2023年5月6日 北京

IDC《2022年第四季度中国IT安全硬件市场跟踪报告》显示,2022年第四季度中国IT安全硬件市场厂商整体收入约为14.6亿美元,同比下降3.1%。结合全年数据,2022全年中国IT安全硬件市场规模达到36.5亿美元,规模增速不及预期,同比下降3.3%。

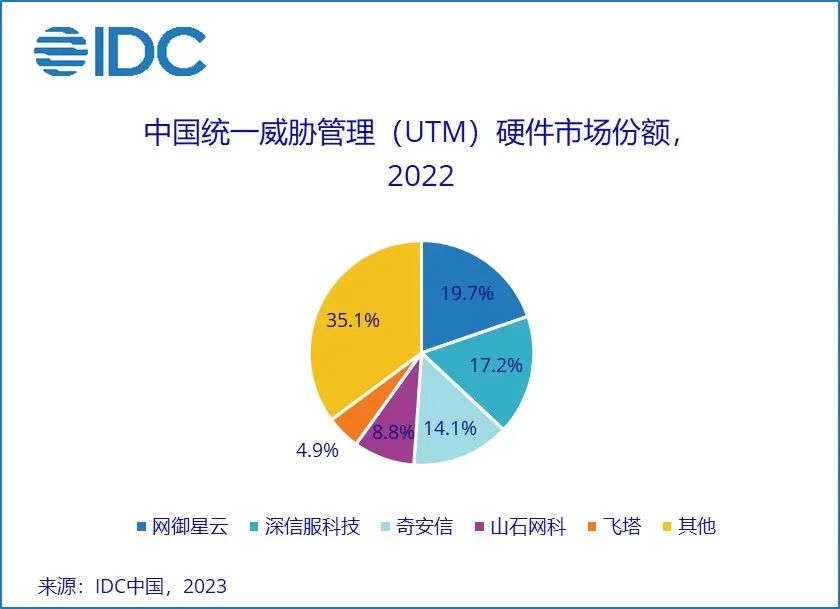

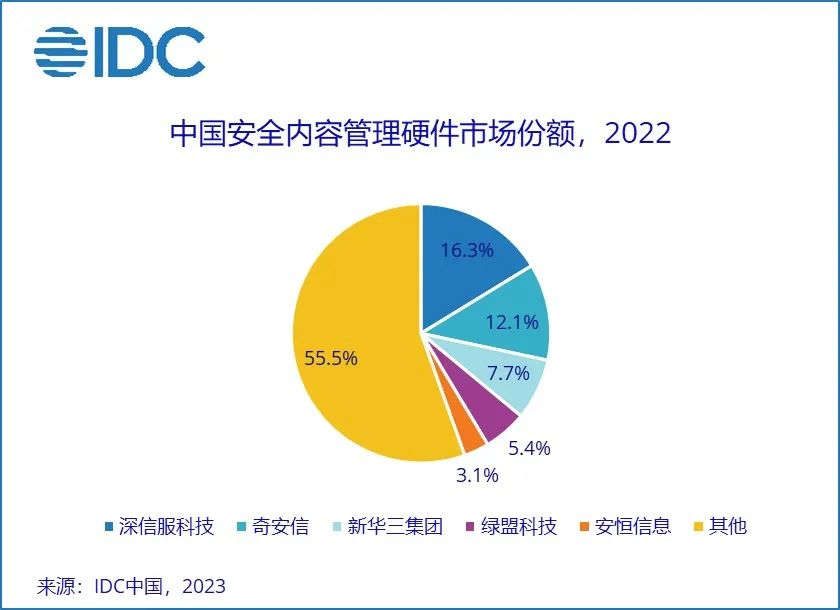

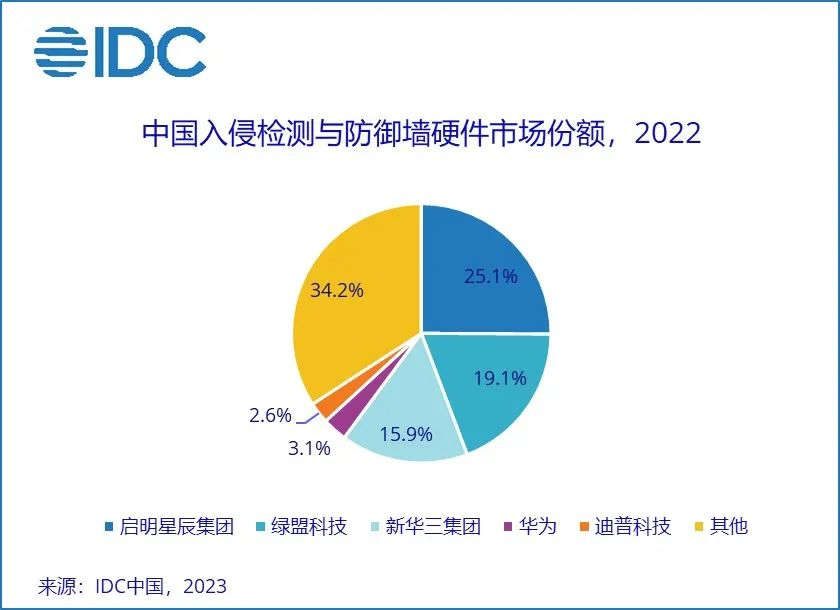

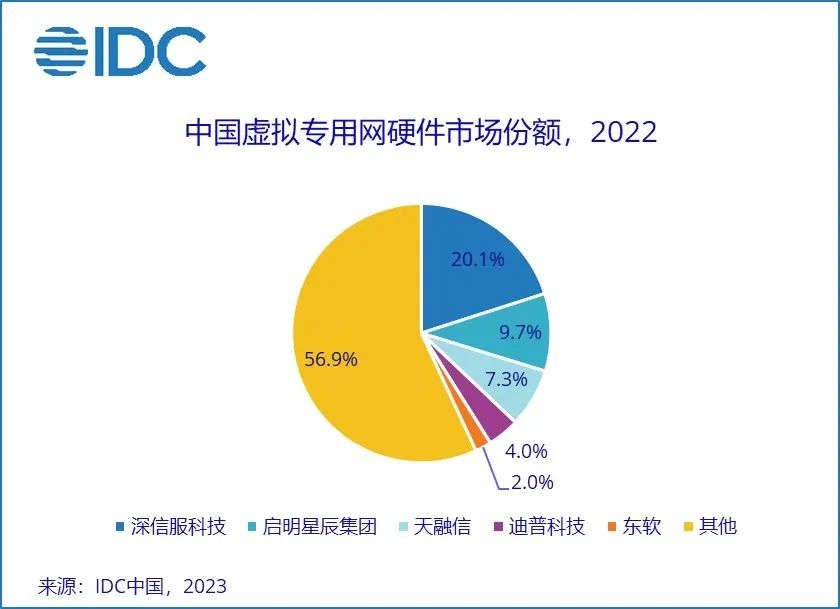

IDC定义下的网络安全硬件市场分别由统一威胁管理 (UTM)、基于UTM平台的防火墙 (UTM Firewall) 、安全内容管理(SCM)、入侵检测与防御 (IDP)、虚拟专用网(VPN)、传统防火墙 (Traditional Firewall) 构成。2022年中国网络安全硬件市场的关键厂商表现如下:

特殊说明:由于传统防火墙市场规模目前在不断缩减,故下图无传统防火墙关键厂商相关内容;另,由于数字四舍五入的原因,数字可能存在微小误差。

总体来看,2022年中国网络安全硬件市场数据表现如下:

- 基于UTM平台的防火墙市场规模仍保持第一,2022年总体市场规模约为11.7亿美元;

- 受疫情、经济、地缘政治、汇率等因素的影响,网络安全硬件产品六大子市场全年规模均呈现同比负增长。其中,安全内容管理市场受融合产品及客户需求的影响,降幅最快,全年规模同比下降6.3%;

- 政府、运营商、金融三大行业用户仍为网络安全硬件的投资主力。在国家政策和企业数字化转型等因素的驱动下,制造业、公共事业、能源等行业展现出了对网络安全硬件产品需求的快速增长;

- 与2021年全年相比,北部地区是唯一展现出网络安全硬件收入规模正增长的区域。

IDC中国高级分析师张雪卿表示,根据规律,四季度应为中国网络安全市场营收规模最大的单一季度。但是受到疫情反复和防疫政策调整的影响,各地区政府集中应对疫情爆发,在网络安全硬件方面的支出趋于保守。同时,疫情对经济的持续冲击对企业在网络安全硬件的投入带来负面影响。在疫情、政策等不确定因素的影响下,多数企业选择观望,相应预算有所收紧。值得注意的是,2022年美元对人民币汇率经历了多轮波动,美元显著走高,进一步拉低了2022年网络安全硬件规模,全年收入罕见出现同比负增长。2023年,随着抗疫成果的持续显现,市场逐步有序放开,基本于2023年一季度实现了全面复产复工,市场回暖的时间线有所提前。IDC预计,2023年中国网络安全硬件市场同比增速将达到17.8%,仍存在许多机会点。

翻译:

Beijing, May 6, 2023

According to IDC’s “China IT Security Hardware Market Tracking Report in the fourth Quarter of 2022”, the overall revenue of China’s IT security hardware market vendors in the fourth quarter of 2022 was about $1.46 billion, down 3.1% year-on-year. Combined with the annual data, the annual scale of China’s IT security hardware market reached 3.65 billion US dollars in 2022, and the scale growth was less than expected, down 3.3% year-on-year.

The network security hardware market as defined by IDC consists of Unified Threat Management (UTM), UTM platform-based Firewall (UTM Firewall), security Content Management (SCM), Intrusion detection and Prevention (IDP), virtual Private network (VPN), and Traditional firewall (Traditional firewall) Firewall). The key vendors in China’s cybersecurity hardware market in 2022 will perform as follows:

Special note: As the traditional firewall market size is currently shrinking, the following figure does not contain relevant content of traditional firewall key vendors; In addition, there may be minor errors in the numbers due to rounding.

Overall, the data performance of China’s network security hardware market in 2022 is as follows:

1. The firewall market size based on the UTM platform remains the first. With an overall market size of about $1.17 billion in 2022.

2. Affected by the epidemic, economy, geopolitics, exchange rate and other factors, the six sub-markets of network security hardware products showed negative year-on-year growth throughout the year. Among them, the security content management market was affected by converged products and customer demand, the fastest decline, the annual scale decreased by 6.3%;

3. Government, operators, and financial users are still the main investment forces in network security hardware. Driven by factors such as national policies and enterprise digital transformation, the manufacturing, public utilities. And energy industries have shown rapid growth in demand for cybersecurity hardware products.

4. The Northern region is the only region to show positive growth in cybersecurity hardware revenue compared to the full year 2021.

Zhang Xueqing, senior analyst at IDC China

Zhang Xueqing, senior analyst at IDC China, said that according to the rule. The fourth quarter should be the largest single quarter of revenue in China’s network security market. However, affected by the recurrence of the epidemic and the adjustment of epidemic prevention policies, regional governments concentrated on responding to the outbreak, and their spending on network security hardware tended to be conservative. At the same time, the continuous impact of the epidemic on the economy has a negative impact on enterprises’ investment in cybersecurity hardware. Under the influence of uncertain factors such as the epidemic and policies. Most enterprises choose to wait and see, and the corresponding budget has been tightened.

It is worth noting that the exchange rate of the US dollar against the RMB in 2022 has experienced multiple rounds of fluctuations. And the US dollar has risen significantly, further dragging down the scale of cybersecurity hardware in 2022. And the annual revenue has rarely experienced negative year-on-year growth. In 2023, with the continuous emergence of the anti-epidemic results. The market was gradually opened up in an orderly manner. And the full resumption of production and work was basically achieved in the first quarter of 2023. And the time line of the market recovery was advanced. IDC expects that the growth rate of China’s network security hardware market will reach 17.8% in 2023, and there are still many opportunity points

本文由数字化转型网(www.szhzxw.cn)转载而成,来源于IDC中国;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(https://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。