当前,数字经济已成为推动经济社会高质量发展、提质增效的重要力量。党的二十大报告提出,要加快发展数字经济,促进数字经济和实体经济深度融合。数字经济时代需要大量的中小企业,而中小企业的创新突破往往与金融业的数字化转型相伴相生。近年来,随着数字技术与金融行业的快速融合,各商业银行纷纷布局,在积极运用数字技术提升银行服务效率、改善客户服务体验的同时,通过开放赋能的方式将金融服务融入企业特定场景,不仅能从整体上提高各类群体金融可得性,推动金融高质量发展,还有助于推动中小企业“上云、用数、赋智”。其中,推进开放银行建设就是非常重要的一环。

一、开放银行发展现状简析数字化转型网szhzxw.cn

根据高德纳(Gartner)咨询公司给出的定义,开放银行是一种平台化的商业模式,通过与商业生态系统共享数据、算法、交易、流程和其他业务功能,为商业生态系统的客户、员工、第三方开发者、金融科技公司、供应商和其他合作伙伴提供服务,使银行创造出新的价值,构建新的核心能力。

开放银行的理念最早于2014年由英国一家银行提出后,英国、澳大利亚、新加坡等国家的金融机构纷纷开展尝试,不久即在全球掀起了开放银行发展浪潮。从发展历程看,国外呈现出由监管部门驱动、自上而下的特征,比较典型的是英国和欧盟。2016年3月,英国财政部发布了《开放银行标准》,正式确定了开放银行框架与标准,这让英国成为首个落地实施开放银行的国家。但在美国,开放银行业由行业主导。这是由于美国金融市场的参与者众多,在竞争激烈的环境下,一些有实力的银行主动开发数据接口,转型成为平台型金融服务公司。

国内开放银行发展呈现由银行主导的自下而上发展的态势。大型商业银行在构建开放银行时一般从两方面入手。一是自建场景,将外部财务软件、一站式公司注册软件、法律援助软件、税务管理软件、医疗软件等服务型软件,通过技术手段引入银行服务体系,为客户提供财务、金融、法律、税务、医疗等全方位、多场景融合的一体化服务。二是融入场景,在金融监管制度框架下,在通过业务规划和技术控制建立安全可靠的风控机制的基础上,逐步扩大支付结算、理财投资、信用卡等领域的金融服务及数据向社交、购物、金融科技、财务等第三方公司的输出,利用第三方公司的业务场景,促进银行金融服务触达更多客户。

二、开放银行赋能普惠金融的路径

目前,开放银行助推普惠金融发展主要表现为以下三种模式。

平台模式——实现从拥抱母体到拥抱生态。从本质上讲,开放银行实现了从拥抱母体到拥抱生态,通过与更多外部场景连接,共享客户基本信息、交易信息等多维度资源,能有效弥补商业银行对普惠金融客户信息搜集、识别及运用的“短板”。换言之,开放银行构建了金融、科技与实体的共建生态圈,不论企业规模大小、是否与核心企业建立供应关系,均可以通过彼此互补实现价值共赢,平等获得优质金融服务。随着开放银行合作渠道不断延伸,通过开放API等形式,接入政务平台、产业互联网、供应链金融、平台经济等各类场景生态,逐步搭建开放的智能金融生态圈,金融服务嵌入场景不断拓展,助力金融服务供给更加结构化、多元化和普惠化,实现金融产品服务精准触达更多普惠客群。

数据开放——促进金融与实体经济融合发展。开放银行结合数字金融发展趋势,充分运用API和SDK技术,以科技能力连接产业平台、企业业务系统与银行系统,实现银行与第三方数据的共享,形成多方数据集成平台。通过数据的开放和共享,有效地将服务触角延伸到中小微企业的上下游,确保其稳健经营;同时将各种不同的商业生态嫁接至平台,间接为中小微企业提供各类金融服务。此外,开放银行通过全程数字化管理的方式,不仅可以提高中小微企业数字化程度,有效降低中小微企业成本,提高资金使用效率,以科技手段为小微客户开辟业务新渠道,构建经营新场景,开拓商业新空间,还可以不断推动合作向全链条、全场景、多层次深化,更高质量地服务中小微企业,助力实体经济发展。

业务开放——有效降低银行产品开发成本。在开放银行模式下,银行通过API技术将自己的产品业务“解耦”为功能模块,客户在各种服务场景中,根据自己的需求通过API自主调用银行功能模块,满足其个性化、场景化的金融需求,掌握金融服务的主动权,也提高了金融服务的自助性。此外,由于开放银行以平台模式批量拓展和服务客户为主,提供集约化服务,促使单一普惠金融客户的服务成本大为下降,规模效益尽显,保持普惠金融事业的可持续发展。通过产品业务模块化处理,开放银行能深度渗透应用场景和贴近用户需求,不断拓展服务范围,将金融化于无形。对客户而言,银行将不再是一个场所,而是一种无所不在、触手可得的服务。数字化转型网szhzxw.cn

三、中国民生银行开放银行服务探索实践

开放银行凭借自身特有的优势深受千行百业认可,市场需求旺盛,行业应用场景丰富。中国民生银行高度重视开放银行发展,结合国家普惠金融战略和自身数字金融战略,积极探索创新开放银行服务模式,打造形成开放银行“生态云”服务平台。通过“走出去”“引进来”和“合作共建”三种形式与第三方机构开展合作,推出“云代账”“云人力”“云货运”“云易付”“云费控”“云健身”“云钱包”等“民生云”系列产品,加快账户、结算、财富、贷款等金融产品的输出,与外部生态合作伙伴共同打造“金融+非金融”一站式综合服务。下文将以中国民生银行开放银行服务中的三类典型案例,介绍开放银行赋能数字普惠金融的行业应用场景及成效。

1、开放银行助推代理记账行业提质增效数字化转型网szhzxw.cn

在传统代理记账模式中,记账以银行对账单、回单作为重要凭证。小微企业只能通过柜台打印或网银下载等方式获取,财务管理平台仅支持人工录入、扫描上传、OCR识别等方式输入,操作流程繁琐、效率较低、容易出错。2020年财政部与国家档案局发布的《关于规范电子会计凭证报销入账归档的通知》(财会〔2020〕6号),明确来源合法、真实的银行电子回单、电子发票等电子凭证与纸质凭证具有同等法律效力,可以作为会计凭证,从政策上支持了会计凭证和会计业务的全面数字化转型。

商业银行以此为契机,通过输出API,将银行系统与财务管理平台直连,经小微企业授权,将其银行回单、明细等数据基于安全传输机制输出至第三方财务平台,财务平台帮助企业自动记账、自动生成凭证,提升了会计工作的效率和准确性。为确保安全合规,商业银行应采用轻量级企业多级授权模式,先由代账公司授权财务平台以代账公司名义代被代账企业发起数据请求,再由被代账企业授权代账公司和财务平台获取其数据和银行会计资料。此授权流程确认了各方的权责关系,认证了代账公司的资质,解决了传统代账业务中被代账企业与代账公司之间需要邮寄会计资料或托管Ukey的问题(见图1)。

从应用效果上看,商业银行在小微客户生命周期中的起点切入,利用账户开户、回单明细轻量级服务撬动记账平台合作,分别解决平台、代账公司、小微客户各自的痛点,强化彼此的关联。各方均受益于最高的价值体验,形成自动筛选有效客户、自动增强聚集效应、自动驱动指数增长的商业模式。对财务平台而言,强化了平台服务能力,通过直连银行系统获取企业会计数据更加快速精准,使自动记账、自动生成凭证成为可能;对代理记账公司而言,省去了人工帮企业收集整理银行会计资料的过程,提升了记账效率,降低了人力成本;对选择自主记账的企业,简化了财务处理流程,提高了效率;对选择代理记账的企业而言,只需一次线上授权,代账公司即可合理合规地获取企业在银行的会计资料,避免了以前邮寄会计资料或托管UKey存在的风险。数字化转型网szhzxw.cn

截至2022年12月31日,中国民生银行已对接用友、金蝶、税友、浪潮、航天信息等头部财务软件服务商,帮助超600家代账公司实现降本增效,通过应用数字化工具和综合解决方案,代账公司会计从人均代账50户提升至200户;服务企业客户超8000户,赋能小微企业财务管理更加轻松便捷。

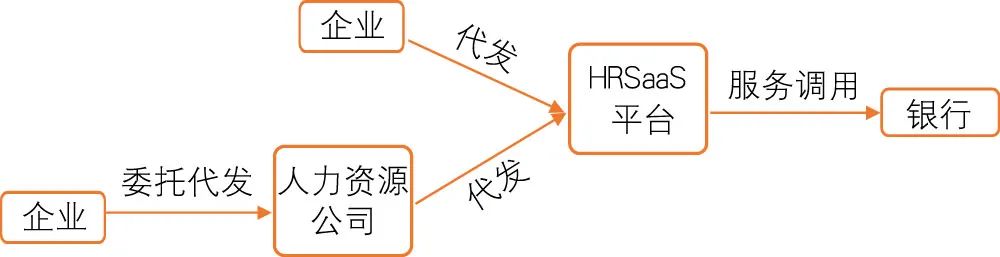

2、开放银行赋能人力资源服务行业提升综合服务能力

在传统模式下,一体化人力资源管理系统(HRSaaS平台)主要提供招聘管理、人事管理、社保管理、薪酬管理、福利管理、绩效管理、培训管理、人才评测等,无法做到与银行联动。其中,薪酬管理仅根据员工的考勤、绩效等数据计算员工的薪资,发放工资时,还需企业财务人员在银行端手动录入薪资,同样面临操作流程繁琐、效率较低、容易出错等问题。

商业银行通过输出API,将银行系统与HRSaaS平台直连,经企业授权,将其银行代发、回单、明细等数据基于安全传输机制输出至第三方人力平台,企业在人力平台操作员工薪资代发时,无需再次手工录入,代发数据可一键传送至银行,代发体验流畅,降低了人工操作成本,提升了薪资代发效率和准确性(见图2)。

从应用效果上看,商业银行以企业员工的薪资代发为切入点,与HRSaaS平台围绕代发工资、回单明细等服务开展合作,一举解决平台和企业客户的痛点,让银行、企业、人力资源管理平台实现共赢。对银行来说,扩宽了服务客户的渠道,通过把银行的金融服务能力输出至人力资源管理平台,提升平台上企业客户享受银行金融服务的便利性和可得性,助推普惠金融发展;对发薪企业来说,省去了人工录入代发数据的过程,提升了代发效率,降低了人力成本;对HRSaaS平台来说,引入银行金融服务能力,可以使企业在平台侧操作发薪,并获取发薪结果等数据,提升综合服务水平,有助于增强客户黏性。同时,平台方可以此服务为抓手,携手银行扩展更多合作场景,共同构建数字化生态服务。

截至2022年12月31日,中国民生银行“云人力”综合服务方案共服务超400级企业,与上海外服、薪人薪事、薪太软、合付保、云薪通等人力服务商建立战略合作关系,助力中小微企业人事管理数字化转型。数字化转型网szhzxw.cn

3、开放银行助力网络货运行业合规稳健发展

随着供给侧结构性改革的持续推进,以数字化为基础的网络货运行业迎来了新的战略机遇。基于网络货运企业在银行开立的对公结算账户,对各货主和实际承运人等交易进行分账记载,可极大提高网络货运平台的线上资金管理效率,节约大量财务成本;同时也将线下承运业务场景转移到线上,助推无车承运人的信息流、订单流、资金流和物流四流合一,实现合规经营。

商业银行依托开放银行API接口聚合能力打造“云货运”生态综合服务方案,以结算为基础,综合各类实时、动态、真实、立体的数据与银行联合建模,开发平台上游核心货主的供应链融资业务,以及下游面向优质司机的消费信贷、支付消费及理财、保险等服务,充分体现商业银行赋能中小微企业数字化经营的理念(见图3)。

从应用效果看,开放银行“云货运”综合服务方案有效解决了网络货运平台所面临的各项痛点。首先是向企业输出底层产品的账户体系,支持平台会员注册实名认证以及子账簿开立登记,叠加线上结算功能,助力上游运输款收缴,并实现平台订单信息与资金流水同步,再根据平台指令清分资金,为下游司机等实际承运人提供现金提取通道。与此同时,针对不同行业、经营体量的货主,尤其聚焦于制造业、大消费场景,可提供适配的定制化融资产品,满足网络货运参与主体的资金需求,打造全面的网络货运场景金融服务体系。

截至2022年12月31目,中国民生银行“云货运”综合服务方案已服务近70万货主及司机,并与青岛数智、山东云顺、无锡远迈等知名货运平台建立战略合作关系,对助推网络货运行业合规稳健发展发挥了积极作用。

四、开放银行未来发展展望数字化转型网szhzxw.cn

强化行业及市场研究,推动金融与场景深度融合。作为开放银行的核心建设者,商业银行需要深入研究国家及重点区域战略,围绕企业“业财税”等业务场景打造新的行业解决方案,与个人、企业、政府建立数字链接、共建开放生态,实现B端、C端客户的裂变式增长,让金融服务更为多元、更加贴心。具体包括:持续跟踪产业结构变迁规律,给予代理记账、人力外包、自动缴税、交通运输、产业园区等生产性服务业以及产业数字化程度较高的行业高度关注,获取具有较大市场份额的客户名单,以电子账户、协议支付、记账代账、收付易等成熟金融产品为基础,辅以供应链融资、保险、融资租赁等产品,为企业/商户解决支付结算、账户管理等领域的痛点问题,为个人客户提供支付缴费、财富管理等服务。

畅通多元服务渠道,搭建立体式服务体系。数字经济时代,商业银行多通道服务不再是纯粹的财务管理工具,而是和客户互动协作的连通器。基于多通道服务的融合,商业银行提供企业用户体系互联互通,把企业客户在各个服务渠道、各环节产生的数据按照不同的管理需求和经营维度,进行直观的展示和对比,帮助企业客户快速做出经营决策。在此理念的影响下,建议商业银行以客户为中心,打通API、H5、网上银行、手机银行、小程序等服务渠道,搭建数字化多维立体服务矩阵,实现渠道间高效协同,给企业经营带来便利。

转变客户服务理念,强化综合服务能力建设。当前,商业银行已清楚地认识到,以开放银行形式输出服务能力并非仅是技术层面的事情,而是全行综合实力的体现。下一阶段,商业银行将在架构、流程、文化等方面进行有针对性地调整,强化行内不同条线板块、不同部门之间的业务协作,全面提升获客、运营、风控、科技等能力,以增强开放性产品的适配性,提高开放服务输出效率。

建立合作对接统一服务协同机制,提升合作对接效率。通过建立开放银行联调沙箱,提供接入指引、接口相关文档、智能小助手、沙箱测试用例、在线模拟联调、测试工具、运营监控驾驶舱等各种功能组件,敏捷响应合作平台系统对接需求,释放科技资源,提升合作对接及敏捷交付效率,打造合作对接统一服务协同平台,完善数字化交付管理体系。

构建多维度、多层次的安全风险防控体系。加强事前防御,做到防患未然。对合作伙伴进行市场规模、科技实力、系统安全、客户服务等多维度审慎评估;强化事中实时监测、快速处置,运用差异化的防控模型对客户身份和目标进行识别;完善事后监控分析、预警优化,建立并逐步完善开放银行业务监控模型,基于大数据分析技术,对开放银行交易数据进行监控,及时发现并处置风险点。

数字经济的本质是一场生产力革命。开放银行作为“数据和能力”跨机构、跨领域开放的重要体现,将打破银行与客户之间的封闭关系,深刻改变现有银行对客服务方式。展望未来,商业银行将以开放共赢的全新商业模式,与生态伙伴携手创新、共建场景,形成金融与相关行业紧密融合的“数字共同体”,真正做到以客户为中心,推动普惠金融高质量发展,促进实体经济保持长效增长。

翻译:

At present, digital economy has become an important force for promoting high-quality economic and social development and improving quality and efficiency. The report of the 20th National Congress of the Communist Party of China proposed to accelerate the development of the digital economy and promote the deep integration of the digital economy and the real economy. The era of digital economy requires a large number of small and medium-sized enterprises, and the innovation breakthrough of small and medium-sized enterprises is often accompanied by the digital transformation of the financial industry.

In recent years, with the rapid integration of digital technology and the financial industry, commercial banks have made arrangements in succession. While actively using digital technology to enhance the efficiency of banking services and improve customer service experience, they also integrate financial services into specific enterprise scenarios by means of open empowerment, which can not only improve the financial availability of various groups as a whole and promote the high-quality development of finance. It also helps to promote small and medium-sized enterprises to “go to the cloud, use data and give wisdom”. Among them, promoting the construction of open banks is a very important link.

A brief analysis of the development status of open bank数字化转型网szhzxw.cn

Open banking, as defined by Gartner, is a platform-based business model that provides services to customers, employees, third-party developers, fintech companies, vendors and other partners of the business ecosystem by sharing data, algorithms, transactions, processes and other business functions with the business ecosystem. Enable banks to create new value and build new core capabilities.

After the concept of open banking was first proposed by a bank in the UK in 2014, financial institutions in the UK, Australia, Singapore and other countries carried out trials one after another, and soon a wave of open banking development was set off worldwide. From the perspective of development process, foreign countries show the characteristics of being driven by regulatory authorities and top-down. The typical ones are the UK and the EU. In March 2016, the British Ministry of Finance issued the Open Banking Standard, which formally determined the open banking framework and standards, making the UK the first country to implement open banking. But in the US, open banking is industry-led. This is due to the large number of participants in the US financial market. In the fierce competition environment, some strong banks take the initiative to develop data interfaces and transform into platform-type financial service companies.数字化转型网szhzxw.cn

The development of open banks in China shows a trend of bottom-up development dominated by banks.

Large commercial banks generally start from two aspects when building open banks. First, the self-built scenario introduces the external financial software, one-stop company registration software, legal aid software, tax management software, medical software and other service software into the banking service system through technical means to provide customers with comprehensive and multi-scene integrated services such as finance, finance, law, tax and medical. Second, integrate into the scene. Under the framework of the financial regulatory system, on the basis of establishing a safe and reliable risk control mechanism through business planning and technology control, gradually expand the output of financial services and data in fields such as payment and settlement, financial investment and credit card to third-party companies such as social networking, shopping, fintech and finance, and make use of the business scenarios of third-party companies. Facilitating banks’ financial services to reach more customers.

Open up ways for banks to enable inclusive finance

At present, there are three main modes that open banks can promote the development of inclusive finance.

Platform model — from embracing the mother to embracing the ecology.

In essence, open bank has realized the transformation from embracing the mother to embracing the ecology. By connecting with more external scenes and sharing multi-dimensional resources such as basic customer information and transaction information, it can effectively make up for the “weaknesses” of commercial banks in the collection, identification and application of inclusive finance customer information. In other words, open banks build a co-built ecosystem of finance, technology and entities. Regardless of the size of enterprises or whether they establish supply relations with core enterprises, they can achieve win-win value through complementing each other and equal access to high-quality financial services.

With the continuous extension of open banking cooperation channels, through the open API and other forms of access to government platforms, industrial Internet, supply chain finance, platform economy and other scenarios, gradually build an open intelligent financial ecosystem, financial service embeddedness is constantly expanded, and the supply of financial services is more structured, diversified and inclusive. To achieve financial products and services accurately reach more inclusive customer groups.

Data opening — promoting the integrated development of finance and the real economy.

Combined with the development trend of digital finance, open bank makes full use of API and SDK technology to connect industrial platform, enterprise business system and banking system with scientific and technological capabilities, realize data sharing between banks and the third party, and form a multi-party data integration platform. Through the opening and sharing of data, the service tentacles can be effectively extended to the upstream and downstream of micro, small and medium-sized enterprises to ensure their steady operation;

At the same time, various commercial ecology is grafted onto the platform to indirectly provide various financial services for small, medium and micro enterprises. In addition, through the whole-process digital management, open bank can not only improve the digitalization degree of micro. Small and medium-sized enterprises, effectively reduce the cost of micro, small and medium-sized enterprises, improve the efficiency of capital use, open up new business channels for small and micro customers by means of science and technology, construct new business scenarios and expand new business space. But also continuously promote cooperation to the whole chain, the whole scene and the multi-level deepening. We will provide better services to micro, small and medium-sized enterprises and boost the development of the real economy.

Business opening – effectively reduce the cost of bank product development. 数字化转型网szhzxw.cn

In the open banking mode, the bank “decoups” its product business into function modules through API technology. In various service scenarios, customers can call bank function modules independently through API according to their own needs. So as to meet their personalized and scenario-oriented financial needs, master the initiative of financial services. And improve the self-service of financial services. In addition, as open banks mainly expand and serve customers in batch in the platform mode. And provide intensive services, the service cost of single inclusive financial customers is greatly reduced. And the economies of scale are fully demonstrated, thus maintaining the sustainable development of inclusive financial undertakings.

Through the modular processing of product business, open banks can penetrate deeply into the application scenarios and meet the needs of users. Constantly expand the scope of service, and make financialization invisible. For customers, banks will no longer be a place but a ubiquitous, accessible service.

Exploration and Practice of open banking services of China Minsheng Bank

With its own unique advantages, open bank is widely recognized by thousands of banks and industries, with strong market demand and rich industry application scenarios. China Minsheng Bank attaches great importance to the development of open banking. Combining the national inclusive finance strategy and its own digital finance strategy. China Minsheng Bank actively explores and innovates open banking service models, and builds an “ecological cloud” service platform for open banking. 数字化转型网szhzxw.cn

Through the three forms of “going out”, “bringing in” and “co-building”. We cooperate with third-party institutions, launch “cloud account replacement”, “cloud manpower”, “cloud freight”, “cloud easy pay”, “cloud fee control”, “cloud fitness”, “cloud wallet” and other “Minsheng cloud” series products. And accelerate the output of financial products such as account, settlement, wealth and loan. Jointly build “financial + non-financial” one-stop comprehensive services with external ecological partners. The following sections will take three typical cases of open banking services of China Minsheng Bank to introduce the industry application scenarios and effects of enabling digital inclusive finance in open banks.

Open banks to boost the quality and efficiency of the bookkeeping industry

In the traditional bookkeeping model, bank statements and receipts are used as important vouchers.

Small and micro enterprises can only be obtained by printing over the counter or downloading from online bank. The financial management platform only supports manual input, scanning and uploading, OCR identification and other input methods. The operation process is cumbersome, low efficiency and prone to errors. In 2020, the Ministry of Finance and the National Archives Administration issued the Notice on Standardizing the Entry and Archiving of Reimbursement of Electronic Accounting Vouchers (No. 6, 2020), which clarified that electronic bank receipts, electronic invoices and other electronic vouchers with legitimate and authentic sources have the same legal effect as paper vouchers and can be used as accounting vouchers. From the policy support accounting vouchers and accounting business comprehensive digital transformation.

Taking this opportunity, commercial banks directly connect the banking system with the financial management platform through the output API.

Authorized by small and micro enterprises, they export their bank statements. Details and other data to the third-party financial platform based on the secure transmission mechanism. The financial platform helps enterprises to automatically keep accounts and automatically generate vouchers. Thus improving the efficiency and accuracy of accounting work. In order to ensure safety and compliance, commercial banks should adopt the lightweight enterprise multi-level authorization mode.

First, the accounting agent company authorizes the financial platform to initiate data request on behalf of the accounting company in the name of the accounting agent. And then the accounting agent company and the financial platform are authorized by the accounting agent enterprise to obtain their data and bank accounting information. This authorization process confirms the right and responsibility relationship of all parties, certifies the qualification of the accounting agent. And solves the problem of mailing accounting materials or trusteeship ukeys between the accounting agent and the accounting agent in the traditional accounting agent business (see Figure 1).

From the perspective of application effect, commercial banks start from the starting point in the life cycle of small and micro customers.

From the perspective of application effect, commercial banks start from the starting point in the life cycle of small and micro customers, leverage the lightweight service of account opening and receipt details to leverage the cooperation of the accounting platform, solve the pain points of the platform, account agent companies and small and micro customers respectively, and strengthen the correlation between each other.

All parties benefit from the highest value experience, forming a business model that automatically screens valid customers. Automatically enhances aggregation, and automatically drives exponential growth. For the financial platform, it strengthens the service ability of the platform. And obtains enterprise accounting data more quickly and accurately through direct connection to the bank system. Which makes automatic bookkeeping and automatic voucher generation possible. For the agency bookkeeping company, it eliminates the process of manual help enterprises collect and sort out bank accounting information, improves the efficiency of bookkeeping, reduces the labor cost. To choose independent accounting enterprises, simplified financial processing process, improve efficiency. For the choice of bookkeeping enterprises, only one online authorization. The accounting company can reasonably obtain the accounting information in the bank. To avoid the previous mailing accounting information or custody of UKey risk.数字化转型网szhzxw.cn

By December 31, 2022, China Minsheng Bank has cooperated with the head financial software service providers. Such as Yonyou, Kingdee, Taxyou, Inspur and Aerospace Information to help more than 600 accounting agent companies achieve cost reduction and efficiency increase. Through the application of digital tools and comprehensive solutions. The accounting accounts of accounting agent companies have increased from 50 to 200 households per capita. It serves more than 8,000 enterprise customers, enabling small and micro enterprises to manage their finances more easily and conveniently.

Open the bank to empower the human resource service industry to enhance the comprehensive service ability

In the traditional mode, the integrated human resource management system (HRSaaS platform) mainly provides recruitment management, personnel management, social security management, compensation management, benefit management, performance management, training management, talent evaluation, etc., which cannot be linked with banks. Among them, the salary management only calculates the employee’s salary according to the employee’s attendance, performance and other data. When the salary is paid, the financial personnel of the enterprise needs to manually input the salary at the bank side. Which also faces the cumbersome operation process, low efficiency, easy to make mistakes and other problems.

Through the output API, commercial banks directly connect the banking system with HRSaaS platform. Authorized by the enterprise, they can export the data such as bank issuance. Receipt and details to the third-party human resource platform based on the secure transmission mechanism. When the enterprise operates the employee salary issuance on the human resource platform. There is no need to manually input the data again. The manual operation cost is reduced, and the efficiency and accuracy of payroll agency are improved (see Figure 2).

From the perspective of application effect, Commercial Bank takes the salary payment agency of enterprise employees as the starting point.

From the perspective of application effect, Commercial Bank takes the salary payment agency of enterprise employees as the starting point. And develops cooperation with HRSaaS platform on such services as salary payment agency and receipt details. So as to solve the pain points of the platform and enterprise customers in one move. So that the bank, enterprise and human resource management platform can achieve a win-win situation.

For banks, it expands the channels to serve customers. By exporting banks’ financial service capabilities to the human resource management platform. It improves the convenience and availability of corporate customers on the platform to enjoy bank financial services and promotes the development of inclusive finance. For payroll enterprises, it saves the process of manual data input and dispatch, improves the efficiency of dispatch and reduces the labor cost. For HRSaaS platform, the introduction of bank financial service capability enables enterprises to operate payroll on the platform and obtain payroll results and other data, improve the comprehensive service level and help enhance customer stickiness. At the same time, the platform can take this service as the starting point, cooperate with banks to expand more cooperation scenarios, and jointly build digital ecological services.

As of December 31, 2022, China Minsheng Bank’s “Cloud Manpower” comprehensive service program has served more than 400 level enterprises. And established strategic cooperative relations with Shanghai foreign Service, Payman, Paysoft, co-pay insurance, Cloud PayTong and other HR service providers to help micro. Small and medium-sized enterprises with the digital transformation of personnel management.

Open banks to help the compliance and steady development of the network freight industry

With the continuous advancement of the supply-side structural reform, the digital-based network freight industry has ushered in new strategic opportunities. Based on the public settlement account opened by the network freight enterprises in the bank. The transactions of each shipper and the actual carrier are recorded in separate accounts. Which can greatly improve the efficiency of online fund management of the network freight platform and save a lot of financial costs. At the same time, the offline carrier business scenario is transferred to the online one. Which promotes the integration of information flow, order flow, capital flow and logistics of car-free carriers to realize compliance operation.

Relying on the aggregation ability of open bank API interface, commercial banks create an ecological integrated service plan of “cloud freight”. Based on settlement, commercial banks integrate all kinds of real-time, dynamic. Real and three-dimensional data with the joint modeling of banks to develop the supply chain financing business of the upstream core cargo owners of the platform. As well as the downstream consumer credit, payment and consumption, financial management and insurance services for quality drivers. It fully reflects the concept of empowering micro, small and medium-sized enterprises to operate digitally by commercial banks (see Figure 3).

From the application effect, the open bank “cloud freight” integrated service scheme has effectively solved the various pain points faced by the network freight platform.

The first is to export the underlying product account system to enterprises, support platform member registration real-name authentication and sub-ledger opening and registration, stack online settlement function, help the upstream transportation payment collection. And realize the platform order information and capital flow synchronization. And then according to the platform instructions to clear funds. For the downstream drivers and other actual carriers to provide cash withdrawal channels. At the same time, for shippers in different industries and business volumes. Especially in manufacturing and large consumption scenarios, customized financing products can be provided to meet the capital needs of participants in online freight transport. And a comprehensive financial service system for online freight transport scenarios can be built.

As of December 31, 2022, China Minsheng Bank’s “Cloud Freight” comprehensive service program has served nearly 700,000 freight owners and drivers. And established strategic cooperative relations with Qingdao Suzhi, Shandong Yunshun, Wuxi Yuanmai and other well-known freight platforms. Which has played a positive role in promoting the compliance and steady development of the online freight industry.数字化转型网szhzxw.cn

Prospects for the future development of open Banks

Strengthen industry and market research, and promote the deep integration of finance and scene.

As the core builder of open banks, commercial banks need to deeply study national and key regional strategies. Create new industry solutions around business scenarios such as “industry finance and taxation”. Establish digital links with individuals, enterprises and governments, and build open ecology together. So as to realize the cracking growth of B-end and C-end customers, and make financial services more diversified and intimate.

The details include: Continue to track the change law of industrial structure, pay close attention to producer services. Such as bookkeeping, human outsourcing, automatic tax payment, transportation, industrial parks and industries with a high degree of industrial digitalization. Obtain the customer list with a large market share, based on mature financial products such as electronic account, agreement payment, bookkeeping and payment facilitation. Supplemented by supply chain financing, insurance, financial leasing and other products. It solves the pain points in payment and settlement, account management and other fields for enterprises/merchants. And provides payment and payment, wealth management and other services for individual customers.

Smooth multiple service channels and build a three-dimensional service system. 数字化转型网szhzxw.cn

In the age of digital economy, the multi-channel service of commercial banks is no longer a pure financial management tool, but a communication device for interaction and cooperation with customers. Based on the integration of multi-channel services, commercial banks provide interconnection of enterprise user systems. Intuitively display and compare the data generated by enterprise customers in various service channels and links according to different management needs and management dimensions. And help enterprise customers to make business decisions quickly. Under the influence of this concept, it is suggested that commercial banks take the customer as the center. Open up service channels such as API, H5, online banking, mobile banking and mini programs. Build a digital multi-dimensional service matrix, realize efficient collaboration between channels. And bring convenience to enterprise operation.

Change the concept of customer service, strengthen comprehensive service capacity building.

At present, commercial banks have clearly realized that the ability to export services in the form of open banking is not only a technical matter. But a reflection of the comprehensive strength of the whole bank. In the next stage, commercial banks will make targeted adjustments in terms of structure, process and culture, strengthen business cooperation among different lines and departments within the bank, comprehensively improve customer acquisition, operation, risk control, science and technology capabilities. So as to enhance the suitability of open products and improve the output efficiency of open services.

We will establish a unified service coordination mechanism for cooperation and docking, and improve the efficiency of cooperation and docking.

Through the establishment of open bank sandbox, various functional components. Such as access guidance, interface related documents, intelligent small assistant, sandbox test cases, online simulation of sandbox, test tools. And operation monitoring cockpit are provided to respond to the system docking needs of cooperation platform in a agile manner, release scientific and technological resources, improve the efficiency of cooperation docking and agile delivery, and build a unified service cooperation platform for cooperation docking. Improve the digital delivery management system.

We will build a multi-dimensional and multi-tiered security risk prevention and control system. 数字化转型网szhzxw.cn

Strengthen prevention in advance, so as to prevent trouble. Conduct multi-dimensional prudent evaluation of partners, such as market size, scientific and technological strength, system security and customer service. Strengthen real-time monitoring and quick handling, and use differentiated prevention and control models to identify customer identities and targets. Improve post-monitoring analysis and early-warning optimization, establish and gradually improve the monitoring model of open banking business, monitor the transaction data of open banks based on big data analysis technology, and timely discover and deal with risk points.

The essence of the digital economy is a productivity revolution. As an important embodiment of the cross-institutional and cross-field openness of “data and capability”, open banking will break the closed relationship between banks and customers and profoundly change the existing banks’ service methods to customers. Looking forward to the future, commercial banks will work together with ecological partners to innovate and build scenarios with a new open and win-win business model, form a “digital community” closely integrated with finance and related industries, truly focus on customers, promote the high-quality development of inclusive finance, and promote the long-term growth of the real economy.数字化转型网szhzxw.cn

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:银行家杂志 ,作者:陈琼;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(http://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。