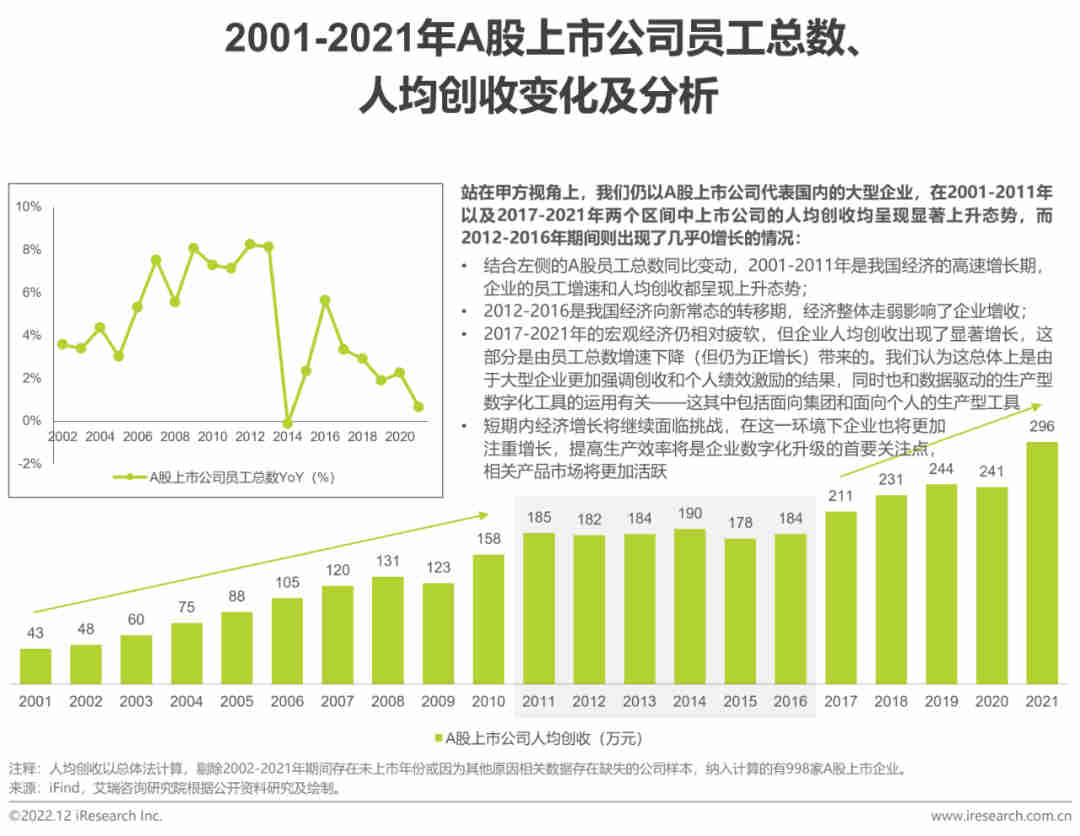

我们仍用A股上市公司来代表国内大型企业,观察财务报表“购建固定无形和长期资产支付的现金”一项(通常反应企业的长期资产性投资),可见国内大型企业的投资周期与五年规划为代表的政策周期存在一定关联。除“十二五”期间宏观经济向“新常态”切换从而影响企业的整体投资外,近20年的其余三个五年规(计)划期间,现金支付均在中间年份处于同比增速高位。尽管企业为数字化转型升级购置的产品服务不一定以上述口径核算,但这一趋势仍然反应了大型企业的资产性投资存在政策引导下的周期性。考虑企业支付大型订单普遍存在的之后,我们认为五年规划期的第2、3年是大型企业受包括“五年规划”在内的政策引导,密集开展长期资产投资的时期。2021年是“十四五”起始之年,叠加二十大政策激励,我们认为2023年有望成为大型企业的密集进行资产投资的时期,数字化市场也有望从中受益。

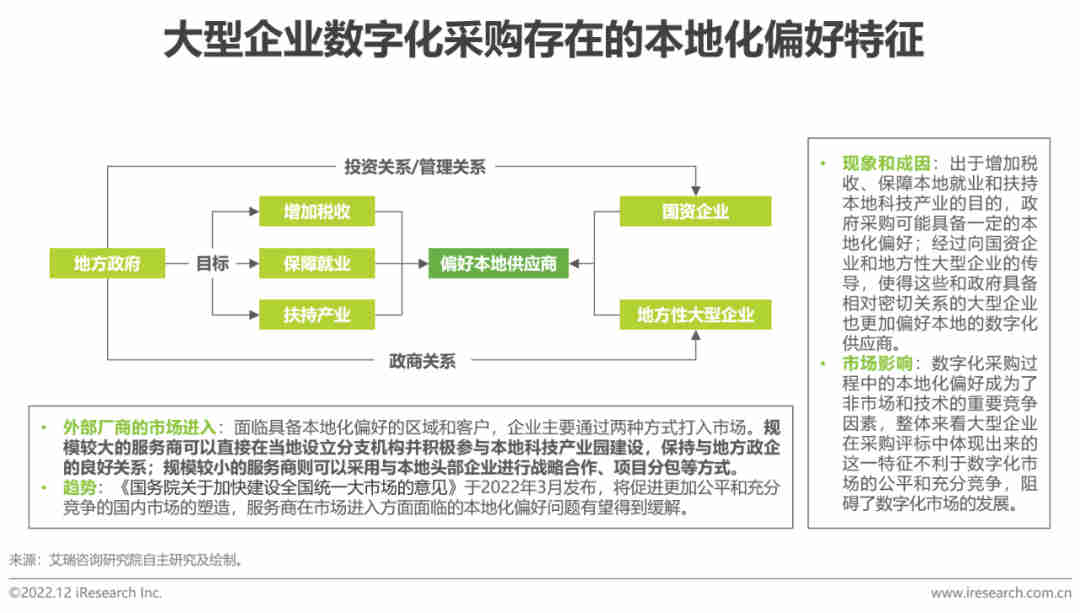

4、地域偏好影响市场进入方式

大/小型服务商分别可通过设立分支机构及分包合作等方式进入市场

地方性的大型企业和国资背景的企业与政府具有比较密切的关系,从而其采购行为也表现出一定的本地化偏好特征,这种现象普遍存在于各行业,数字化领域由于属于受到政策普遍鼓励和扶持的高新科技行业,更加受到关注。从服务商视角看,如果数字化企业希望进入某存在本地化偏好的市场或大型企业,大型服务商可以选择设立本地分支机构并积极参与科技产业园的建设来维护与地方政企的关系,小型服务商可以通过与当地头部企业进行分包合作等方式来参与大规模的项目,为自身积累项目经验和资源。

四、二十大政策解读&企业数字化八大趋势(节选)

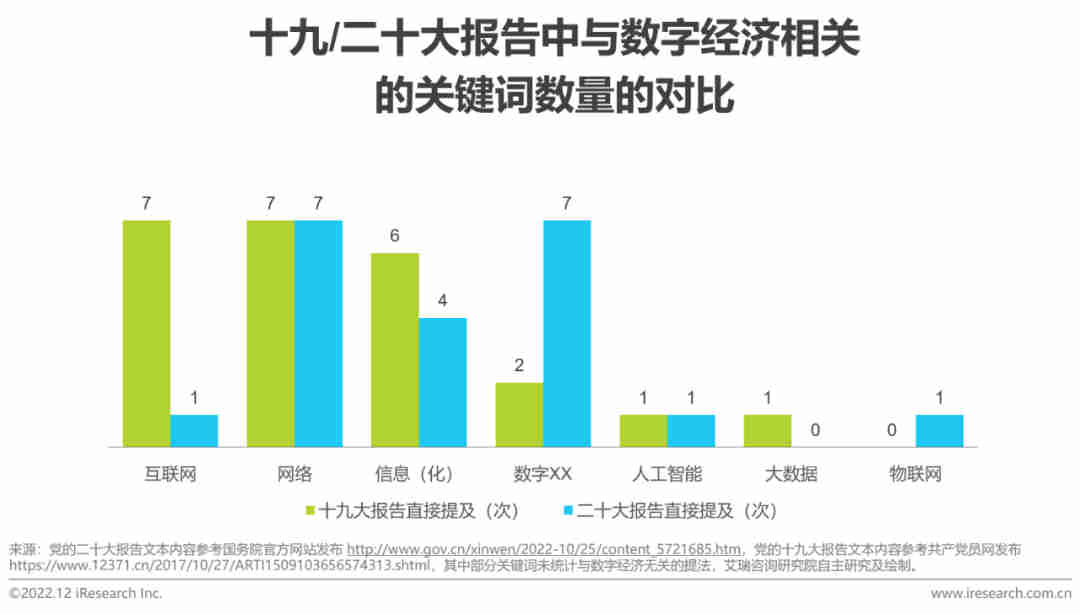

1、十九/二十大报告相关关键词数量

“数字XX”提及数量增加,产业数字化在数字产业中重要性有所提升

我们对十九和二十大报告中出现的与数字经济直接相关的关键词进行了统计,其中,“数字XX”类提法从2次上升为7次,我们认为主要是由于报告对具体产业的数字化转型工作提出了更直接的关注,例如“数字物流”和“文化数字化”等;直接提及“互联网”的次数从7次下降为1次,我们认为主要是由于近年来消费互联网产业经历了多年高速发展后趋于成熟,未来与消费互联网相关的监管和扶持工作或将更多围绕优化网络环境、治理网络生态来开展。在一定程度上,上述两组关键词被提及数量的变化反映了数字经济的发展重心由ToC向ToB的倾斜,数字化转型将进一步成为我国企业提升生产力和生产效率的关键驱动力。

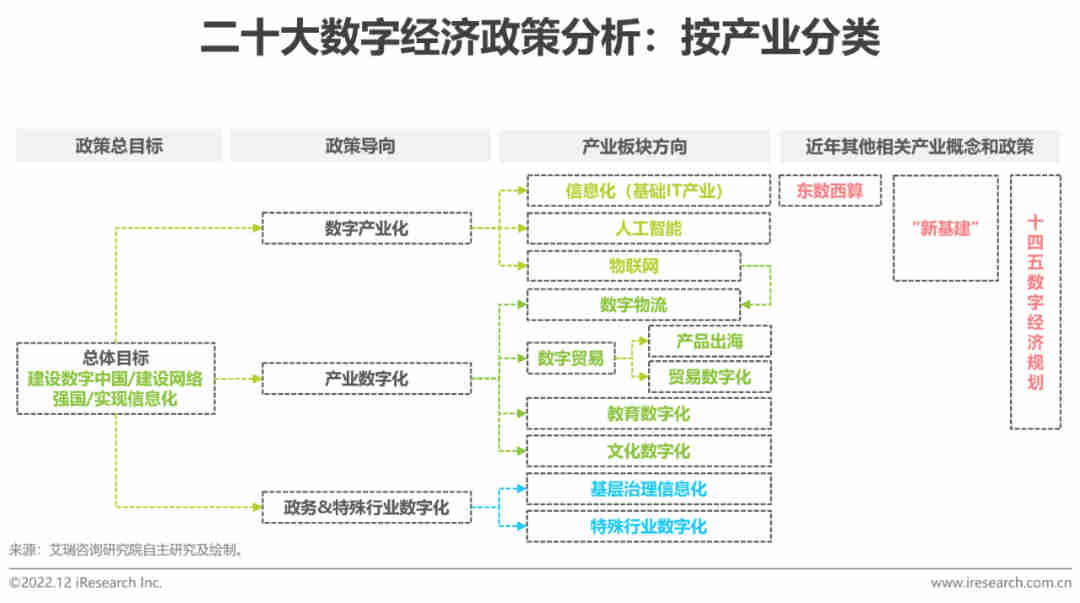

2、二十大数字经济政策分析

细分数字产业化、产业数字化、政务等行业数字化三大领域

我们对二十大报告中直接提及的与数字经济相关的政策表述进行了分类,大致可以分为数字产业化、产业数字化、政务&特殊行业数字化三大领域:数字产业化包括基础信息化、人工智能和物联网产业;产业数字化领域包括数字物流、数字贸易、教育数字化和文化数字化产业;其中,文化数字化概念首次出现在党的二十大报告中;其他领域包括政务数字化和特殊行业数字化。近年来,“东数西算”、“新基建”、十四五数字经济规划等长期政策对上述领域也有所涉及,预计多项政策重合度高的领域可能成为未来政策进一步支持的发力点。聚焦到我国企业数字化市场中来看,“产业数字化”板块中涉及行业的头部企业将有限受到政策激励,相关数字化产业有望得到优先发展。

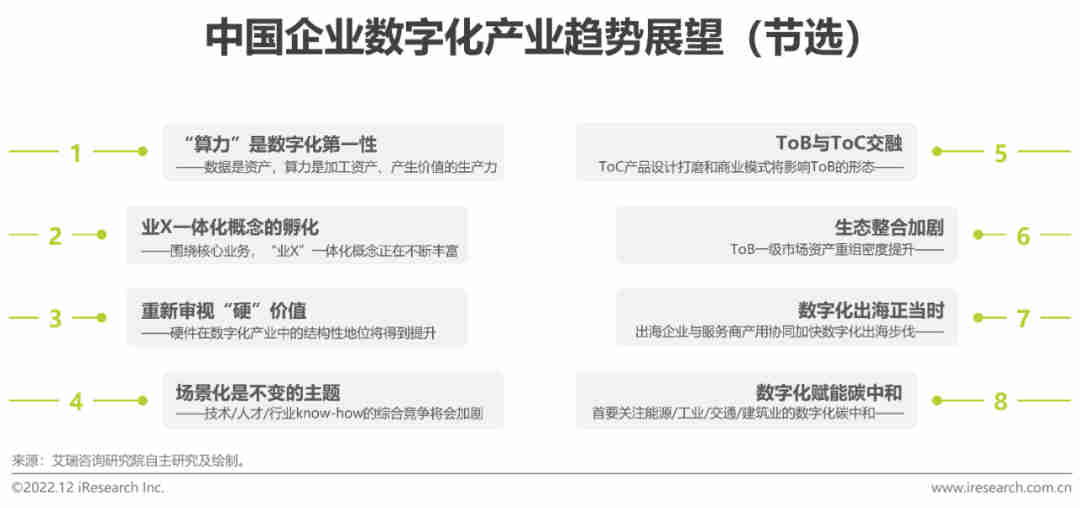

本节内容综合了企业、供应商、投资者等多重视角,总结了中国企业数字化产业未来发展的八大趋势,包括:

趋势1:“算力”是数字化第一性

数据是资产,算力是加工资产、产生价值的生产力

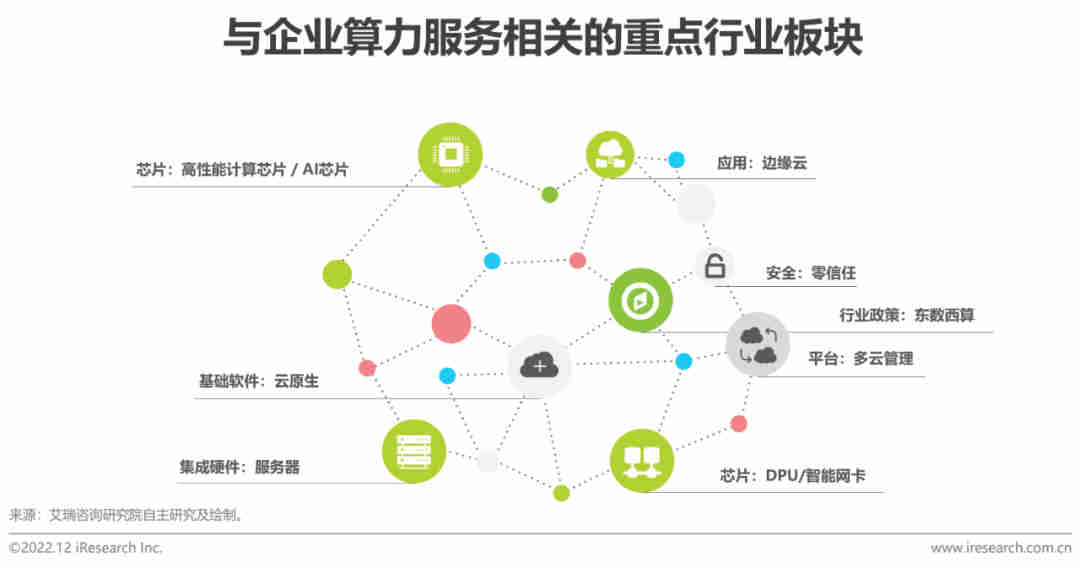

参考本报告前文所述的行业发展历程,随着企业数字化阶段从“信息化、电子化”发展到“数据化”和“智能化”阶段,数据作为企业“资产”的地位更加明确,与此同时,算力的作为企业“生产力”地位也会更加明确。我们认为高性能的算力是企业数字化由“数据化”阶段完全迈入“智能化”阶段的关键,只有当企业能够以极低的成本获取高质量算力,基于数据的各类应用才能能够得到充分的开发和探索——提高算力性能,需要依靠计算用基础软硬件的更新迭代,在国产化替代紧迫性不断提升的背景下,计算芯片产业的战略重要性将得到不断提升;降低算力价格,除了依靠硬件升级提升算力供给之外,还需要算力部署以及利用方式的升级——云原生应用、边缘云以及今年提出的“东数西算”政策都有利于从各方面降低算力成本。

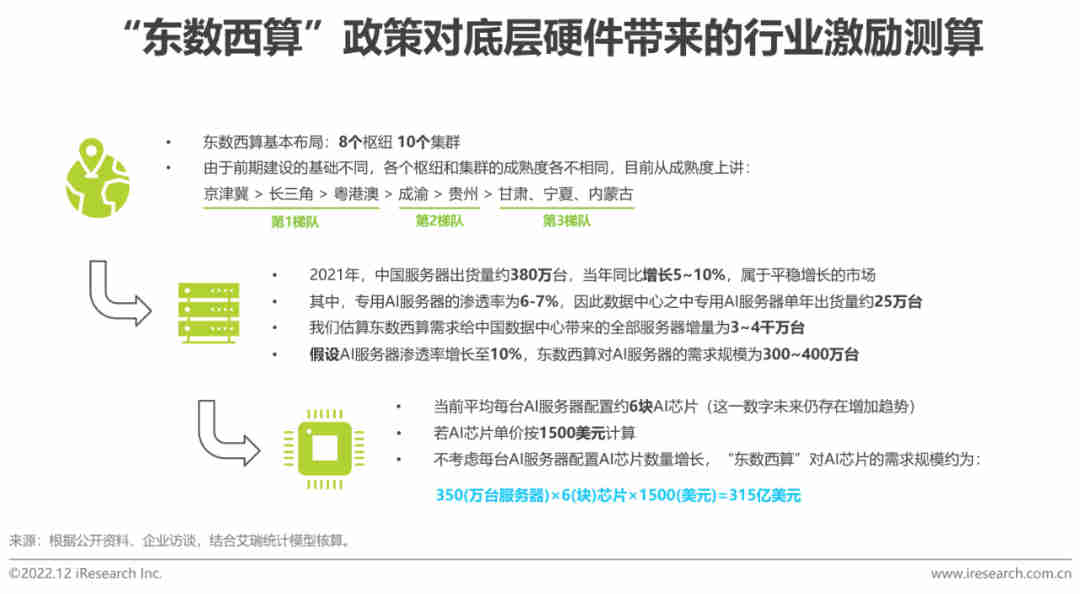

附:“东数西算”行业增量测算

东数西算将带来3至4千万台服务器需求,对AI芯片的需求量将超过300亿美元

2022年2月,发展改革委等部门联合印发文件,提出京津冀、长三角、粤港澳大湾区、成渝、内蒙古、贵州、甘肃、宁夏启动建设国家算力枢纽节点,并规划了10个国家数据中心集群,标志着“东数西算”工程正式启动。“东数西算”是服务于数字经济算力升级的大规模基建项目,将对多种基础IT软硬件需求产生有力的推动。下图中我们对“东数西算”给服务器以及AI芯片产业带来市场推动作用进行了测算。

趋势2:业X一体化概念的孵化

围绕核心业务需求,各类“业X”一体化概念正在不断丰富

近年来不断有企业以“业X一体化”为理念推出新产品和构建产品服务矩阵,我们认为这反映的是随着市场对数字化认知的不断深入,客户越来越不满足于“为数字化而数字化”,而是需要看到数字化投入给企业业务带来的效果,也就是本报告前文所强调的“生产导向”。业务由员工执行、通过财务数据进行反映、频繁涉及合同缔约、需要IT系统的支持,市场上已存在的几类“业X一体化”正是围绕与企业业务密切相关的这几个部门和环节,借助数字化渠道来提升业务部门和其他部门的协同效率,利用大数据洞察来提升企业决策的正确性,从而体现数字化给企业业务带来的赋能价值。

翻译:

Lead:

This report focuses on the digital transformation market of domestic large enterprises. The first chapter of the report reviews the digital market of Chinese large enterprises from an empirical perspective, and analyzes the main digital strategies of large enterprises in various industries in recent years. The second chapter of the report combines the steps of internal digital development of a single enterprise and the overall path of digital industry evolution, and analyzes the ways, paths and structures of digital transformation and upgrading of domestic large enterprises. The third chapter of the report enumerates the representative characteristics of the digital market of large enterprises and its impact on the market form and behavior. The fifth chapter of the report looks forward to the future development trend of the digital market of Chinese enterprises.

Overview of the Digital Market of China’s Large Enterprises (Excerpt)

Market size

In 2021, large enterprises will spend 2.8 trillion yuan on digitization, with a compound growth rate of 12.3% expected in the next five years

According to iResearch, the digital expenditure scale of large Chinese enterprises in 2021 is about 2.8 trillion yuan, and it is estimated that the average compound growth rate of digital expenditure of large Chinese enterprises in 2021-2026 will reach 12.3%. Due to the impact of COVID-19 and macroeconomic growth, the growth rate of digital spending by large enterprises will fluctuate in 2020 and 2022, and the market is expected to recover in 2023. On the whole, due to the relatively rigid demand for digital transformation of large enterprises and their strong ability to carry risks, the overall growth of the market is stable.

Industry Map

Structure and Path of Digital Upgrading of Large Enterprises (Excerpt)

Structure of digital upgrading of large enterprises

The digital structure can be divided into four quadrants according to the required objects and functional attributes

According to the attributes of direct object and core function, the structure of enterprise digitization demand can be divided into four quadrants. In terms of object attributes, digital upgrades may be oriented towards groups/companies or individuals/teams (collectively referred to as employees), the core difference between the two is the information sources used, such as: Enterprise financial information software collects and analyzes the financial data generated in the business activities of enterprises, so it is a product for the group/company, while IM information source is the communication and exchange of employees, so it is a product for employees. In terms of functional attributes, digital upgrading serves either management or production. The core difference between the two lies in that the former aims to improve visible output income or work efficiency, while the latter’s core function is usually to improve management level, reduce cost and increase efficiency.

Internal path of digital upgrade of large enterprises

On the basis of “group x management”, the digital upgrade penetrates in a wavy path

From the perspective of Party A, the digital process within large enterprises is generally based on and starting from the “group × management” quadrant, spreading to the “group × production” and “staff × management” quadrangles, and finally to the “wavy” path of “staff × production” penetration. The transformation work of “group x management” quadrant is the basis of digitalization of large enterprises, and the core is the digitalization and data of group business process and management process.

After laying the digital foundation, the enterprise takes the two key words “group” and “management” as the core, respectively expanding the digital transformation at the group level from management to production process, and refining and sinking the enterprise management from the group level to the individual level of employees, no matter from the function expansion path of digital products or from the enterprise’s organizational process adaptation. It all comes naturally. The path map shown in this report represents a common approach for large enterprises in the process of gradually improving digital construction. For specific enterprises or industries, there may be other approaches. For example, for manufacturing enterprises that have carried out digital transformation in the early stage, industrial software upgrading belonging to group X production may be initiated simultaneously with the digital upgrading of management.

Digital industry history of large enterprises

The evolution of digital industry is basically consistent with the internal transformation and upgrading path of enterprises

If the development process of China’s digital industry is matched according to product, classification and application time, it can show the evolution of Chinese enterprises’ digital demand in the past 30 years, as shown in the figure below. As has been discussed above, in the domestic market, large enterprises are the main body of demand for digital transformation. Therefore, the evolution of market demand from the perspective of industry also reflects the evolution of the overall demand of large domestic enterprises to some extent.

By comparing the digital industry process from the macro perspective with the enterprise internal transformation path from the micro perspective, it can be seen that the wavy penetration paths of the two are very similar, both advancing from “group × management” quadrant to “group × production” and “staff × management” quadrant. Finally, the process of penetration into “employees × production” also confirms the rationality of the digital transformation and upgrading path of large enterprises described above. It is worth noting that the path shown on this page mainly lists the application time of different categories of digital products, and does not re-list the evolution and upgrading of the products themselves. In recent years, driven by AI, big data and other technologies, the form and function of many digital products have changed significantly. The reasons and manifestations of these changes will be covered later in this report.

The innovation of infrastructure and industry concepts influences the direction of digital development

Digitization/digitization/intelligentization represents the evolution of domestic digitization concept and goal

Digital path trend

Productivity-oriented digital tools will get more attention

It is suggested to pay attention to the digital transformation plate of “employees × production”

Based on the structure and path of digital transformation of large enterprises described in this section, from the perspective of the market as a whole, domestic large enterprises have basically completed group-level and management-oriented digital deployment in the past 20 years. If the wavy path described above is understood as a cycle of digital transformation of large enterprises, then in the later period of such a cycle, combined with the current macroeconomic environment, we believe that the enterprise will continue to consolidate the application and transformation of group × production on the existing basis, and further strengthen the tool upgrade of staff × production on the basis of the business form.

Figma and Notion etc. that have received widespread attention in the overseas primary market in 2022 can be regarded as representative products in this field. In the domestic market, on the one hand, we believe that more and more collaboration tools and employee productivity platforms will appear in the future market. On the other hand, for the existing digital products, in order to meet the needs of enterprises, focusing on improving the coordination, operability and efficiency of products by referring to the selection elements of employee × production tools will also become an important direction of upgrading and changing.

Iterative settlement of emerging technologies to build a digital “new base” for large enterprises

The wave path of penetration from “group × management” quadrant to “group × production” and “staff × management” mentioned above, and finally to “staff × production”, is defined as a cycle of digitalization of large enterprises. Most of the digital transformation work of large domestic enterprises has come to the middle and late stage of the “first wave”. Companies that have taken the lead in digitization are starting the second wave. Around 2020, the leading service providers in various fields of digitalization of national policy enterprises frequently mention the concepts of “new infrastructure”, “new base”, “digital base” and “smart brain”, emphasizing that digital services are more systematic, digital and intelligent.

We believe that this corresponds to the needs of large enterprises with leading digitalization work in the new cycle: To further exert the “mapping” ability of data to operation and management, organically aggregate complex and scattered IT resources and applications, and carry out real-time development, optimization and iteration according to the flexible needs of enterprises — to have these capabilities, large enterprises are in need of a large capacity, high elasticity, ecological open digital “new base”.

The construction of “new base” starts with the change of data governance and mining methodology

In contrast to the digitalization industry process of large enterprises mentioned above, we believe that the “first wave” of digitalization of large enterprises is the construction of digitization/informatization, and begins to get closer to comprehensive data, while the “second wave” represents the deepening of intelligence, which is also the core of national policies and the promotion of digital “new infrastructure” at the industrial end.

Just as “digitization” connects the electronization/informatization stage and the intelligent stage of the digital industry, the transformation of data governance and mining methodology also represents the deepening of enterprise digitization from the “first wave” to the “second wave”, the attitude of enterprises towards data is more changed from “storage” to “use”, and the methodology of data governance is changed from human-oriented to machine-oriented (AI). This will be reflected in data collection, data storage, data governance, data development and other aspects. Enterprises will have more clear demands for AIoT infrastructure, AI-enabled data storage and governance platforms, and real-time analysis capabilities of the labor division tools.

Market Characteristics of Digital Industry of Large Enterprises (Excerpt)

From the perspective of Party B and the industrial market in the digital market. This section lists the common characteristics of large enterprises in the process of buying digital products and carrying out digital transformation, clarifies the influence of these characteristics on the form and development mode of the domestic digital industry. And puts forward some suggestions for Party B enterprises preparing to expand to large enterprise customers.

Local deployment preference hinders the promotion of subscription system

The need for customization and data security concerns have led to a preference for localization among large enterprises

Large enterprise customers prefer localized software deployment over SaaS deployment. Which is an important difference between large enterprises and smes in the digitalization space. The localization preference of large enterprises stems first from the need for customized development described above. And second from the importance large enterprises place on data security. Compared with overseas leading SaaS companies and software companies with successful SaaS transformation, domestic SaaS concept companies face difficulties in increasing the proportion of subscription revenue. This is related to the low acceptance of SaaS model and subscription payment by domestic large enterprise customers. And this situation is not expected to change in the short term. In order to optimize the sustainability of software business revenue. Some software companies are beginning to try to implement subscription fees on the basis of localized deployment.

Domestic SaaS track TAM and valuation should be adjusted on the basis of benchmarking overseas markets

The preference of large domestic enterprises for localized deployment should also influence primary market analysis and valuation. Taking the enterprise SaaS industry as an example, the primary market generally uses comparable financial indicators and valuation multiples against the US market. We believe that this approach does not fully consider the differences between the Chinese and American digital markets. The figure below shows a way to adjust the business valuation/track TAM calculation for the difference between the two markets.

The core idea is: (unless the enterprise management does not plan the business of large enterprises at all) it assumes that SaaS enterprises will switch to serving large enterprises in a certain period of growth. And then estimate the growth of small and medium-sized enterprises and large enterprises separately. For the latter, it should be similar to project-based software enterprises using different growth models, financial indicators and valuation indicators from pure SaaS enterprises. Avoid overestimating enterprise revenue prospects and market ceilings under the classic SaaS model (other key factors that lead to differences between domestic and foreign SaaS markets. Such as enterprise willingness to pay, will not be discussed in detail here).

Policy sensitivity drives continuous investment from large enterprise customers

It is estimated that the target CAGR of core industry scale of digital economy in 2020-2025 is 11.4%

Large enterprises, especially state-owned enterprises, are sensitive to the policy direction. Policies including digitalization will give priority to the digital transformation of large enterprises and drive them to continue digital investment. Typical industries include finance and industrial manufacturing. In 2021, China released its first five-year plan focusing on digital economy. Which shows that digital economy is receiving more attention from policy planning departments. The following figure shows some of the key contents of the plan and makes clear the quantitative indicators of digital economy mentioned in the plan:. Calculated according to the planning objectives. The composite growth rate of core industrial scale of digital economy in 2020-2025 is 11.4%. Which can also reflect the average growth rate of digital investment of large enterprises to some extent.

The demand for policy sensitivity fluctuates periodically

2023 is expected to be a period of intensive investment by large companies during the 14th Five-Year Plan period

We still use A-share listed companies to represent large domestic enterprises. By observing the item “cash paid for the purchase and construction of fixed intangible and long-term assets” in financial statements (usually reflecting the long-term asset investment of enterprises). We can see that the investment cycle of large domestic enterprises is somewhat related to the policy cycle represented by the five-year plan. In addition to the macroeconomic transition to the “new normal” during the 12th Five-Year Plan period. Which affected the overall investment of enterprises, cash payment in the other three five-year plan (plan) periods in the past 20 years all had a high year-on-year growth rate in the middle years.

Although the products and services purchased by enterprises for digital transformation and upgrading may not be accounted in the above caliber. This trend still reflects the policy-guided periodicity of asset investment of large enterprises. Considering the prevalence of large orders paid by enterprises. We believe that the second and third years of the five-year planning period will be a period of intensive long-term asset investment by large enterprises guided by policies including “five-year planning”. 2021 is the beginning year of the 14th Five-Year Plan. With the addition of 20 major policy incentives, we believe that 2023 is expected to become a period of intensive asset investment by large enterprises, from which the digital market is also expected to benefit.

Regional preferences affect market entry methods

Large and small service providers can enter the market by setting up branches and subcontracting

Large local enterprises and state-owned enterprises have a close relationship with the government. So their purchasing behaviors also show certain characteristics of localization preference. This phenomenon is widespread in all industries, And the digital field is more concerned because it belongs to the high-tech industry which is generally encouraged and supported by policies. From the perspective of service providers, if digital enterprises want to enter a certain market or large enterprises with localized preferences, large service providers can choose to set up local branches and actively participate in the construction of science and technology industrial park to maintain the relationship with local government and enterprises. While small service providers can participate in large-scale projects by subcontracting and cooperating with local leading enterprises. Accumulate project experience and resources for yourself.

Twenty Major Policy Interpretations & Eight Trends of Enterprise Digitization (Excerpt)

Number of relevant keywords in 19/20 reports

The number of references to “digital XX” has increased, and the importance of industrial digitalization in the digital industry has increased

We made statistics on the key words directly related to the digital economy in the 19th and 20th National Congress reports. Among them, the reference of “digital XX” increased from 2 times to 7 times, which we believe is mainly because the reports put forward more direct attention to the digital transformation of specific industries. Such as “digital logistics” and “cultural digitalization”. The number of direct mentions of “Internet” decreased from 7 to 1. Which we believe is mainly because the consumer Internet industry has become mature after years of rapid development in recent years.

In the future, the supervision and support work related to consumer Internet may focus more on the optimization of network environment and the governance of network ecology. To some extent, the change in the mentioned number of the above two groups of keywords reflects the trend of the development center of digital economy from ToC to ToB. Digital transformation will further become the key driving force for Chinese enterprises to improve the productivity and production efficiency.

Analysis of the top 20 digital economy policies

Subdivide digital industrialization, industry digitization, government and other industry digitization three areas

We classify the policy statements directly mentioned in the top 20 reports related to the digital economy. Which can be roughly divided into three areas: digital industrialization, industrial digitization, and digitization of government and special industries. Digital industrialization includes basic informatization, artificial intelligence and the Internet of Things industry. The industry digitization field includes digital logistics, digital trade, education digitization and culture digitization industry; Among them. The concept of cultural digitization appeared for the first time in the Party’s twenty National Congress report. Other areas include digitization of government affairs and special industries.

In recent years, long-term policies such as “counting in the East and counting in the West”, “new infrastructure”. And the 145th Digital economy Plan have also covered the above areas. It is expected that the areas with a high degree of policy overlap may become the power points for further policy support in the future. Focusing on the digital market of Chinese enterprises. The head enterprises involved in the “industry digitalization” plate will be limited by policy incentives. And the related digital industries are expected to get priority development.

Based on the perspectives of enterprises, suppliers and investors. This section summarizes eight trends of the future development of digital industry of Chinese enterprises, including:

Trend 1: “Computing power” is digital first

Data is an asset, and computing power is the productive forces that process assets and produce value

With reference to the industry development process mentioned above in this report. As the enterprise digitization stage develops from “informatization and electronization” to “digitization” and “intelligence” stage. The status of data as enterprise “assets” is more clear. Meanwhile, the status of computing power as enterprise “productivity” will also be more clear. We believe that high-performance computing power is the key for enterprises to move from the “digitalization” stage to the “intellectualization” stage. Only when enterprises can obtain high-quality computing power at a very low cost. Various data-based applications can be fully developed and explored.

To improve computing performance, it needs to rely on the updating and iteration of basic computing software and hardware. Under the background of the increasing urgency of localization substitution. The strategic importance of the computing chip industry will be continuously enhanced. To reduce the price of computing power, in addition to improving the supply of computing power by upgrading the hardware. We also need to upgrade the deployment and utilization of computing power. Cloud native application, edge cloud and the policy of “counting in the East and counting in the west”. Proposed this year are conducive to reducing the cost of computing power from all aspects.

Attached: “East count west count” industry increment calculation

This will create demand for 30 to 40 million servers and demand for AI chips will exceed $30 billion

In February 2022, the National Development and Reform Commission and other departments jointly issued a document, proposing to start construction of national computing hub nodes in Beijing-Tianjin-Hebei, Yangtze River Delta, Guangdong-Hong Kong-Macao Greater Bay Area, Chengdu-Chongqing, Inner Mongolia, Guizhou, Gansu and Ningxia. And planning 10 national data center clusters, marking the official launch of the “East data and West computing” project. “Counting in the East and counting in the West” is a large-scale infrastructure project that serves to upgrade the computing power of the digital economy and will strongly promote the demand for a variety of basic IT hardware and software. In the chart below, we measure the impact of “counting East and counting west” on the server and AI chip industries.

Trend 2: Incubation of industry-X integration concepts

Around the core business needs, various “industry X” integration concepts are constantly enriched

In recent years, more and more enterprises have launched new products and constructed product service matrix based on the concept of “industry X integration”. We believe that this reflects that with the deepening of the market’s awareness of digitalization. Customers are increasingly not satisfied with “digitalization for digitalization’s sake”. But need to see the effect of digitalization investment on enterprise business. Which is the “production-oriented” emphasized in the previous part of this report. Business is carried out by employees, reflected through financial data. Frequently involved in contract making, and needs the support of IT system.

Several types of “industry-X integration” existing in the market are precisely centered on these departments and links closely related to enterprise business. And enhance the collaborative efficiency of business departments and other departments with the help of digital channels. Big data insight is used to improve the correctness of enterprise decisions. So as to reflect the enabling value brought by digitalization to enterprise business.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:艾瑞咨询;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。