银行丨研究报告

核心摘要:

报告从银行数字化行业的发展背景及现状痛点入手,对中国商业银行数字化转型的关键要素进行梳理分析。通过艾瑞资深团队搭建的一套成熟完善的银行数字化评测体系,从数字化转型能力与数字化底层支撑两方面拆解银行数字化转型的差异化实施路径及技术需求判断,并对银行数智化、开放性、敏捷性、生态化的未来趋势进行深入洞察。同时,本篇报告优选银行数字化服务领域的头部企业,并深度剖析其服务银行的优秀案例,最终评选出50强企业。

一、银行数字化转型背景介绍及难点剖析

1、大势所趋:银行业数字化转型

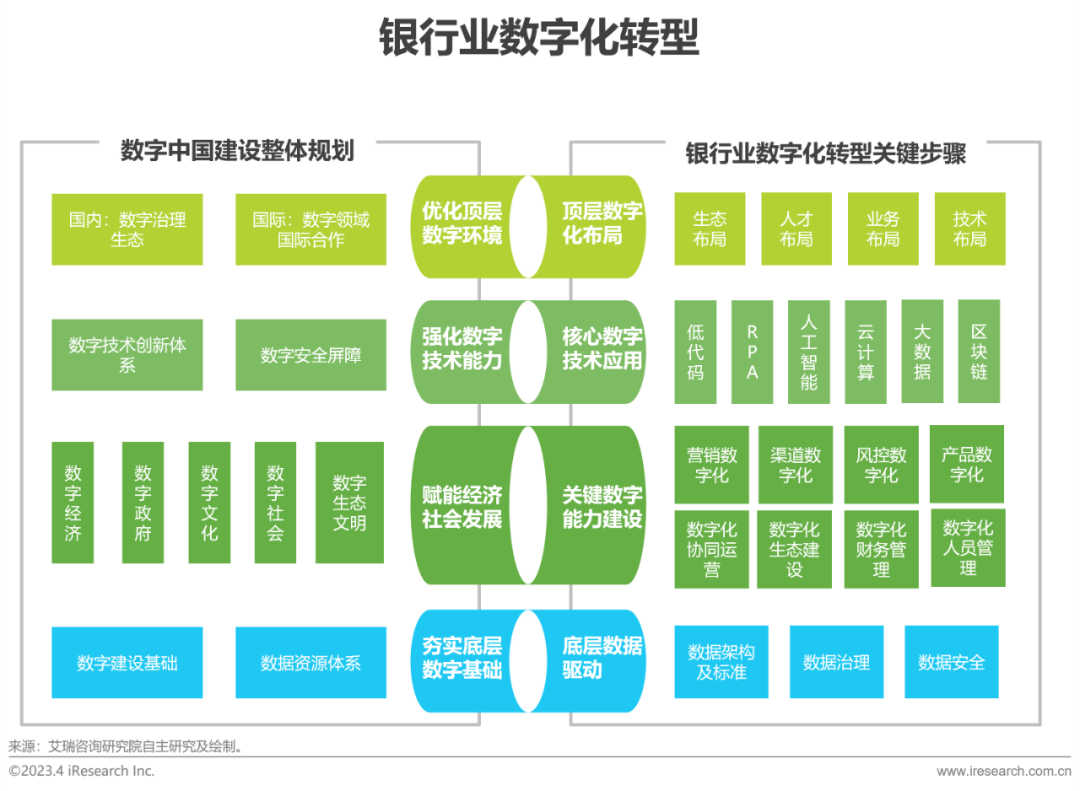

数字中国建设成未来最大确定性之一,银行业应加快数字化转型以适应数字经济社会新环境

2、顶层规划:构建数字金融新格局

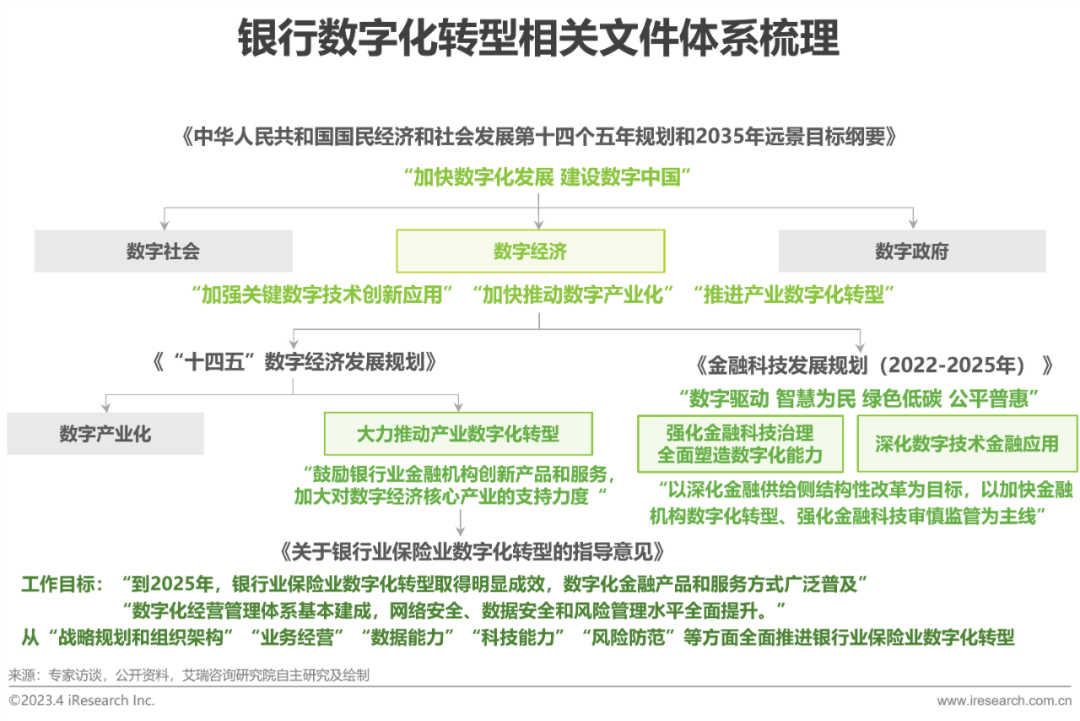

由广入微,见微知著,国家数字化转型系列政策层层推进,逐步构建数字金融新格局

3、疫情影响:“后疫情时代”的挑战

疫情促使“非接触式”金融服务需求激增,银行业务线上化进程加速

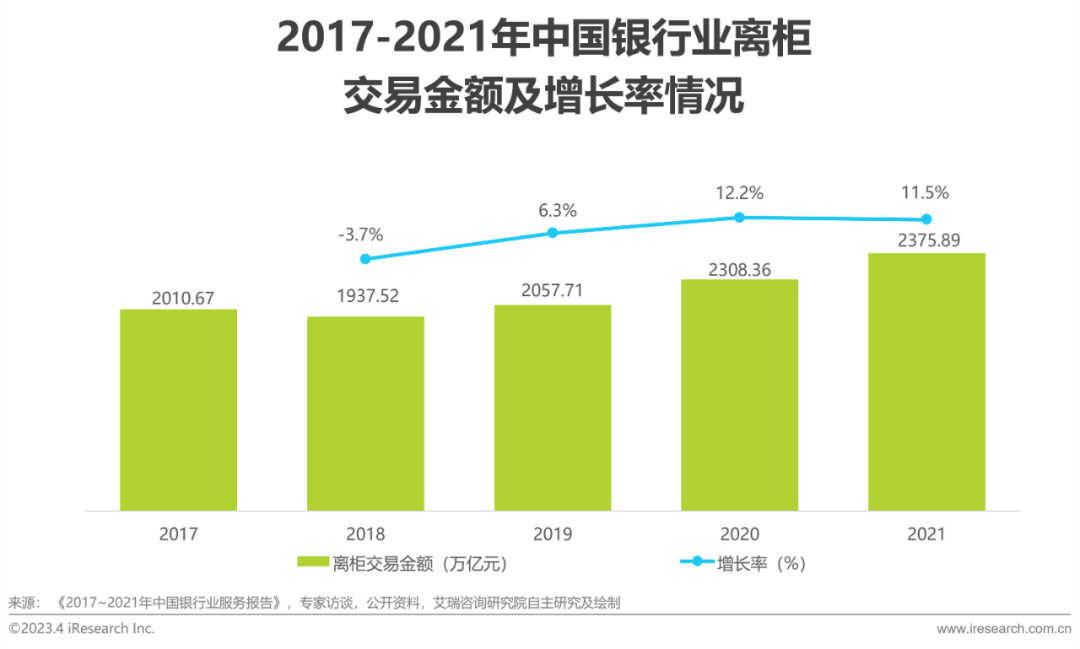

疫情限制线下金融活动,改变用户金融业务办理习惯,线上渠道与“非接触式”金融服务受到市场的普遍关注。2020年2月,中国银保监会发布《关于进一步做好疫情防控金融服务的通知》要求各银行保险机构“积极推广线上业务”,“优化丰富‘非接触式服务’渠道”。在政策影响下,2020年中国银行业离柜交易金额增长率约为2019年的两倍,一年内由6.3%提升至12.2%,到2021年离柜增长率仍维持在较高增长水平,离柜交易金额连续两年稳步提升。疫情对于用户金融业务办理习惯的改变促使银行业务线上化转型进程的推进,“非接触式”金融服务对于银行渠道建设能力、技术架构搭建、数字化运营能力等多方面提出了全新的要求,为银行业数字化发展与金融服务方式改变带来持久而深远的影响。

4、外部竞争:互联网公司入局造成冲击

互联网公司技术能力及生态建设水平超过银行,金融“换”媒浪潮动摇银行市场地位

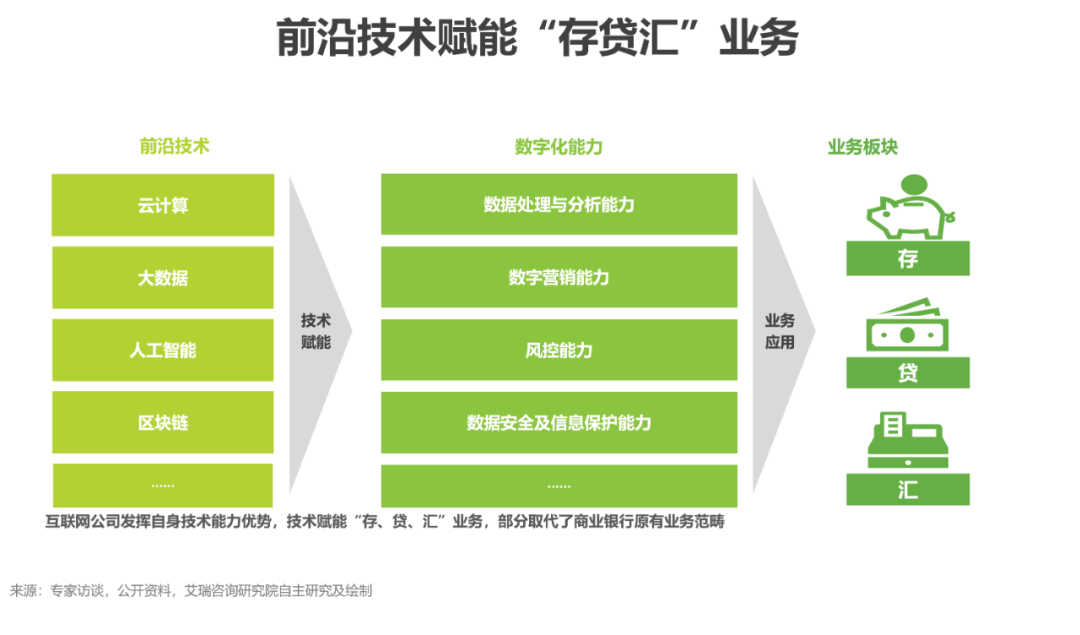

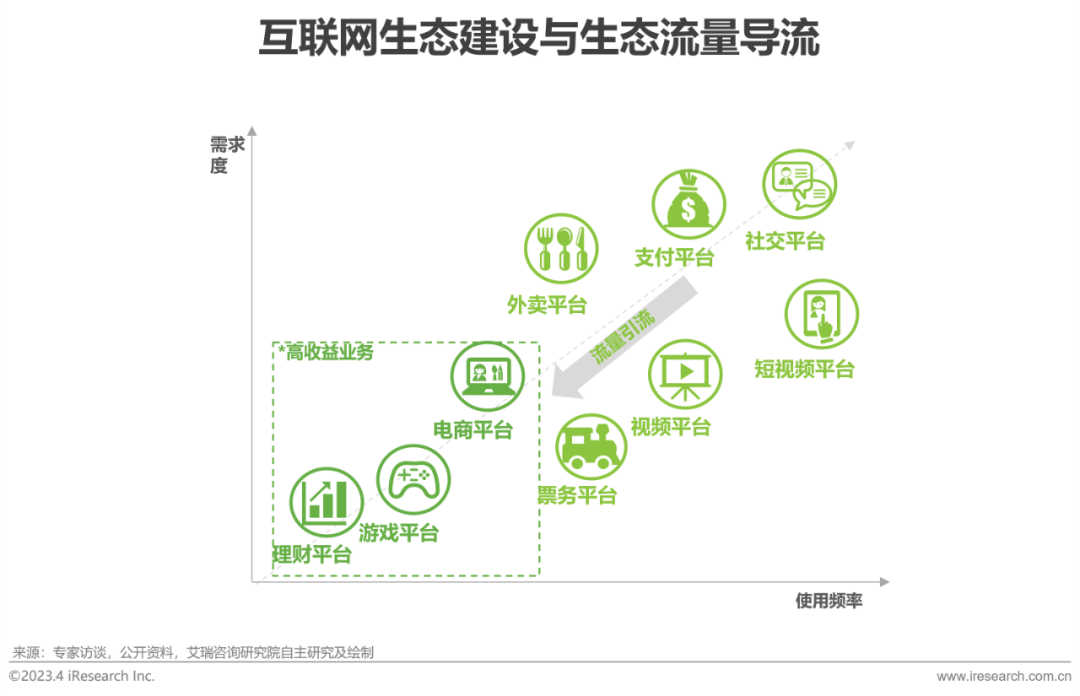

随着大数据、人工智能、云计算等前沿技术在互联网领域的成熟应用,互联网企业充分发挥其自身技术能力优势,将新技术在数据分析、模型搭建、信息保护等方面的数字化能力应用于金融服务领域,为银行传统“存、贷、汇”业务带来服务模式与运营方式的革新。在技术赋能金融业务的同时,互联网企业在金融领域的探索与技术革新对于商业银行原有业务板块与市场份额带来了不小的冲击,金融“换”媒浪潮逐步动摇银行在金融领域的市场地位。除此之外,互联网企业在生态能力建设与生态资源整合方面拥有先天优势,有能力和资源将在高频高需平台获取的用户流量迁移至高收益的电商、金融板块,从流量入口端侵蚀银行银行客户资源,导致商业银行从流量端口开始就存在流量锐减的问题,进一步影响了银行整个生态体系业务的流量和业务收益,将互联网巨头在流量方面优势逐步扩大到更深层的高收益业务领域。

5、内部投入:银行业IT投入逐年稳步增加

近年国内银行业IT投入规模稳步提升,预计将以约24.6%的复合增长率高速增长,2025年市场投入规模将接近6000亿

随着国家数字化转型系列政策的出台及前沿技术在金融服务领域应用的逐步成熟,银行数字化转型已经成为国内商业银行发展的大势所趋。近年国内银行业在IT建设与服务领域的资金投入规模逐年递增,自2019年起银行业IT投入规模以24%的复合增长率稳定高速增长,在2022年突破3000亿元,预计未来国内银行业IT投入规模仍将以约24.6%的复合增长率保持高速增长态势,于2025年达到接近6000亿的规模投入。

6、技术进步:前沿技术与银行业高度契合

底层技术及新兴技术的成熟发展成为银行数字化转型助推器

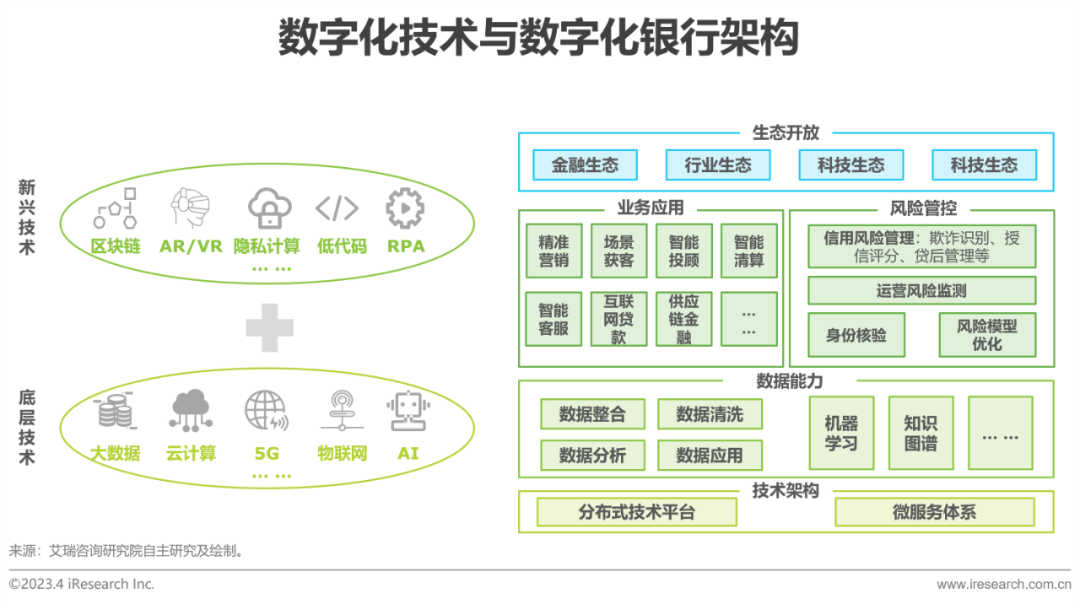

数字化转型离不开坚实的技术支撑。日渐成熟的大数据、云计算及AI等底层技术与数字化场景衍生新兴技术相辅相成,赋能于诸多银行业务场景。如智能客服:基于自然语言理解的对话机器人可取代部分人工客服,降低人力成本,提升解决问题的效率。智能清算:搭建基于区块链的供应链金融平台,完成数据的可信流转,使企业客户实现更便捷安全的自动清算。

信用风险管理:主要通过大数据技术识别信息不对称问题,进行欺诈识别、授信评分、贷后管理等风险管理。在如今数字新基建的背景下,依托“ABCDE”(人工智能(AI)、大数据(BigData)、云(Cloud)、物联网设备(Device)及前沿探索(Exploration))全栈技术能力,打造数字化产品、渠道、运营及生态体系,已成为促进银行业数字化升级的刚需。

二、模型详解及落地指南

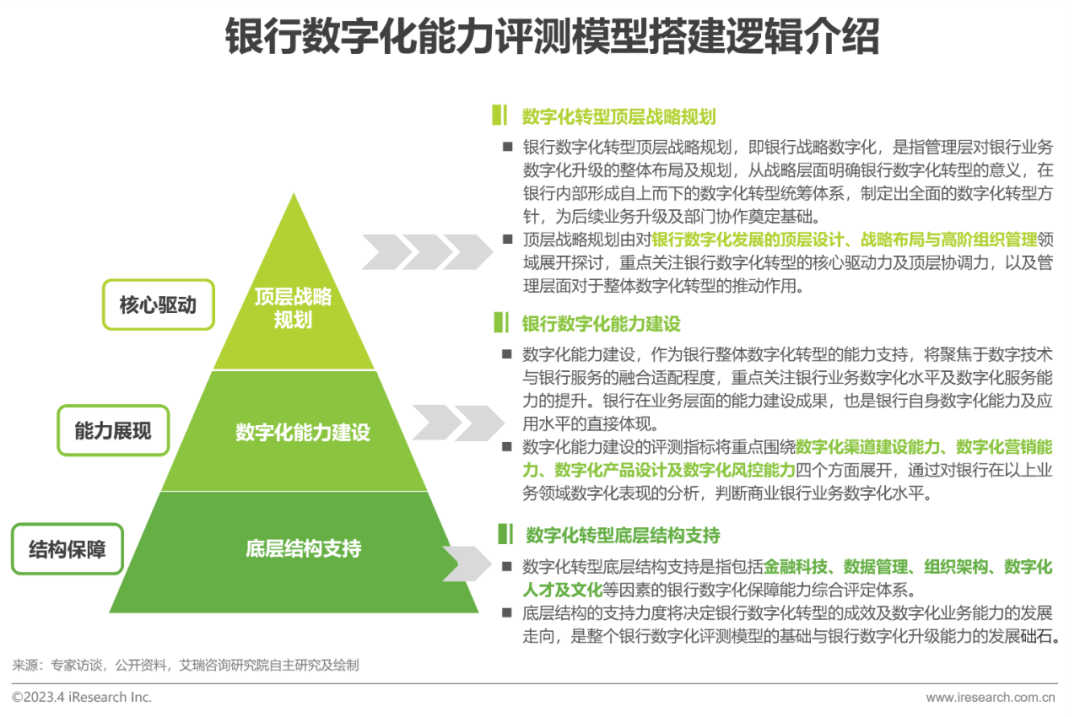

1、模型搭建逻辑介绍

评测模型由作为核心驱动的顶层战略规划、能力展现的数字化能力建设以及作为转型保障的底层结构支持三部分构成

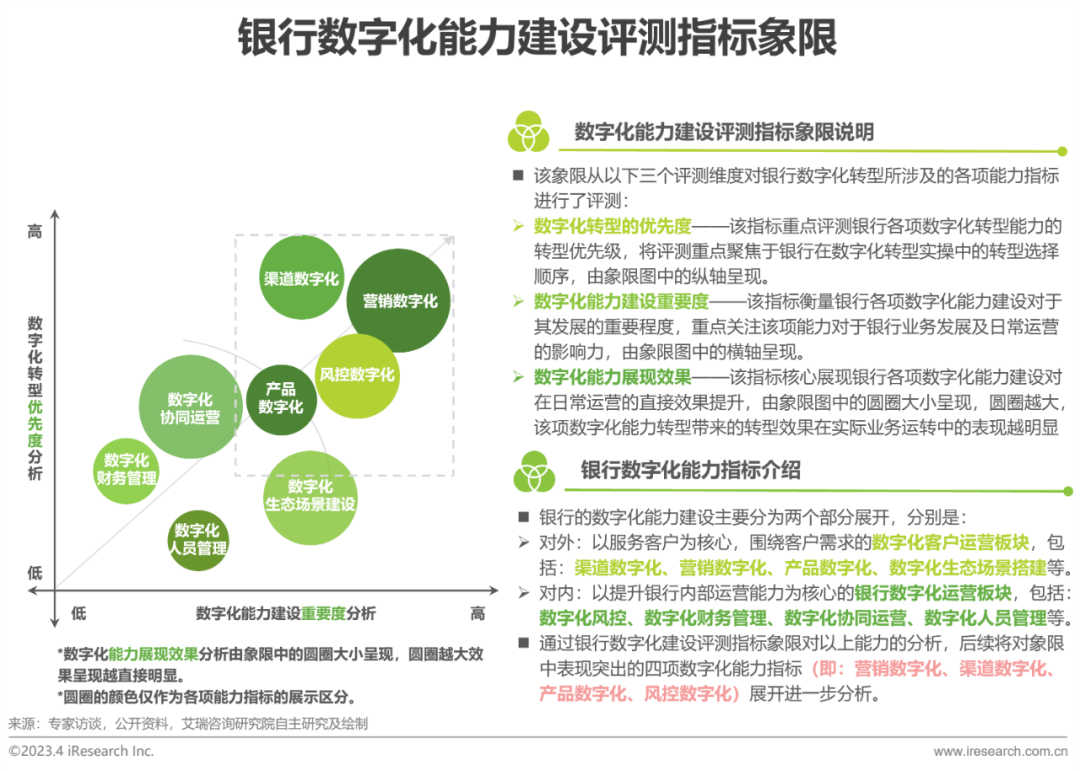

2、数字化能力建设:数字化指标象限展示

通过优先度、重要度与能力展现效果三重维度评测银行数字化能力转型水平

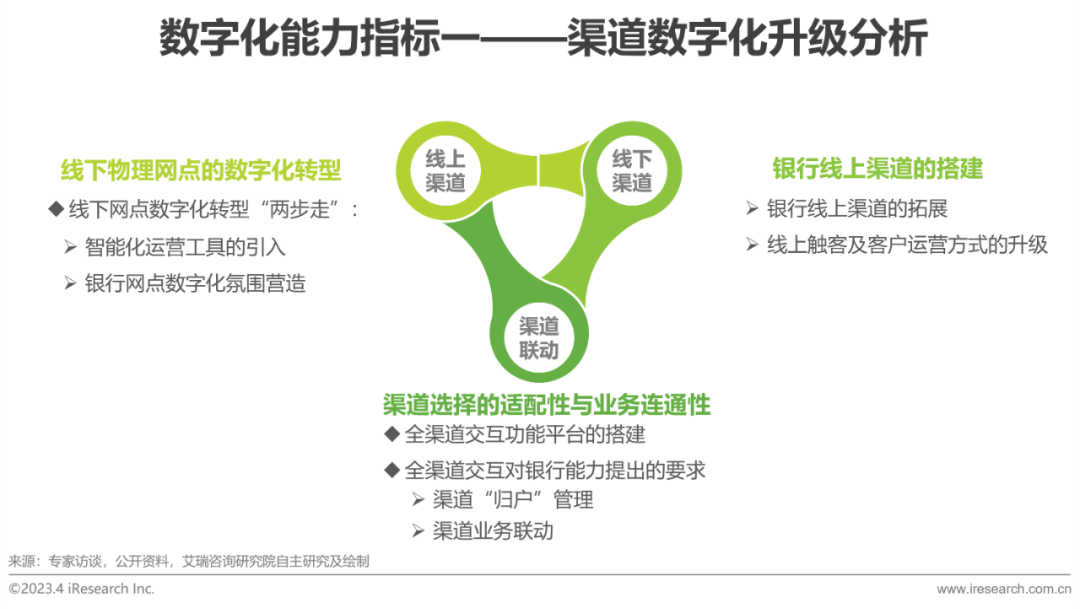

3、数字化能力指标一:渠道数字化

渠道数字化由线上、线下渠道建设及渠道联动三部分组成

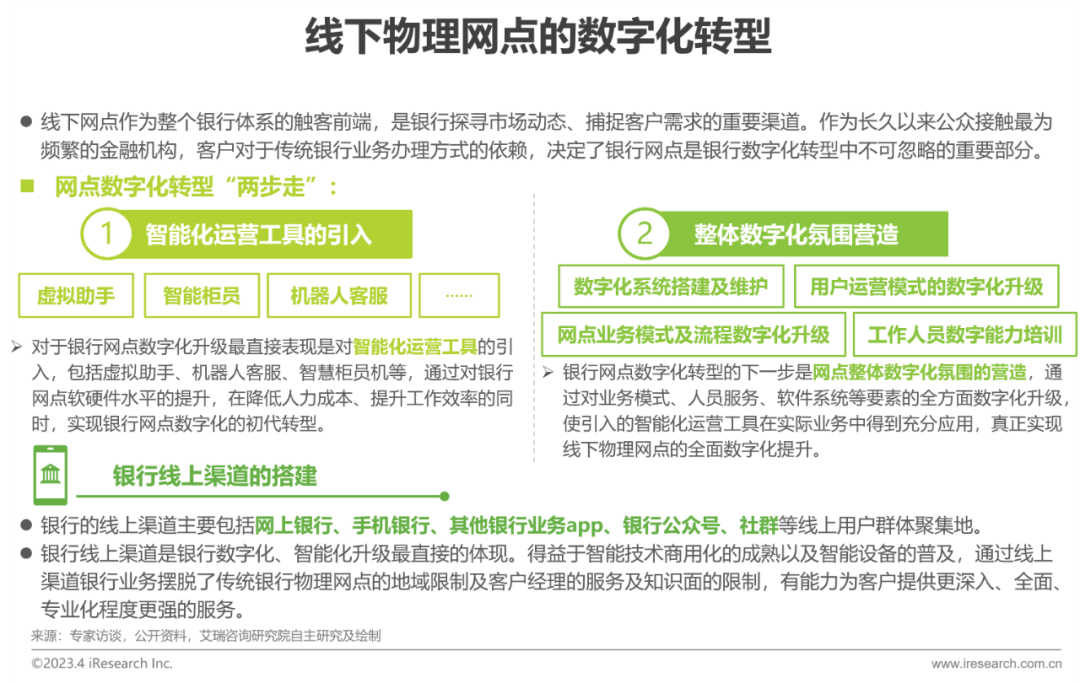

渠道建设作为银行业务的基础环节,其数字化转型的效果将直接影响银行在营销、产品、风控等其他领域的数字化表现。构建数字化渠道、实现渠道间智慧联动不仅是银行数字化转型过程中的优先选项,其对于银行业务的发展及数字化转型效果的呈现都是不可或缺的关键部分。银行的渠道数字化能力主要体现在三个方面,分别是银行线下网点数字化转型、线上数字化渠道建设以及渠道间的联动互通,后续内容将围绕以上三方面开展对于银行渠道数字化建设能力的分析。

智能工具的引入助力银行线下网点的数字化升级;网银、手机银行等线上平台成为银行线上用户的聚集地

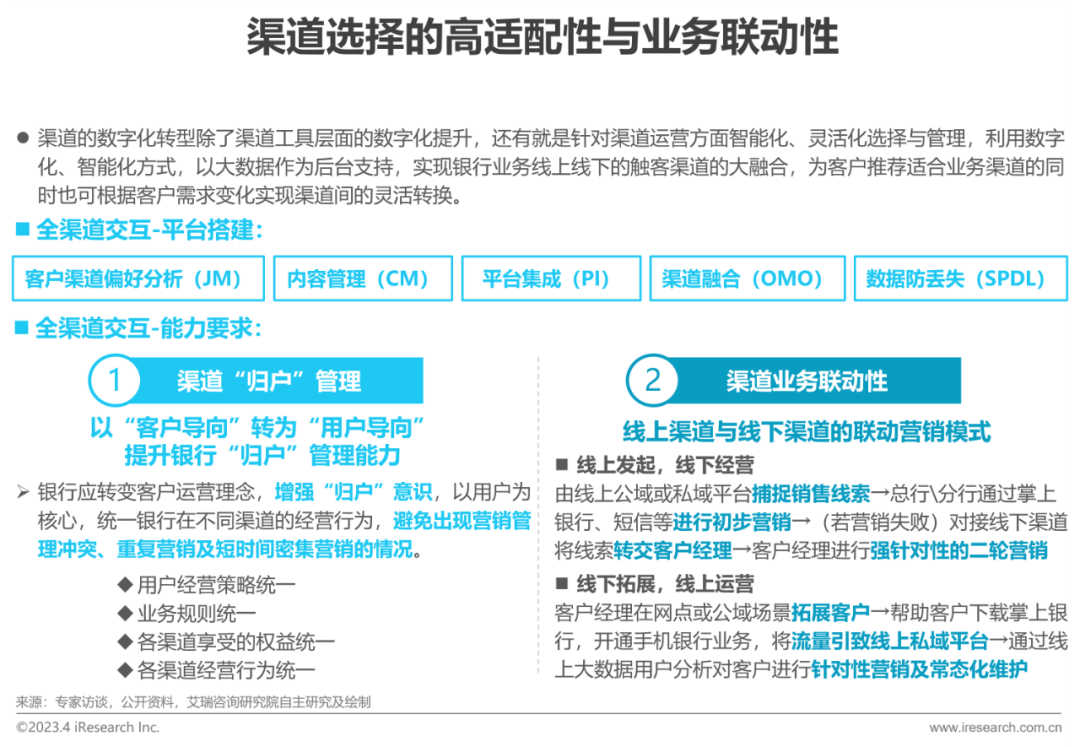

业务联动性依赖于银行归户管理能力及业务联通体系的搭建

4、数字化能力指标二:营销数字化

建立以用户运营为核心的数字化营销体系,围绕用户全生命周期提供精准营销服务

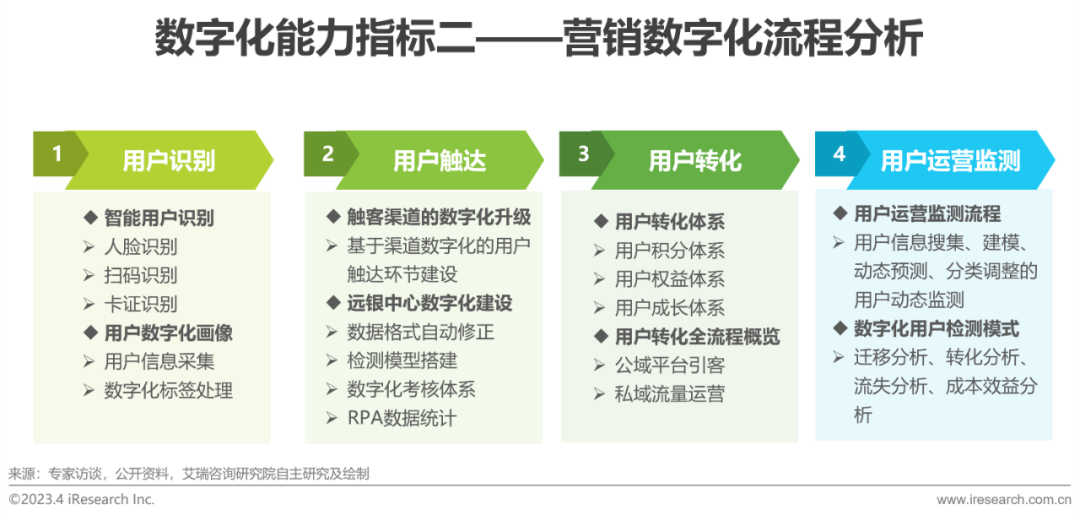

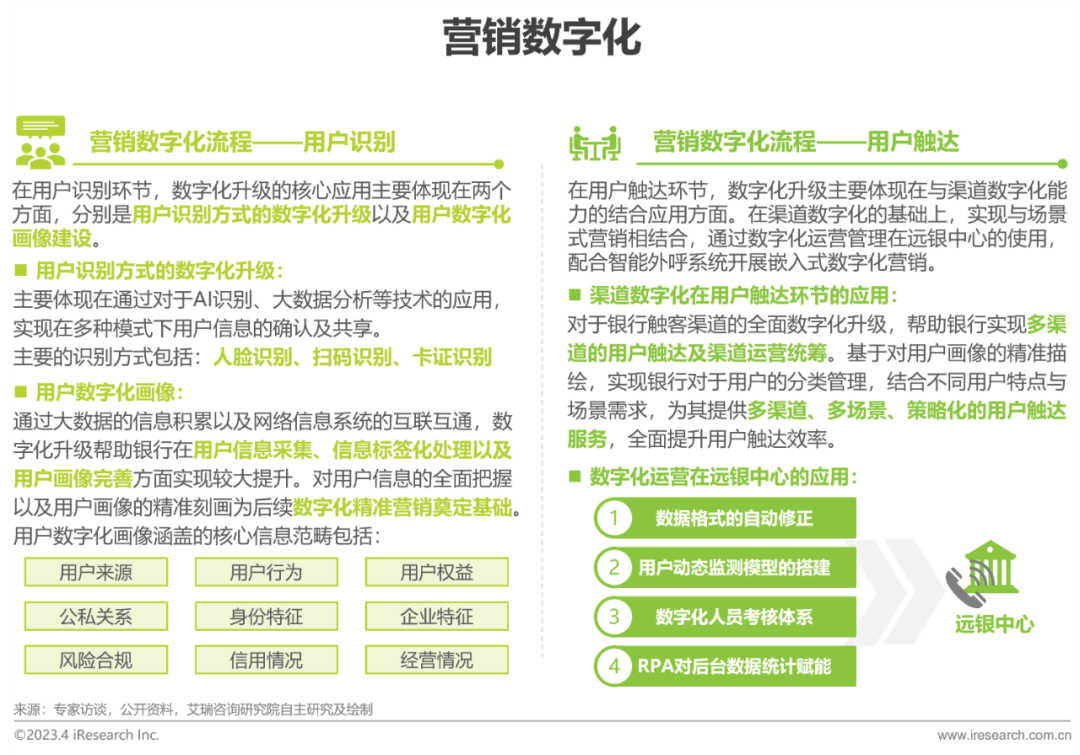

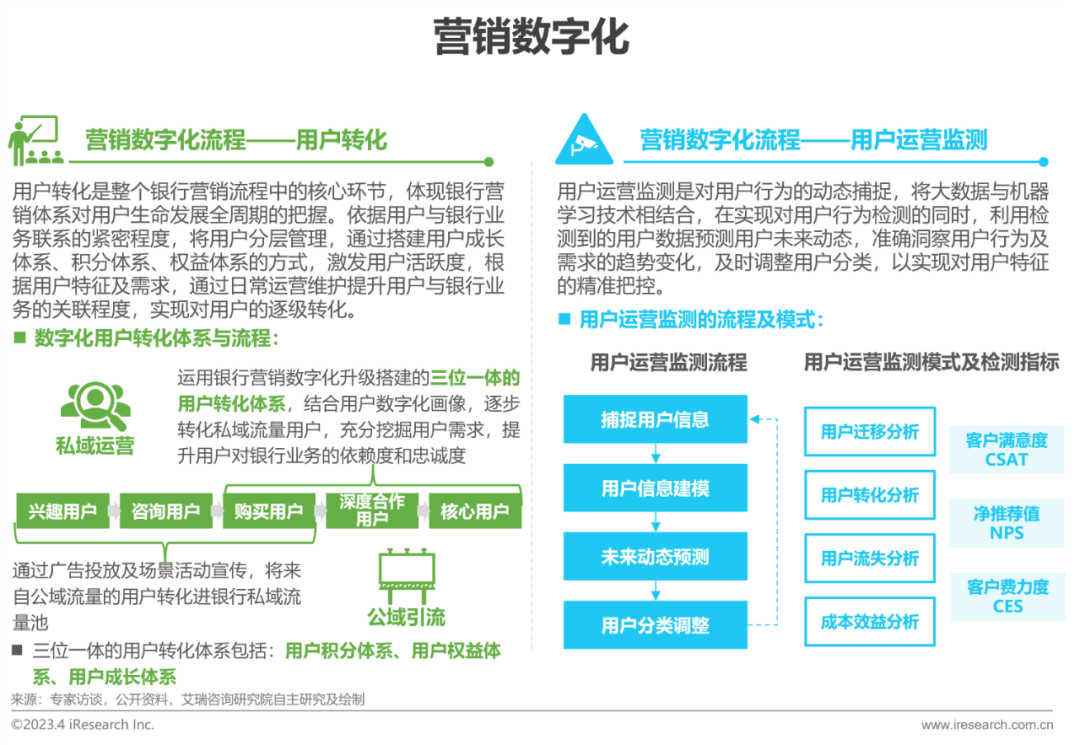

营销数字化作为在银行数字化能力建设中优先度、重要度与能力展现效果均位列前位的银行数字化能力评测指标,其对于银行整体的数字化升级效果的展现与影响力是不言而喻的。由于该项能力数字化升级效果易量化,银行受益直接,对于银行营销体系的数字化升级通常是银行“试水”数字化的第一步。营销数字化的核心是将传统银行业务由“客户导向”转变为“用户导向”,整个数字化营销流程全面围绕用户展开,以单个用户的实际需求为核心,结合大数据、云计算、人工智能等技术,精准刻画用户画像,全面捕捉用户生命周期。银行营销能力数字化升级按照其用户运营流程被分为四个阶段,依据每个阶段不同的业务重点,针对性的部署各业务环节的数字化升级模式,具体情况如下:

用户识别阶段的升级核心是用户身份确认与数字画像建设;渠道数字化是用户触达环节数字化升级的基础

三位一体的用户转化体系助力银行实现数字化用户运营及转化;运营监测系统动态捕捉用户行为,及时调整用户分类

5、数字化能力指标三:产品数字化

前沿技术应用赋能银行产品数字化设计、销售与迭代全流程

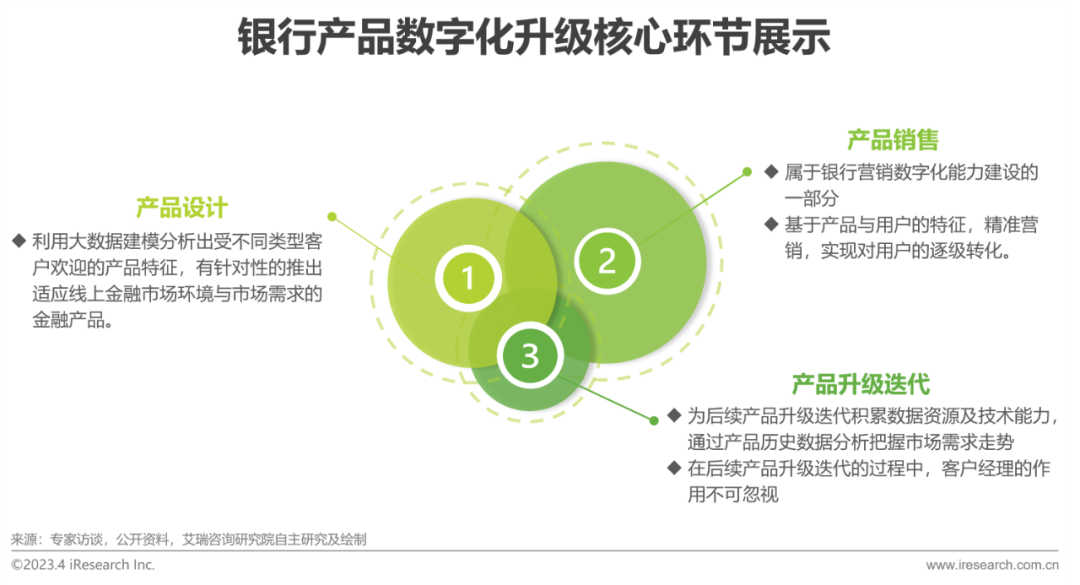

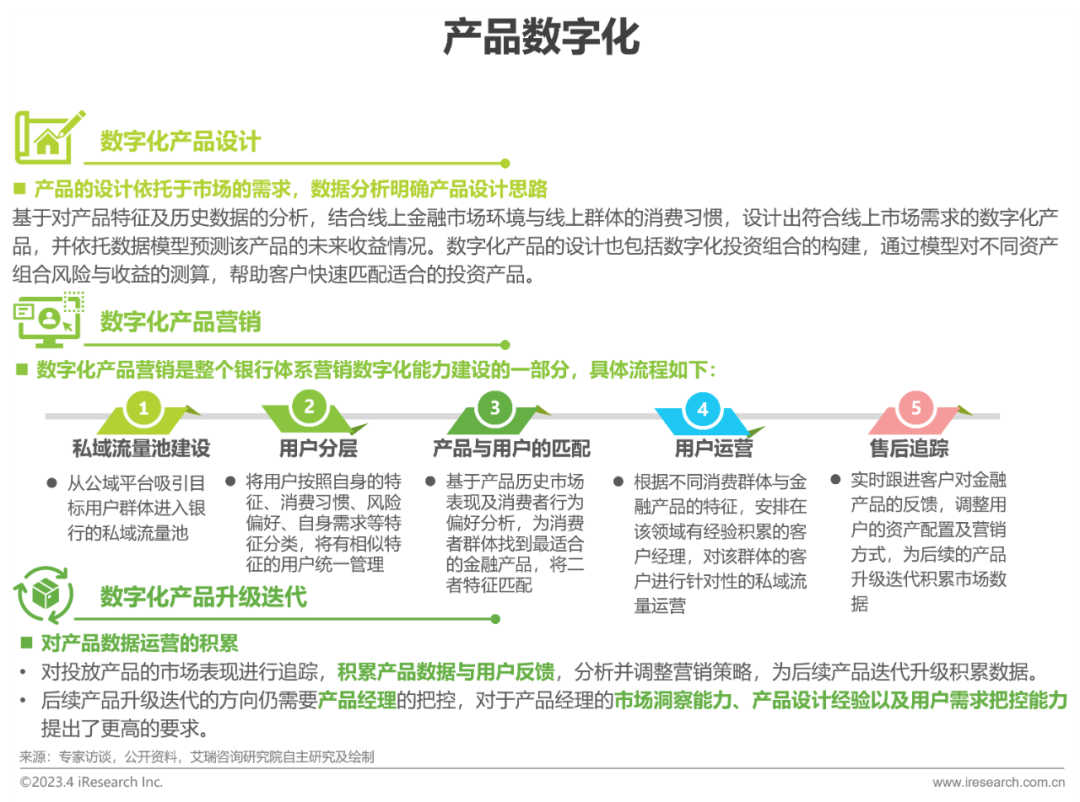

大数据、人工智能、云计算等前沿技术在银行产品领域同样得到了广泛的应用。对于银行来说,产品的数字化升级不仅仅是将其线下营业网点推出的信贷、理财等产品放到线上平台售卖,而是从产品的设计环节开始,重新塑造产品的价值链及商业模式,用数字化方式全面赋能产品从设计到销售、运营的每个环节,其数字化升级的核心主要体现在三个方面,分别是产品设计阶段的数字化能力应用,产品销售阶段的数字化智能营销以及后续产品的数字化运营与迭代升级。基于以上三方面的能力提升及业务模式转型,帮助银行实现产品领域的数字化、智能化提升。

基于用户及产品的历史数据分析,实现精准产品设计与营销

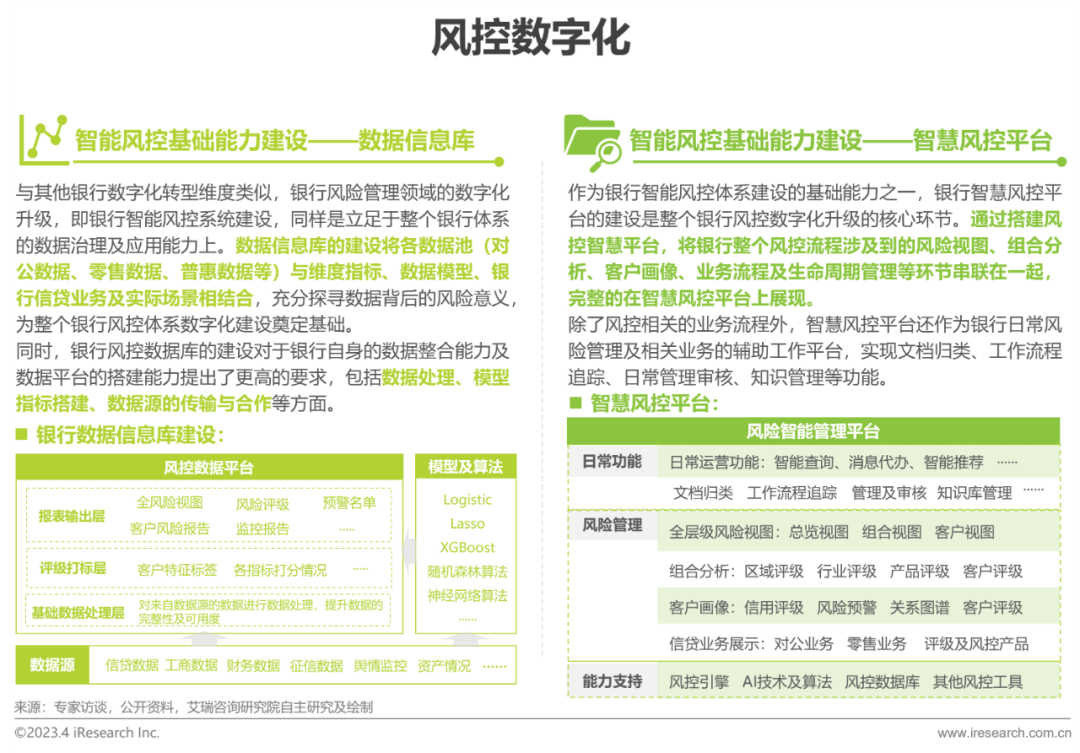

6、数字化能力指标四:风控数字化

银行智能风控体系由基础能力与业务能力两个核心部分组成

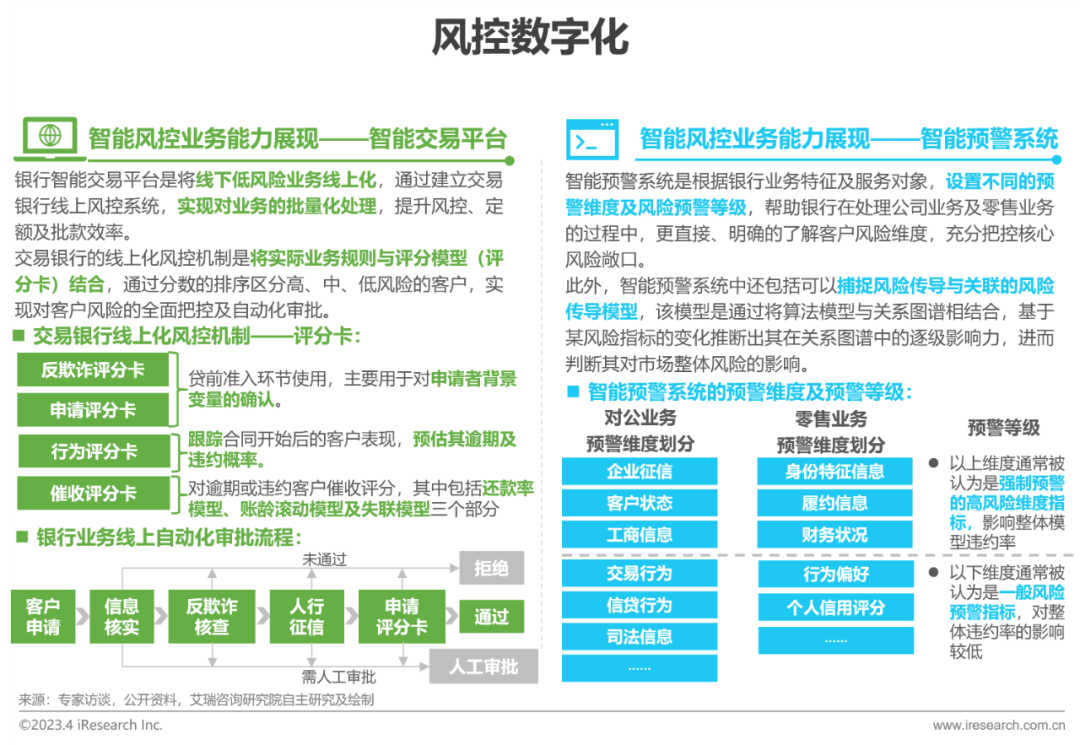

银行风险管理领域的数字化升级是整个银行系统数字化升级的核心部分,风控作为银行业务能力提升的重要辅助环节,其核心工作原理就是通过分析处理历史数据,得出风险等级并展望未来风险变动趋势。通过将大数据、人工智能、云计算等前沿技术与银行风控业务的汇总融合,帮助银行风控流程实现线上化、数字化、智能化,全面提升银行对于客户、行业及地域的风险把控能力,帮助银行在客户资格审核及贷款批复、资产管理及投资组合构建等方面降低风险水平,提升银行整体业务效果。银行智能风控体系搭建主要由基础能力及业务能力两个核心部分组成,基础能力体现在对于银行集团级风控数据信息库的建设以及智慧型风控平台的搭建上,业务能力主要包括对于银行智能交易平台及智能预警系统的使用。

银行数据信息库与智慧风控平台的建设是银行风控领域数字化、智能化升级的基础能力建设部分

银行智能风控业务能力主要体现在智能交易风控平台建设与智能预警系统使用两个方面

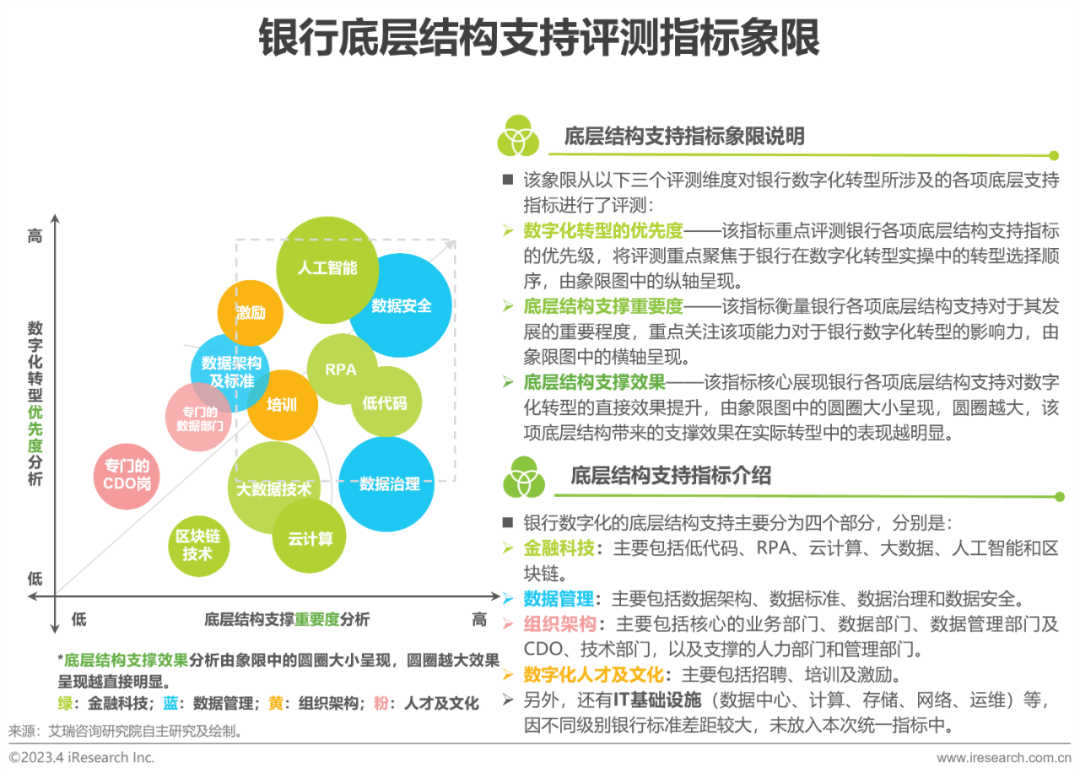

7、底层结构支持:数字化指标象限展示

通过优先度、重要度与支撑效果三重维度评测银行底层支撑

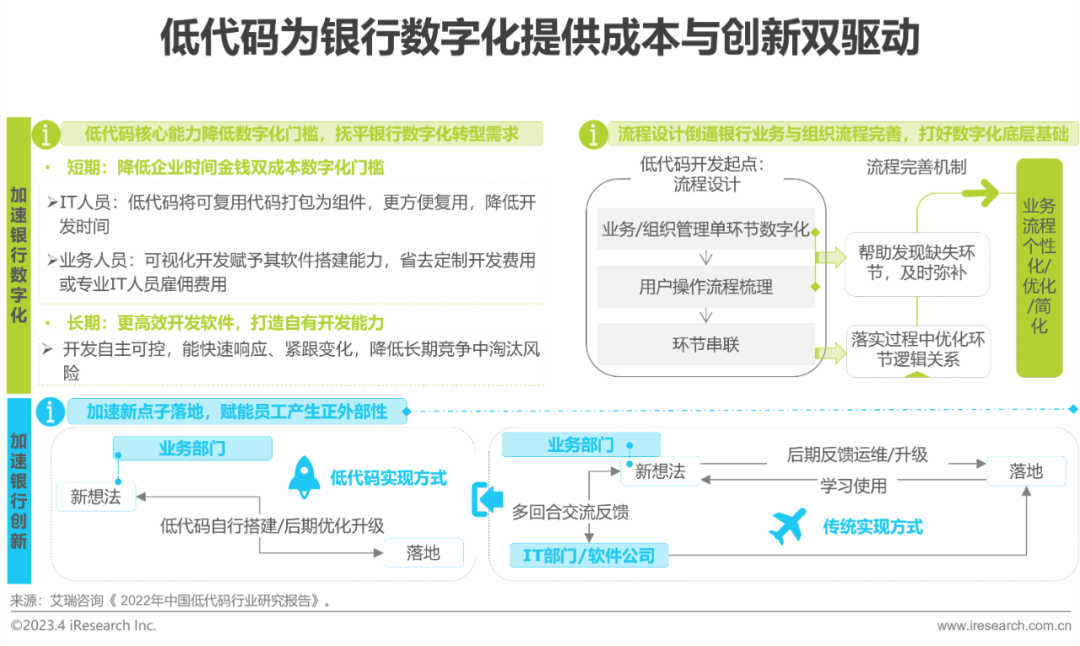

8、底层结构支持指标一:低代码

短期拉低数字化门槛,长期提升创新动力与技术自主性

中短期来看,低代码不仅赋能IT人员,提高复用及开发效率,同时赋能于银行业务人员,便于软件的自主搭建,降低数字化门槛。长期视角中,低代码平台将企业需求与自主开发深度融合,打造出可持续性的、紧跟变化的IT服务能力来经受瞬息万变的时代考验。但银行要在时代洪流中屹立不倒,仍需保持创新动力,而低代码赋予普通业务人员的开发技能可以促进新点子变现,激发员工创新,赋能银行探索第二甚至是第三曲线的描绘可能。

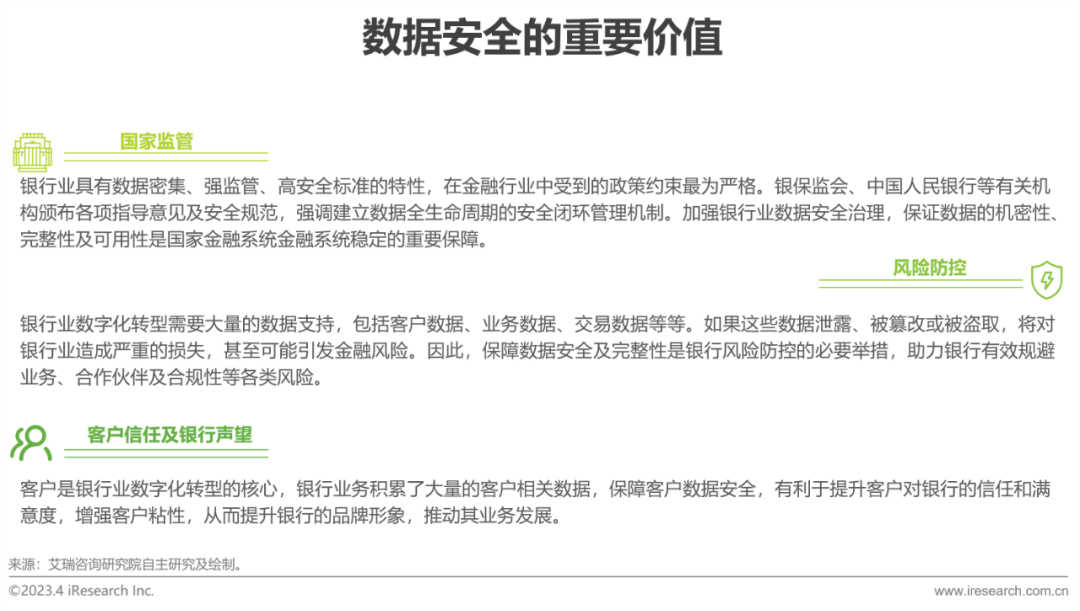

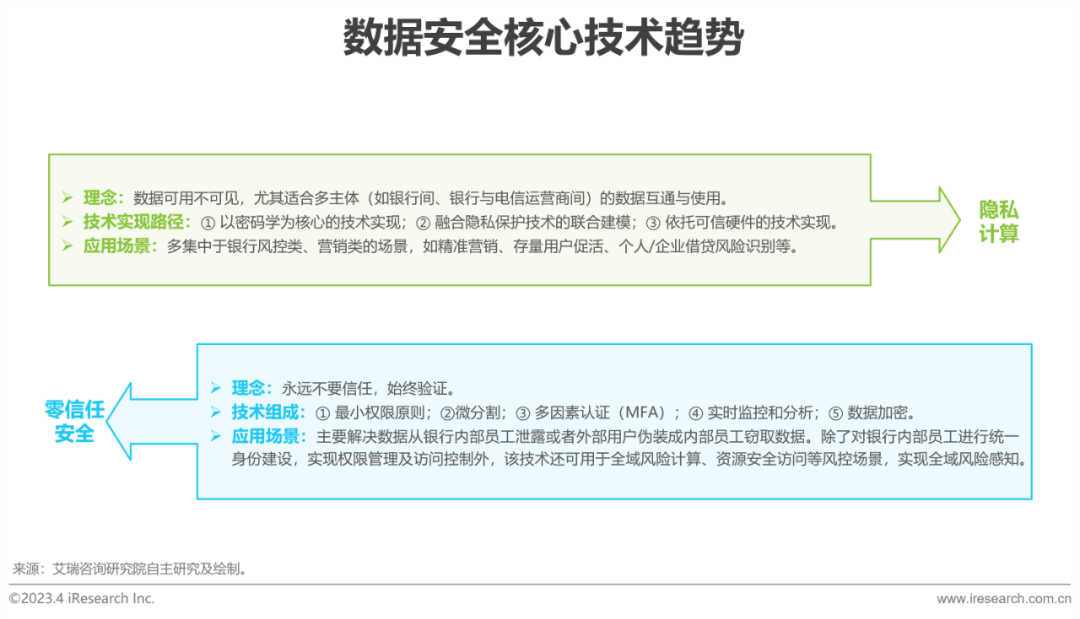

9、底层结构支持指标四:数据安全

多种技术配合,构建完整数据安全体系

数据安全是银行数字化转型重要的底层结构支撑。从国家和监管层面看:数据安全是金融系统稳定的重要保障,也是银行合规的重要考评标准。从银行自身风险看:数据安全是反欺诈和自身稳定运营的关键。从用户服务和声誉度看:数据安全可有效保障用户隐私,维护银行声誉。数据安全技术体系复杂,但根据目的,可以分为:(1)保障数据不被丢失,具体包括容灾、备份等技术。(2)保障数据不被篡改,具体包括防火墙、访问控制、监控和审计。区块链技术等。(3)保障数据不被泄露,具体包括加密技术、隐私计算、数据遮蔽等。数据安全大致可有两个方向:对数据本身进行控制(类似于强制存取控制)和对用户进行控制(类似于自主存取控制),前者属于狭义数据安全,后者与网络安全等关系密切,属于广义数据安全,两者相互配合,缺一不可。

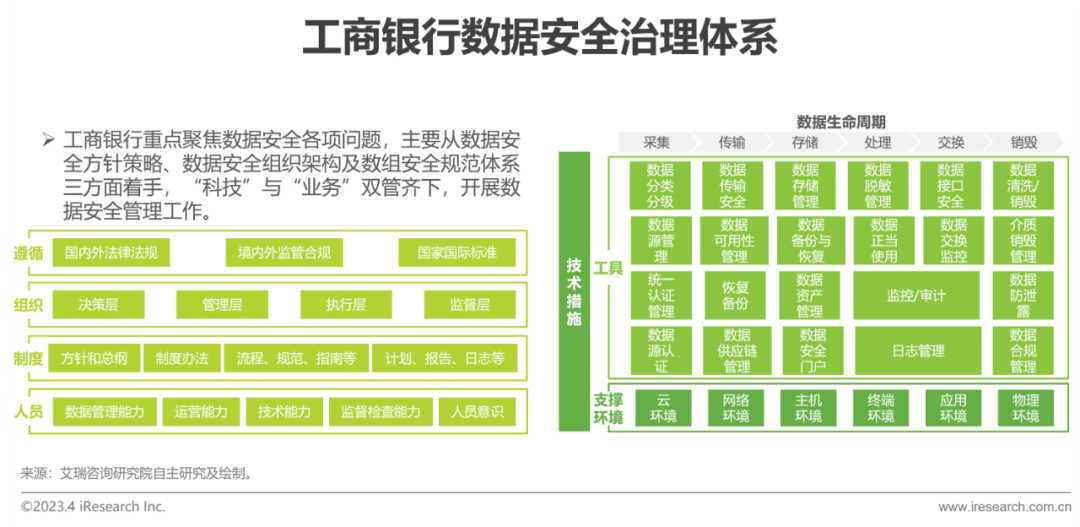

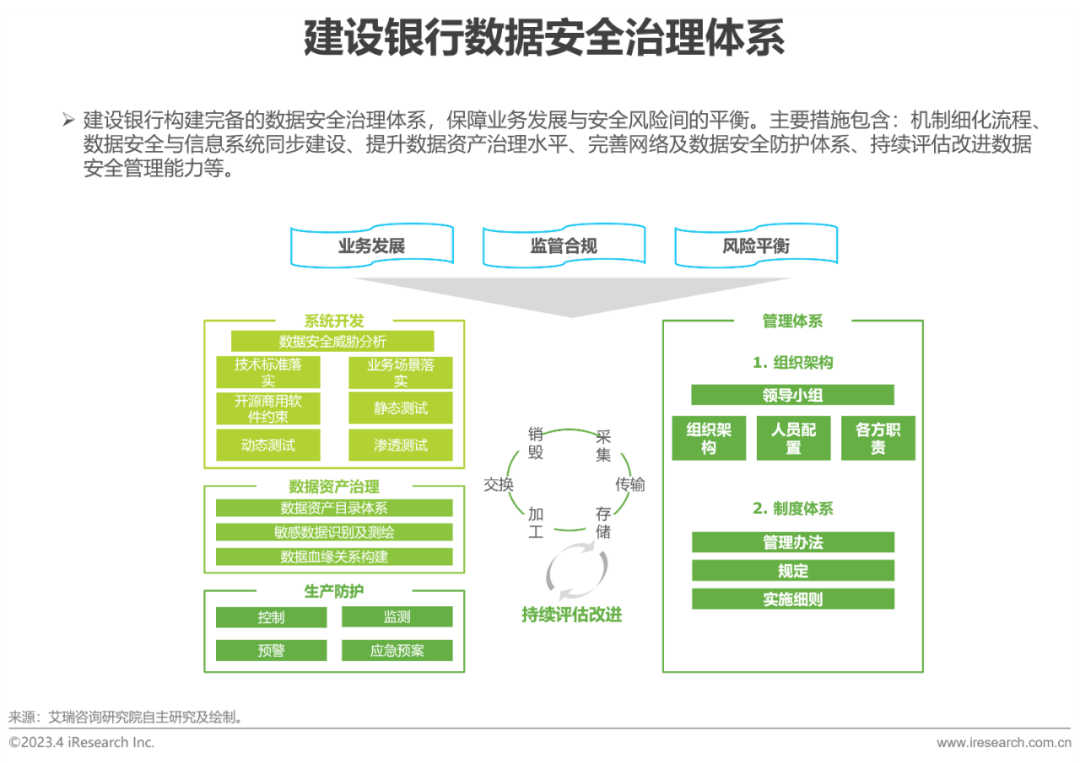

10、数据安全整体架构案例展示

银行数据安全治理体系标杆案

三、趋势洞见: 银行数字化发展趋势展望

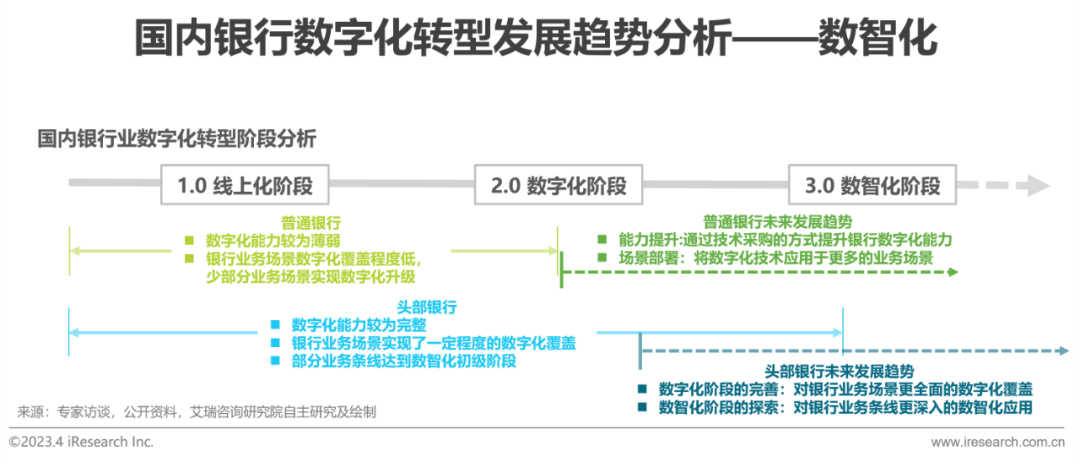

1、趋势及展望(一):数智化

银行数字化体系建设将更加完善,逐步覆盖更多业务场景,为用户提供全面、便捷的金融服务

从整个银行业金融科技赋能程度与数字化转型阶段来看,目前大多数国内银行仍处于转型1.0的线上化阶段,处于该阶段的银行数字化能力比较薄弱,在实现业务线上化的基础上,仅在少数几项业务板块(如:营销、风控等)探索性开展数字化业务的能力升级。对于头部大行来说,目前基本已经进入了银行数字化转型的2.0阶段,银行在业务数字化转型及应用方面的能力较为完整,对于银行业务场景也实现了一定程度的数字化覆盖,并且在某些业务条线,头部大行的技术能力应用也能够达到数智化初级水平。随着国内银行业在金融科技、IT系统建设等数字化领域投入成本的增加,银行数字化业务服务能力水平将进一步提升,前沿技术的融入将推动银行整体迈入数字化新阶段。与此同时,银行数字化转型进程的推进也将逐步覆盖更多的业务条线,特别是线上化难度大、业务较为复杂的对公业务条线,或将成为近几年数字化升级的重点发力方向。此外,银行数字化升级的业务板块也将会更多的关注用户体验与用户服务,将数字化、智能化技术应用于解决用户投诉、保护用户权益、产品智能决策等方面,在满足用户需求的同时利用数字化技术为用户带来更好的服务体验。

2、趋势及展望(二):开放性

数字化升级推动开放融合的金融生态体系建设,促进国内开放银行业务的发展

随着金融科技在银行业更广泛的应用以及国内商业银行数字化转型进程的推进,银行与客户之间的交互方式与服务模式正逐步发生改变,以用户为核心、与场景相融合的数字化金融生态建设将成为国内银行业未来发展的新趋势,由传统银行逐步向开放银行探索是国内银行业数字化发展与生态建设的“进阶之路”。开放银行是指商业银行通过标准化API、SDK、H5、小程序等连接方式与生态内金融科技公司、第三方开发者、供应商等其他合作伙伴相互融合,共享数据、算法、交易流程与其他业务功能,为生态内的合作伙伴输出金融服务能力,由生态内的其他参与者为用户提供场景化的金融服务,实现对于银行商业模式与经营模式的数字化重塑。此外,开放业务通过银行系统与产业平台、企业业务系统的连接,拓展了银行业务的服务边界,将终端服务客群衍生至传统银行服务难以触达到的长尾用户,全面释放生态内的数据价值与规模价值。

翻译:

Bank research report

Core summary:

Starting from the development background and current pain points of the banking digital industry, the report combs and analyzes the key elements of the digital transformation of Chinese commercial banks. Through a mature and perfect bank digital evaluation system built by iResearch’s senior team, the differentiated implementation path and technical demand of dismantling banks’ digital transformation are judged from two aspects of digital transformation ability and digital bottom support, and the future trend of bank digital intelligence, openness, agility and ecology is deeply gained. At the same time, this report selects the leading enterprises in the field of digital service of banks, analyzes the excellent cases of their service banks in depth, and finally selects the top 50 enterprises.

Background introduction and difficulty analysis of bank digital transformation

1. General trend: digital transformation of banking industry

The construction of digital China has become one of the biggest certainties in the future, and the banking industry should accelerate its digital transformation to adapt to the new social environment of digital economy

2. Top-level planning: Building a new pattern of digital finance

From the broad to the micro, the national digital transformation series of policies have been promoted, gradually building a new pattern of digital finance

3. The impact of COVID-19: Challenges in the post-pandemic era

The pandemic has prompted a surge in demand for “contactless” financial services and accelerated the process of banking going online

The epidemic has restricted offline financial activities and changed users’ financial business handling habits. Online channels and “contactless” financial services have attracted widespread attention from the market. In February 2020, China Banking and Insurance Regulatory Commission issued the Notice on Further Improving Financial Services for Epidemic Prevention and Control, requiring banks and insurance institutions to “actively promote online business” and “optimize and enrich the channels of ‘contactless service'”. Under the influence of the policy, the growth rate of lock-out transaction amount of China’s banking industry in 2020 was about twice that of 2019, increasing from 6.3% to 12.2% in one year.

In 2021, the growth rate of lock-out transaction amount remained at a high growth level, and the amount of lock-out transaction increased steadily for two consecutive years. The change of users’ financial business handling habits caused by the epidemic has promoted the online transformation process of banking business. “Contactless” financial services have put forward new requirements for banks’ channel construction capacity, technical structure construction, digital operation capacity and other aspects, which have brought lasting and far-reaching impacts on the digital development of banking industry and the change of financial service mode.

4. External competition: The entry of Internet companies has caused impact

The technical capability and ecological construction level of Internet companies exceed that of banks, and the market position of banks is shaken by the wave of financial “exchange” media

With the mature application of big data, artificial intelligence, cloud computing and other cutting-edge technologies in the Internet field, Internet enterprises give full play to their own advantages in technical capabilities, and apply the digital capabilities of new technologies in data analysis, model building, information protection and other aspects to the financial service field, bringing innovation in the service mode and operation mode for the traditional “deposit, loan and remittance” business of banks. While technology enables financial services, the exploration and technological innovation of Internet enterprises in the financial field have brought a great impact on the original business segments and market shares of commercial banks.

The wave of financial “exchange” media has gradually shaken the market position of banks in the financial field. In addition, Internet enterprises have inherent advantages in ecological capacity construction and ecological resource integration. They have the ability and resources to transfer user traffic obtained from high-frequency and high-demand platforms to e-commerce and financial sectors with high returns, eroding the customer resources of banks from the traffic inlet, and leading to the problem of sharp decrease of commercial banks’ traffic starting from the traffic port. It further affects the flow rate and business income of the whole ecosystem of banks, and gradually expands the advantages of Internet giants in traffic to deeper areas of high-yield business.

5. Internal input: The IT input of the banking industry has increased steadily year by year

In recent years, the scale of IT investment in domestic banking industry has steadily increased, and it is expected to grow at a compound growth rate of about 24.6%. In 2025, the scale of market investment will be close to 600 billion yuan

With the introduction of a series of national policies on digital transformation and the gradual maturity of the application of cutting-edge technologies in the field of financial services, the digital transformation of banks has become the general trend of the development of domestic commercial banks. In recent years, the investment scale of the domestic banking industry in the field of IT construction and service has been increasing year by year. Since 2019, the investment scale of the banking industry has been growing steadily and rapidly with a compound growth rate of 24%, and in 2022, IT will exceed 300 billion yuan. IT is expected that the investment scale of the domestic banking industry in the future will maintain a high growth trend with a compound growth rate of about 24.6%. It will reach nearly 600 billion yuan by 2025.

6. Technological progress: cutting-edge technology is highly compatible with the banking industry

The mature development of underlying technology and emerging technology has become the booster of bank digital transformation

Digital transformation cannot be separated from solid technical support. Increasingly mature underlying technologies such as big data, cloud computing and AI complement each other with emerging technologies derived from digital scenarios, enabling many banking business scenarios. For example, intelligent customer service: Dialogue robots based on natural language understanding can replace part of human customer service, reduce labor costs and improve the efficiency of problem solving. Intelligent clearing: Build a supply chain finance platform based on blockchain, complete the trusted flow of data, and enable enterprise customers to realize more convenient and safe automatic clearing.

Credit risk management: Mainly through big data technology to identify information asymmetry problems, fraud identification, credit scoring, post-loan management and other risk management. Under the background of today’s new digital infrastructure, relying on the full stack technical capabilities of “ABCDE” (artificial intelligence (AI), big data (BigData), Cloud (Cloud), Internet of Things (Device) and frontier Exploration), to create digital products, channels, operations and ecological system. Has become to promote the banking industry digital upgrade just need.

Detailed explanation of the model and landing guide

1. Introduction of model building logic

The evaluation model consists of three parts: top-level strategic planning as the core drive, digital capacity construction as the capability display. And bottom structure support as the transformation guarantee

2. Digital capacity building: digital index quadrant display

The transformation level of digital capability of banks is evaluated through three dimensions of priority, importance and ability display effect

3. Index of digital ability 1: channel digitization

Channel digitization consists of online channel construction and offline channel linkage

Channel construction is the basic link of banking business. And the effect of its digital transformation will directly affect the digital performance of banks in marketing, products, risk control and other fields. The construction of digital channels and the realization of intelligent linkage among channels are not only the priority in the process of bank digital transformation. But also the indispensable key part for the development of bank business and the presentation of the effect of digital transformation. The channel digitalization capability of banks is mainly reflected in three aspects. Namely, the digital transformation of bank offline outlets. The construction of online digital channels and the linkage and communication among channels. The subsequent content will focus on the above three aspects to carry out the analysis of the bank channel digitalization construction capability.

The introduction of intelligent tools to facilitate the digital upgrading of offline branches of banks. Online banking, mobile banking and other online platforms have become the gathering place of online banking users

Business linkage depends on the bank’s management ability and the establishment of business interconnection system

4. Index 2 of digital ability: marketing digitalization

Establish a digital marketing system with user operation as the core. And provide precise marketing services around the whole life cycle of users

Marketing digitalization, as an evaluation index of bank digitalization capability with priority. Importance and ability display effect ranking first in bank digitalization capability construction. Has a self-evident influence on the overall digitalization upgrade effect of the bank. As the digital upgrading effect of this capability is easy to quantify, the bank will benefit directly. The digital upgrading of the bank marketing system is usually the first step for the bank to “test the water” of digitalization. The core of marketing digitization is to transform traditional banking business from “customer oriented” to “user oriented”.

The whole digital marketing process is fully developed around users. With the actual needs of individual users as the core, combined with big data, cloud computing, artificial intelligence and other technologies. To accurately depict user portraits and fully capture user life cycle. The digital upgrade of the bank’s marketing capability is divided into four stages according to its user operation process. According to the different business focus of each stage. The digital upgrade mode of each business link is targeted to be deployed. The specific situation is as follows:

The upgrade core of user identification stage is user identity confirmation and digital portrait construction. Channel digitization is the foundation of digital upgrade of user touch link

The trinity user conversion system helps the bank realize the digital user operation and transformation. Operation monitoring system dynamically captures user behavior and timely adjusts user classification

5. Index 3 of digital ability: product digitalization

The application of cutting-edge technology enables the whole process of digital design, sales and iteration of bank products

Big data, artificial intelligence, cloud computing and other cutting-edge technologies have also been widely used in bank products. For banks, the digital upgrade of products is not only about selling credit and finance products launched in offline business outlets on online platforms. But also about reshaping the value chain and business model of products starting from product design. And comprehensively empowering every link from product design to sales and operation in a digital way. The core of its digital upgrading is mainly reflected in three aspects. Namely, the application of digital capability in the product design stage, the digital intelligent marketing in the product sales stage. And the digital operation and iterative upgrading of subsequent products. Based on the above three aspects of ability improvement and business model transformation. Help banks to achieve digital and intelligent promotion in the product field.

Based on historical data analysis of users and products, accurate product design and marketing can be realized

6. Index 4 of digital ability: Digitized risk control

Bank intelligent risk control system consists of two core parts: basic ability and business ability

The digital upgrade in the field of bank risk management is the core part of the digital upgrade of the whole banking system. As an important auxiliary link for the improvement of banking business capability. Risk control is the core working principle of which is to analyze and process historical data. Obtain the risk level and forecast the trend of future risk changes. By putting a big data, artificial intelligence, cloud computing and other cutting-edge technology with the bank’s risk control business summary of fusion, help Banks’ risk control process to achieve online, digital, intelligent, improve the risk of bank for the customer, industry and regional control ability, help the bank loan in customer qualification review and approval, asset management and portfolio construction to reduce the level of risk, Improve the overall business effect of the bank.

The establishment of a bank’s intelligent risk control system mainly consists of two core parts: basic competence and business competence. The basic competence is reflected in the construction of the bank’s group-level risk control data information base and the construction of the intelligent risk control platform. The business competence mainly includes the use of the bank’s intelligent trading platform and intelligent early warning system.

The construction of bank data information base and intelligent risk control platform is part of the basic capacity construction of digitized and intelligent upgrading in the field of bank risk control

The intelligent risk control business ability of banks is mainly reflected in the construction of intelligent transaction risk control platform and the use of intelligent early warning system

7. the underlying structure support: digital index quadrant display

The bank bottom support is evaluated by three dimensions of priority, importance and support effect

8. the underlying structure support index one: low code

In the short term, it lowers the digital threshold, and in the long term. It improves the impetus of innovation and the autonomy of technology

In the short and medium term, low code not only enables IT personnel to improve reuse and development efficiency. But also enables banking personnel to facilitate the independent construction of software and lower the threshold of digitalization. In the long term, the low code platform will deeply integrate the needs of enterprises with independent development. And create sustainable IT service capabilities that keep up with changes to withstand the test of the rapidly changing times. But if banks are to survive The Times, they still need to be motivated to innovate. And the development skills that low code enforces in ordinary business people can facilitate the realization of new ideas, stimulate innovation among employees. And enable banks to explore the possibility of tracing the second or even the third curve.

9. The underlying structure supports index four: data security

A variety of technical cooperation, the construction of a complete data security system

Data security is an important underlying structure support for bank digital transformation. From the national and regulatory level:. Data security is an important guarantee for the stability of the financial system, and also an important evaluation standard for bank compliance. From the bank’s own risk: data security is the key to anti-fraud and its own stable operation. From the perspective of user service and reputation:. Data security can effectively protect user privacy and maintain the reputation of the bank.

Data security technology system is complex, but according to the purpose, it can be divided into: (1) To protect data from loss, including disaster recovery, backup and other technologies. (2) Protect data from tampering, including firewall, access control, monitoring and audit. Blockchain technology, etc. (3) Protect data from being leaked, including encryption technology, privacy computing, data masking, etc. Data security can be roughly divided into two directions: control of data itself (similar to mandatory access control) and control of users (similar to autonomous access control). The former is a narrow sense of data security, while the latter is closely related to network security and so on, belonging to a broad sense of data security.

10. Case presentation of overall data security architecture

Bank data security governance system benchmarking case

Insight into the Trend: The prospect of digital development trend of banks

1. Trends and Prospects (I) : digital intelligence

The construction of the digital banking system will be more complete, gradually covering more business scenarios, and providing users with comprehensive and convenient financial services

From the perspective of fintech enabling degree and digital transformation stage of the whole banking industry, most domestic banks are still in the online stage of transformation 1.0, and the digital capability of banks in this stage is relatively weak. Based on the realization of online business, only a few business sectors (such as marketing, risk control, etc.) are exploratory to carry out digital business capability upgrade. For the top bank, it has basically entered the 2.0 stage of banking digital transformation. The capability of the bank in the aspects of business digital transformation and application is relatively complete, and the digital coverage of the banking business scenario has been realized to a certain extent. In some business lines, the application of the technical capability of the top bank can also reach the primary level of digital intelligence.

With the increase of investment costs in digital fields such as fintech and IT system construction in the domestic banking industry, the level of digital business service capacity of banks will be further improved, and the integration of cutting-edge technologies will promote the whole bank to enter a new digital stage. At the same time, the promotion of the digital transformation process of banks will gradually cover more business lines, especially the online business lines which are difficult and complicated, and may become the focus of digital upgrading in recent years. In addition, the business section of the bank’s digital upgrade will also pay more attention to user experience and user service, and apply digital and intelligent technology to solve user complaints, protect user rights and interests, intelligent product decision-making and other aspects. While meeting user needs, digital technology will bring better service experience to users.

2. Trends and Prospects (II) : Openness

Digital upgrading promotes the construction of an open and integrated financial ecosystem and promotes the development of open banking services in China

With the wider application of fintech in the banking industry and the advancement of the digital transformation process of domestic commercial banks. The interaction mode and service mode between banks and customers are gradually changing. The construction of a user-centered digital financial ecology integrated with the scene will become a new trend in the future development of domestic banking industry. The exploration from traditional bank to open bank is the “advanced road” of digital development and ecological construction of domestic banking industry.

Open banking refers to the integration of commercial banks with fintech companies, third-party developers, suppliers and other partners in the ecosystem through standardized API, SDK, H5, small programs, etc., to share data, algorithms, transaction processes and other business functions, and export financial service capabilities to partners in the ecosystem. Other participants in the ecosystem provide scenario-based financial services to users, realizing the digital reshaping of the bank’s business model and operation model. In addition, open business expands the service boundary of banking business by connecting banking system with industrial platform and enterprise business system, derivatives terminal service customer base to long-tail users that traditional banking services cannot reach. And fully releases the data value and scale value within the ecosystem.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源于艾瑞咨询 ;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(https://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。