一、航母级的油气龙头

1、公司基本概况

中国石油天然气股份有限公司(以下简称“中国石油”或“公司”)是中国油气行 业占主导地位的最大的油气生产和销售商,也是世界最大的石油公司之一。公司创立 于 1999 年 11 月 5 日,是在原中国石油天然气集团公司(现中国石油天然气集团有限公 司,简称 “中国石油集团”)重组改制基础上设立的股份有限公司。公司发行的 H 股及 A 股于 2000 年 4 月 7 日及 2007 年 11 月 5 日分别在香港联合交易所有限公司(“香港联 交所”)及上海证券交易所挂牌上市(香港联合交易所股票代码 857,上海证券交易所 股票代码 601857)。中国石油广泛从事与石油、天然气有关的各项业务,是集国内外油 气勘探开发和新能源、炼化销售和新材料、支持和服务、资本和金融等业务于一体的 综合性国际能源公司。

国资委实际控股,子公司业务广泛。公司的直接控股股东为中国石油天然气集团 有限公司,其持有 82.46%的公司股权,而中国石油天然气集团有限公司是国务院国有 资产监督管理委员会直属的特大型国有企业,故国务院国资委为公司实际控股人。 公司目前在世界范围内拥有多家全资子公司、合营联营公司,业务覆盖石油天然 气勘探开采、运输销售,石油炼制、石油化工及其它化工产品和新材料的生产与储运 销,石油、天然气、石化产品及其他服务与技术的进出口,新能源开发等活动。

中国石油主营业务分为 4 大板块:油气和新能源、炼油化工和新材料、天然气销 售、销售。其中油气和新能源涉及原油和天然气的勘探、开发、生产和销售以及新能 源业务,炼油化工和新材料板块主要包括原油及石油产品的炼制,基本及衍生化工产 品、其他化工产品的生产和销售以及新材料业务,销售板块主要涉及炼油产品和非油 品的销售以及贸易业务,天然气和管道板块主要包括天然气销售,以及油气管道输送。

2、公司业绩情况

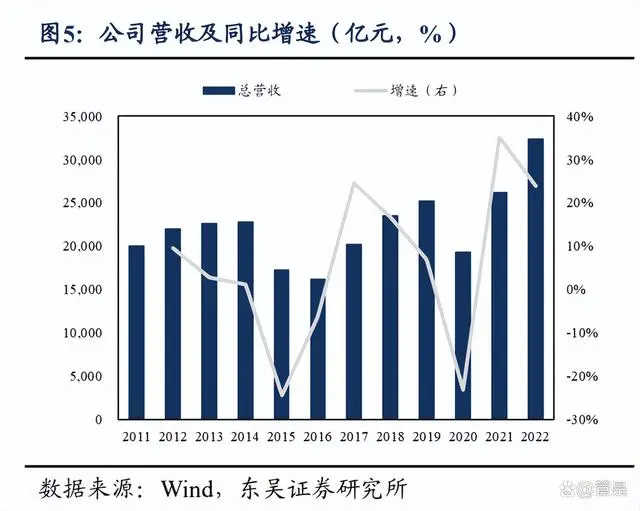

公司净利润与油价呈高度正相关。2020 年新冠疫情冲击,国内生产生活停滞,油 价暴跌,公司盈利受到较大影响,营业收入下降 23.2%,归母净利润下降 58.4%。随着 疫情影响减弱以及国际油价回升,公司盈利大幅度回升,2021 年营业收入上涨 35.2%, 归母净利润上涨 385.0%;2022 年俄乌冲突催化下国际油价创新高,公司盈利继续上涨, 公司营业收入为 32391.7 亿元,同比上涨 23.9%,归母净利润为 1493.8 亿元,同比上涨 62.1%。

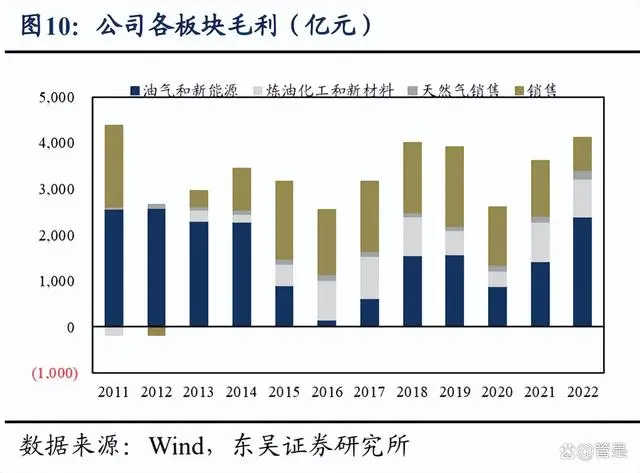

2022 年油气和新能源板块是主要利润来源。从营收来看,销售板块对公司营业收 入的贡献最大。从毛利率来看,油气和新能源板块与油价高度正相关,炼化和新材料 板块、销售板块与油价负相关,天然气销售板块的毛利率长期处于低位。从毛利来看, 高油价时期主要由油气和新能源板块贡献业绩,低油价时期主要由销售板块贡献业绩, 2022 年油价高企,油气和新能源板块毛利达到 2400 亿元,同比增长 67.5%。

资本开支水平稳定,炼化投资高峰已过。2018 年以来,中石油资本开支水平基本 保持稳定。2021-2023E,油气和新能源板块支出占比稳定在 80%,炼化和新材料板块 支出占比由 21.7%持续降至 14.0%,炼化项目投资高峰即将过去。2022 年公司实际资本 开支为 2743 亿元,2023 年公司计划资本开支为 2435 亿元,相比去年同期计划资本开 支水平提升 0.62%,相比去年同期实际资本开支水平降低 11.23%。

3、公司财务状况

疫后销售净利率和净资产收益率回升,盈利能力提升。2011-2022 年油价周期波动 中,公司的销售净利率波动,在 1.5%~7.5%范围内,且在 2016 年和 2020 年油价低迷时 也显示出了较强的抗冲击性,仍然保持正销售净利率和 ROE。2020 年疫情冲击后,中 石油的销售净利率和 ROE 明显回升。公司资产负债率稳定且适中。近十年,公司的资产负债率稳定在 45%左右,体现 了公司稳健的财务状况。与国内外石油公司相比,公司资产负债率处于适中水平。 公司经营现金流增加,夯实财务基础。近五年,公司经营性现金流充足且稳定维 持在 3500-4000 亿元,且 2021~2022 年连续上涨,为公司运营发展所需的高强度资本支 出提供了资金支持。

二、油气和新能源:稳油增气步伐不停,新能源业务全面提速

1、油气和新能源业务板块情况

中国石油是我国最大的油气生产商,公司在上游主营石油与天然气勘探开采业务, 拥有大庆、长庆、塔里木、西南、新疆、辽河等多个大型油气区。其中,大庆油区是中 国最大的油田,2022年全年实现原油产量3003万吨,已连续8年保持在3000万吨以上; 长庆油田是中国最大的油气田,2022 年产原油 2570 万吨、天然气 506.5 亿立方米,全年 油气产量当量攀上 6500万吨新高峰。此外,在非常规领域,中石油还积极推进页岩油、 页岩气国家级示范区建设,一体化全力推进页岩油气勘探开发,2022 年页岩油气总产量 分别较 2018 年增长 2.9 倍、2.3 倍。

油气和新能源板块经营效益与油价高度相关。公司油气和新能源板块经营收入与 油价波动正相关,板块毛利率随油价波动较大。2022 年,油价大幅上涨环境下,板块 毛利同比+67.5%至 2400.1 亿元,毛利率同比+5pct 至 26.40%。

公司上游资本支出变化与油价正相关,同时也受到国家增储上产政策影响。2022 年公司资本性支出 2743亿元。其中,油气和新能源部分资本支出为人民币 2216 亿元, 主要用于:国内塔里木、四川、鄂尔多斯、准噶尔、松辽、渤海湾等重点盆地的规模 效益勘探生产,加大页岩气、页岩油等非常规资源开发力度,推进清洁电力、CCUS 等 新能源工程;海外积极应对形势变化,聚焦重点区块深化规模效益勘探,加强中东、 中亚、美洲等重点项目产能建设,持续优化业务布局和资产结构。

预计 2023年油气和新能源分部的资本性支出为人民币 1955 亿元,主要是继续加强 国内松辽、鄂尔多斯、准噶尔、塔里木、四川、渤海湾等重点盆地的规模效益勘探开 发,加大页岩气、页岩油等非常规资源开发力度,推进清洁电力、CCUS、氢能示范等 新能源工程;海外提高业务发展集中度,推动高效发展,做好中东、中亚、美洲、亚 太等合作区现有项目的经营同时,加大优质项目获取力度,持续优化资产结构、业务 结构和区域布局。中石油油气操作成本优势突出。过去五年,中石油、中石化的油气操作成本较为 稳定,分别在 11-13 美元/桶、14-17 美元/桶之间浮动,且中石油的单桶油气操作成本更 低。较低的油气操作成本使公司即使在油价低谷期也能维持正常经营。油气操作成本 优势有效地保证了公司的盈利空间,巩固了龙头的竞争优势。

公司坚持高效勘测,稳油增气取得新进展。在原油开发方面,公司立足重点区带 加大风险勘探力度,强化鄂尔多斯中生界常规油、松辽古龙页岩油等增储领域集中勘 探,同时抓好准噶尔玛湖沙湾新层系、四川栖霞—茅口等战略接替领域甩开勘探,力 争取得战略性发现和突破。2022 年,公司原油产量 9.06 亿桶,同比增长约 2.1%。2023 年,公司计划原油产量为 9.13 亿桶,同比增长 0.7%。 在天然气开发方面,公司加快推进气田产能建设。其中,长庆、西南、塔里木三 大气区是产量及产量增量的主体。2022 年,公司天然气产量为 46750 亿立方英尺,在 油气产量当量中占比达 46.23%。2023 年,公司计划天然气产量为 48889 亿立方英尺, 同比增长 4.6%。 综合来看,2022 年公司油气产量当量为 16.9 亿桶,同比增长约 3.73%。2023 年, 公司计划油气产量当量为 17.28 亿桶,同比增长 2.51%。

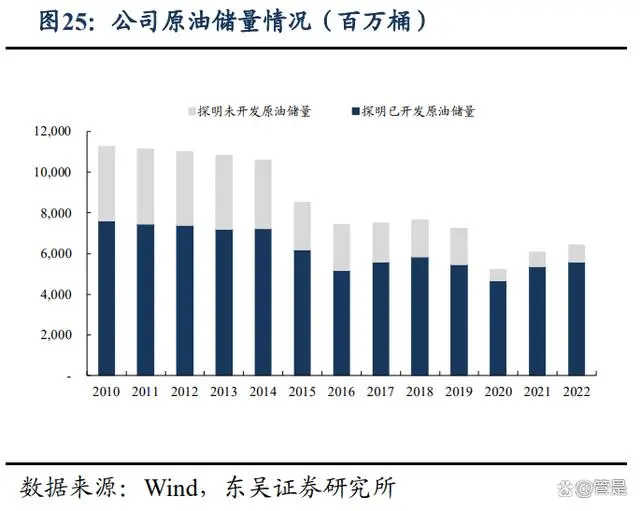

公司油藏开发充分,天然气储量平稳。原油方面,其一,经济可采储量跟随油价 调整,油价下跌导致公司经济开采储量下降;其二,随着稳定持续的原油生产,已探 明可采储量不断消耗,两方原因导致公司剩余原油可采储量在 2014 年后出现大幅下降, 从 2014 年的 105.9 亿桶跌至 2022 年的 64.2 亿桶。天然气方面,2014 至 2016 年公司稳 油增气的总体战略推动了天然气的增储上产,2016 年至今,剩余天然气可采储量平稳 中略有下降,2022 年为 73.5 万亿立方英尺。 横向对比来看,中石油剩余油气可采储量在“三桶油”公司中的占比最大,但由 于我国陆上油气田开采年限较长,衰减问题更为明显,近年来中石油在“三桶油”中 的储量占比持续下降,2022 年以 186.6 亿桶油当量的储量水平占比 67.5%。

中石油的储采比在“三桶油”中位居首位,2020-2022 年公司储采比相对稳定, 2022 年公司的油气可采年限为 11 年。由于陆上油气田开采时间较长,近五年公司储量 接替率不及另外“两桶油”。

2、保障国家能源安全,增储上产进行时

推动能源革命需要保持原油、天然气产能稳定增长。能源是国民经济的重要物质 基础,影响国家宏观经济的发展,掌控着国家未来命运。随着能源革命的愈演愈烈, 加快推进我国能源结构的战略性调整迫在眉睫。夯实国内能源生产基础、保障基础民 生是能源革命的前提条件。在“双碳”目标的大背景下,石油与天然气作为除煤炭之 外最重要的一次能源,保持原油、天然气产能稳定增长,是国家能源结构调整的重要 基础举措。

我国原油需求量持续增长,对外依存度逐渐攀升。从 2003 年起,中国成为世界第 二大石油消费国和最大原油进口国。2017 年,中国超越美国成为世界第一大原油净进 口国。实际上,我国的油气资源较为丰富。根据 2022 年中国矿产资源报告,我国已探 明石油储量达到近 37 亿吨;在第三次石油资源评估中,我国海上石油总储量可达近 250 亿吨。尽管我国石油资源较为丰富,但囿于地理条件与开采难度,我国原油开采投 资成本较高,因此开采量始终维持在中等水平。

近十年,我国原油产量增长缓慢,自 2015 年达到阶段性峰值2.15亿吨,随后开始下降态势。另一方面,国内原油需求量在 近十年一直稳定增长,2021年达到7.18亿吨,同比增长 6.33%。在开采问题与高强度 消费的双重夹击下,中国石油资源对外依存度逐渐攀升、居高不下,2022年我国原油产量为2.04亿吨,净进口量达到5.20亿吨,进口依赖度高达72%。

天然气需求将大幅增加,我国产量仍有待提升。天然气是一种洁净环保的优质能 源,随着我国能源结构转型步伐的加快,市场对天然气资源勘探开发和生产供应能力 提出了更高的要求。尽管我国天然气勘探开发取得了显著成绩,生产供应能力逐步提 升,近十年天然气产量的复合增长率达到 7.23%,但仍然供不应求。近十一年来,我国 天然气需求大幅增加,2010 年我国天然气需求量为 1089 亿立方米,到 2021 年,我国 天然气消费量达到 3787 亿立方米,增长超过两倍,复合增长率高达 12 %。因此我国天 然气的对外依存度也在逐渐增长。2021 年我国天然气产量为 2092 亿立方米,净进口量 为 1695 亿立方米,进口依赖度为 45%。随着环保政策趋严,煤改气工程进程加快,中 国未来天然气需求将持续大幅增加,其对外依存度或将超过 50%。

政策层面促进、支持和推动油气产量快速增长。我国日益增长的能源需求与实际 供给情况出现了矛盾,制约着我国未来的可持续发展,降低石油、天然气的对外依存 度迫在眉睫。2021 年 3 月,十四五规划中明确要求油气勘探开发被列入国家科技攻关 的核心技术;强调夯实国内产量基础,保持原油和天然气稳产增产,做好煤制油气战 略基地规划布局和管控。2022 年 2 月,国家发展改革委、国家能源局发布“关于完善能源绿色低碳转型体制机制和政策措施的意见”,再次强调完善油气清洁高效利用机制、 提升油气田清洁高效开采能力。未来,随着石油、天然气资源勘探开发力度不断加大, 政策层面促进、支持和推动石油、天然气产量快速增长,特别是清洁能源天然气将迎 来高速增长的突破期。

3、油价或持续稳定在高位运行

供给侧:全球上游资本开支增幅有限,原油主产国供给弹性下降

2015-2021年全球原油上游投资不足导致当下原油供应紧张,2022年油价高位并未 带动上游资本开支积极性。2020 年,新冠疫情冲击国际油价,全球上游资本支出较 2019 年收缩 1490 亿美元,同比减少 31%。2021 年,全球经济复苏叠加 OPEC+联盟减 产,Brent 油价均值达到 70.94 美元/桶,相比 2020 年涨幅为 64%,但全球上游计划资本 开支较 2020年增加 250亿美元,仅同比上涨 7.7%,但是仍明显低于 2019年水平。2022 年初,国际油价一路上涨至 90 美元/桶以上,但全球油气公司年初制定的 2022 年上游 计划开支仅比 2021 年实际资本开支增长 330 亿美元,同比增速仅 8.6%,并且仍明显低 于 2019 年水平。

受新旧能源转型影响,未来传统油气投资意愿不足。我们认为,在新旧能源结构 转型过程中,2027 年左右原油需求或将达峰,如果现在加大力度投资,传统油田开发 生产周期需 3-5 年,投产后需求反而下降,传统原油项目长期回报率存在不确定性。面 对这一问题,欧洲系公司(如壳牌)向综合能源服务商转型,油气产量下降;美国系 公司(如雪佛龙、康菲石油、西方石油)以传统能源为主业,但油气产量也仅维持平 稳,大幅增产意愿不强。当前俄罗斯原油产量下降有限。2022 年 4 月,俄乌冲突影响显现,俄罗斯原油产 量环比下降 90 万桶/天至 910 万桶/天。但从 2022 年 5 月以来,随着俄罗斯原油出口贸 易向印度和中国转移,俄罗斯原油产量逐步回升,截至 2023 年 2 月,原油产量已恢复 至 991 万桶/天,比俄乌冲突前(指 2022 年 1-2 月,下同)下降 17 万桶/日,下降幅度 有限。

截至 2023年 2月,受欧盟禁运俄罗斯成品油、G7对俄罗斯成品油限价政策影响, 俄罗斯石油出口下降。2023 年 2 月,俄罗斯石油出口总量为 750 万桶/天,较冲突前水 平减少 60 万桶/天,较 2023 年 1 月减少 50万桶/天,其中,原油出口量为 490万桶/天, 较冲突前减少 10 万桶/天,环比减少 20 万桶/天,成品油出口量为 260 万桶/天,较冲突 前减少 50 万桶/天,环比减少 30 万桶/天。 资本开支不足,俄罗斯原油产量已达产能瓶颈。根据国际能源信息署 IEA,俄罗 斯原油产能已从 2021 年 10 月的 1042 万桶/天下降至 2023 年的 1020 万桶/天,俄罗斯原 油产能已经出现了衰减的问题。2023 年 3 月,俄罗斯计划减产 50 万桶/天,或造成供给 进一步收缩。

截至 2022 年 10 月,OPEC+实际增产情况仍未达到计划目标。一方面,沙特、阿 联酋等有增产能力的国家维持谨慎增产,另一方面,其他 OPEC+国已达生产瓶颈,无 力增产。2022 年 10 月部长级会议上,OPEC+决定在 2022 年 8 月产量目标基准上继续 减产 200 万桶/天,减产区间为 2022 年 11 月至 2023 年 12 月。本轮减产开始至 2023 年 2 月,OPEC+实际产量稳定在 4000 万桶/天以下,减产执行情况良好。自 2023 年 5 月 起至 2023年年底,沙特以及其他 OPEC和多个非 OPEC成员国自愿削减石油产量,减 产规模超 160 万桶/天。

本轮减产面临增产能力不足的客观约束。一方面,OPEC+减产负担国能够较好执 行减产计划。另一方面,未达产量目标的国家受产能不足影响难以实现大幅增产。因 此我们对本轮减产计划执行情况的预期较为乐观。 在 OPEC+部分国家产量达到极限、全球原油供给紧张未有效缓解的情况下,仅沙 特和阿联酋拥有剩余产能,截至 2023 年 2 月两国剩余产能分别为 175、89 万桶/天,我 们认为沙特内部协调能力和油价调控能力进一步增强,其维持油价高位的意愿非常强 烈,其控制产量托底油价的措施或将有更大成效。

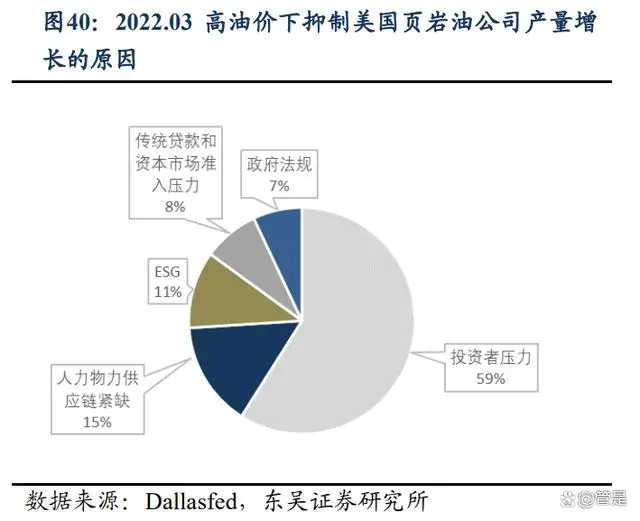

疫情后美国原油供给恢复缓慢。其一,在投资者愈加严格的资本约束下,美国主 要页岩油气公司选择将更多的收益返还给股东,而非扩大投资;其二,前期疫情冲击 下,页岩油公司利用库存井维持生产,疫后油气公司需要更高的成本加快打新井,弥 补过去优质油井的消耗,来实现增产。其三,人力物力短缺及成本上升成为美国页岩 油公司进行油气生产时所面临的主要问题,使得公司油气开采周期拉长,增产速度放 缓。 根据美国能源信息署 EIA,预计 2023年美国原油增产 56万桶/天至 1244万桶/天, 美国原油逐步恢复增产,但是产量增幅有限,年均增产不及疫情前 150 万桶/天的水平。

2、需求侧:原油需求达峰尚需时日

交通用汽柴油占据了全球油品消费的半壁江山,主要考虑新能源汽车替代效应的 影响。 考虑传统能源价格高涨推动新能源汽车渗透加速,我们采用新能源车渗透率按照 S 型上升的情景假设。 根据我们搭建的模型,我们预测到 2025 年,全球交通领域汽柴油消费量达峰,对 应 2025 年全球新能源汽车销售渗透为 24%。 随后由于新能源汽车的快速渗透,全球新能源汽车保有量持续加速增长,全球交 通用汽柴油需求量加速下降,到 2040 年全球新能源汽车销售渗透将达到 100%。

基于全球交通用汽柴油需求量将在 2025 年达峰的预测结论,以及我们对航空煤油、 工业用油、化工用油和其他用油的假设和模型,我们预计全球原油总需求量将在 2027 年左右达峰,2027年需求达峰量与 2022年需求总量之间还存在约 400万桶/天的增长空 间。 2027-2040 年,新能源汽车的快速替代导致交通用汽柴油逐年大幅下降,原油总需 求加速下降,2040-2060 年,市场不再销售传统燃油车,交通用汽柴油年消耗量随着传 统能源保有车辆的报废而逐年缓慢下降,原油需求下降速度随之放缓。 预计 2022-2023 年全球原油需求增量在 150-200 万桶/天,2024-2026 年全球原油需 求增量约为 100 万桶/天, 2027 年全球原油需求实现达峰。中长期来看,全球原油需求 仍保持增长趋势,达峰时刻尚未来临。

从长期需求结构来看,交通用汽柴油消费量占比将逐年递减,化工用油占比将逐 年提升,化工用油成为未来原油需求的主要增量来源。预计 2023 年油价仍然高位运行。供给端,紧张。能源结构转型背景下,国际石油 公司依旧保持谨慎克制的生产节奏,资本开支有限,增产意愿不足;受制裁影响,俄 罗斯原油增产能力不足且会一定程度下降;OPEC+供给弹性下降,减产托底油价意愿 强烈,沙特控价能力增强;美国原油增产有限,长期存在生产瓶颈,且从 2022 年释放 战略原油库存转而进入 2023 年补库周期。

需求端,增长。今年上半年国内经济恢复但 海外经济衰退,下半年国内外经济都进一步恢复,需求端呈现前低后高的格局。综合 国内外来看,全球原油需求仍保持增长态势。另外,我们认为,2023 年即便发生经济 衰退,但由于美联储为了复苏经济将加息趋缓甚至采取降息措施、沙特主导的 OPEC+ 通过控制产量支撑油价、非 OPEC 无法大规模增产,油价出现大幅暴跌可能性较小。 在没有突发大型冲击事件的情况下,油价或将持续且较为稳定的处于高位运行。中石 油的油气和新能源板块业绩或将继续维持稳定且良好的业绩。

4、新能源业务全面提速

公司新能源业务加速发展。2022年,中石油新能源投资 76.7亿元,同比增长252%, 重点项目建设加快推进,生产用能清洁替代和对外清洁供能市场开拓成效明显。积极 获取清洁电力并网指标,大力发展风力、光伏发电、地热供暖以及碳捕集、利用和封 存(“CCUS”)业务,首个风光储一体化开发项目——大庆油田葡二联小型分布式电源 集群应用示范一期工程并网发电,累计建成风光发电装机规模超过140万千瓦,累计地 热供暖面积达到 2,500 万平方米,新能源开发利用能力达到 800 万吨标煤/年。公司目标到 2025 年实现新能源产能比重达到一次能源生产的 7%,力争到 2035 年 外供绿色零碳能源超过自身消耗的化石能源,基本实现热、电、氢对油气业务的战略 替代,力争 2050 年实现“近零”排放,新能源业务产能占据半壁江山。

三、炼化和新材料:政策趋严+行业好转,板块业绩有望迎来改善

1、炼化项目审批趋严,中石油更显存量优势

2021 年 9 月以来,中共中央、国务院发布《关于完整准确全面贯彻新发展理念做 好碳达峰碳中和工作的意见》,国务院发布《关于印发2030年前碳达峰行动方案的通知 (国发〔2021〕23 号)》,国家发展改革委发布《关于严格能效约束推动重点领域节能 降碳的若干意见》和《石化化工重点行业严格能效约束推动节能降碳行动方案(2021- 2025 年)》,推动石化行业碳达峰,严控新增炼油能力,到 2025 年国内一次加工能力控 制在 10 亿吨以内,主要产品产能利用率提升至 80%以上。2021 年 12 月,中央经济会 议指出新增可再生能源和原料用能不纳入能源消费总量控制。我们认为,在供给侧发 展受限的环境下,后续大幅新增炼化产能有限。

2023 年及以后仅有不到 1 亿吨/年的大炼化产能在建或规划中。中国石油旗下广东 石化 2000 万吨/年炼化一体化项目在 2023 年 2 月实现全面投产,山东裕龙岛一期 2000 万吨/年项目和镇海炼化 1100 万吨/年项目有望于 2023 年建设完成。

另一方面,根据石油和化学工业规划院给出的“十四五”石油化工行业规划指南, 十四五期间,中国将持续推动炼油企业“降油增化”,新增炼化项目成品油收率较低。 “十四五”石油化工行业规划的重点在于淘汰小产能,整合炼油指标,建设流程更长、 开工率更高、产品更加多样化的炼化一体化项目,提升我国石油化工生产的效率,减 少生产环节对油品的浪费,做到对资源“吃干榨尽”。 随着国家政策方向的发展和实际运营过程中不断发掘出来的下游化工品的精细化 和差异化的价值,在双碳大背景下,向下游化工材料延伸、走小油头大化工路径的炼 厂成为未来发展趋势。

从中国“降油增化”政策导向和大炼化项目成品油收率角度来看,虽然未来几年 中国的炼油能力增加,但成品油收率不高,对成品油供给贡献力度有限。在此情况下, 中石油炼油板块或将尤其受益于即将迎来的成品油供给端收缩。目前,公司仍然有多 个重点炼化项目在投建,炼化板块未来依然可期。

2、炼油化工与新材料业务基本情况

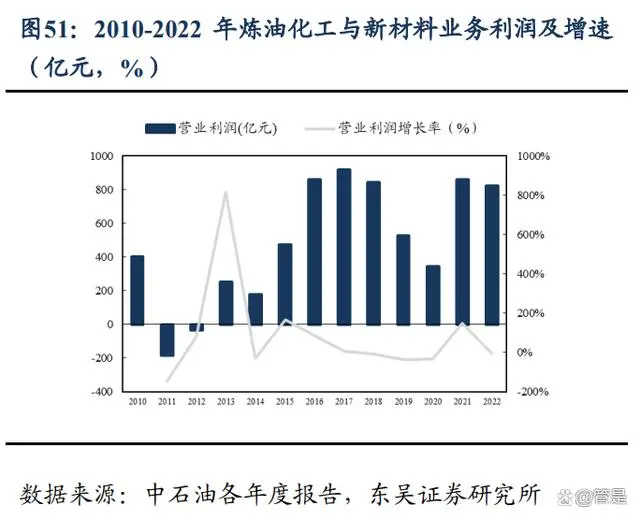

公司炼化产能居全国第二。中石油不断提升炼化装置平稳运行水平,全年装置运 行平稳率达到 99.7%。截至 2021 年底,公司国内共拥有大型炼化一体化企业 8 个,千 万吨规模炼厂 13 个。炼油毛利率与原油价格负相关。2022 年,俄乌冲突催化作用下,国际原油价格高 企,原油价格上涨导致炼油原料采购成本上升,进而导致炼油毛利率环比下降 1.8pct至 7.1%。2022 年公司炼油与化工营业收入达 11579.18 亿元,同比增长 36%;营业利润 822.12 亿元。同比减少 5%。得益于公司不断地拓展和升级炼化项目,提升效率,2021- 2022 年炼油与化工板块利润以逼近 2016-2018 年低油价时期的水平。2023 年,经济复 苏伴随出行需求提升,公司成品油板块业绩有望改善。

炼油业务基本情况

炼油结构按需调整,降油增化正在进行时。公司炼油产品主要包括汽油、柴油、 煤油。公司的成品油收率在 2010-2019年整体呈上升趋势,2020年后公司持续推进转型 升级,降油增化,到 2022 年公司成品油收率为 64.2%,降至近 10 年低点。根据市场需 求,近 10 年公司柴汽比持续下降,从 2010 年的 2.31 下降至 2021 年的 0.98,2022 年, 国内出行受疫情影响,汽油需求出现下滑,柴油稍好,公司及时上调柴汽比至 1.23。 此外,公司也将推进区域资源优化配置,充分发挥特色原油资源与炼厂装置优势, 优化生产路线及产品方案,加大低硫船用燃料油、石蜡、润滑油、沥青等特色产品生 产力度。

化工业务基本情况

公司化工板块主要有五大类产品,分别是乙烯、合成树脂、合成纤维原料及聚合 物、合成橡胶、尿素。公司坚持“减油增化”“减油增特”,持续优化产品结构;成立 日本新材料研究院,加大化工新材料研发力度,努力提升高端专用料和高附加值产品 比例,新材料产量大幅增加。近 5 年,公司化工品产量不断提升,2022 年公司化工品 产量合计为 2373 万吨,同比增长 6.8%。

3、炼油:消费税监管趋严,利好国营炼油龙头

原油价格稳定高位,价差有望达到近期最高

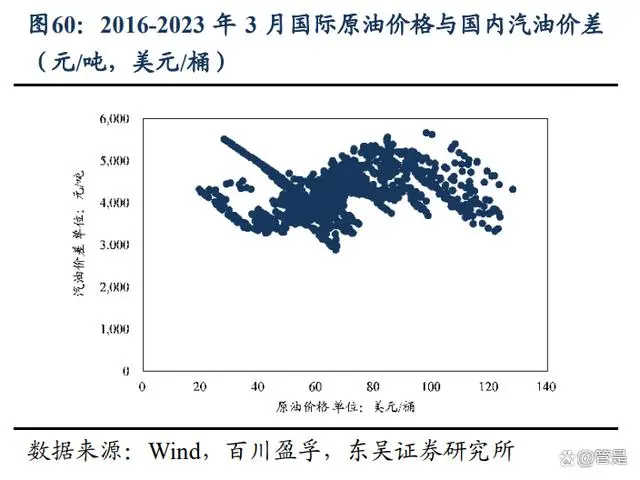

2016 年 1 月,发改委发布《石油价格管理办法》,其中第六条较为明确地规范了国 内成品油市场的定价问题,即“当国际市场原油价格低于每桶 40 美元(含)时,按原 油价格每桶 40 美元、正常加工利润率计算成品油价格。高于每桶 40 美元低于 80 美元 (含)时,按正常加工利润率计算成品油价格。高于每桶 80 美元时,开始扣减加工利 润率,直至按加工零利润计算成品油价格。高于每桶130美元(含)时,按照兼顾生产 者、消费者利益,保持国民经济平稳运行的原则,采取适当财税政策保证成品油生产 和供应,汽、柴油价格原则上不提或少提。”

根据 2016 年 1 月以来的国际油价和国内汽油、柴油零售价的散点图,可以发现这 种规则在实际使用中具有明确的指导意义。当国际原油价格高于 80 美元/桶时,国内汽、 柴油价格基本不再变动,由企业承担成本变动带来的利润削减。当国际原油价格处于 80 美元/桶时,国内汽、柴油与原油价差分别达到阶段性高点。我们认为,在没有突发大型冲击事件的情况下,油价或将持续且较为稳定的处于 高位运行,中枢略低于 2022 年,考虑沙特财政平衡油价,油价底部将处于 70-80 美元/ 桶。因此,我们看好炼油板块未来的业绩好转。

国内成品油分项需求回暖,助力炼化业务利润抬升

2022Q4,受国内疫情感染高峰影响,经济处于低谷期。利用 PMI 辅助分析,2022 年 11 月份 PMI 指数为 48.0%,同比下降 2.1pct,环比下降 1.2pct;2022 年 12 月 PMI 指 数为 47%,同比下降 3.3pct,环比下降 1.0pct。 2023Q1,PMI 水平达近年最高,疫后经济复苏趋势显著。2023 年 2 月份 PMI指数 为 52.6%,同比上升 2.4pct,环比上升 2.5pct,达到 2018 年以来最高值。2023 年 3 月 PMI 指数为 51.9%,同比提升 2.4pct,环比下降 0.7pct,产需两端扩张有所放缓。整体 来看,2023 年有望迎来疫后经济快速复苏,驶上了近年少有的快速路。

汽油:城市交通状况良好,印证汽油需求长期持续稳定。汽油需求不再受疫情制约,需求迅速回暖。2022Q4 汽油消费受阻,2023 年正迅速 回暖。受国内 2022 年四季度疫情和上游原油价格高位影响,汽油需求受到了较强的抑 制作用,2022Q4 国内汽油产量 3561.3 万吨,相比于 2021 年 Q4 的 4017.9 万吨有所降 低,但是相比于 2020 年 Q4 的 3535.3 万吨有所提升。 2023 年年初城市交通机动车数量相比于往年同期有较大的增长。2023 年 2 月北京 市拥堵指数达 172,同比增长 92.96%;上海市拥堵指数达 146,同比增长 73.83%;广 州市拥堵指数达 167,同比增长 96.97%;深圳市拥堵指数达 164,同比增长 115.29%。 其余主要城市拥堵指数相比往年也均呈现增长趋势。

柴油:基建复苏信号明显,助力柴油需求上升。2022Q4 柴油产量相比于 2021Q4 均有大幅增长,增长态势良好。这种强势增长有 望延续到 2023 年。 2023 年春节后基建复苏信号明显,预计将助力柴油需求迅速上升。根据百年建筑 网的统计,2023 年正月初十开复工率 10.5%、劳动到位率 14.69%,低于 2021 与 2022 年同期水平。但随后迅速上升,正月廿四的开复工率达到 76.5%、劳动到位率达到 68.20%,与 2021 年同期水平几乎无异。到了二月初二开复工率达到了 86.1%、劳务到 位率达到了 83.9%,虽然 2023 年开复工率和劳务到位率尚未完全恢复到 2021 年水平, 但相比于 2022 年已经有了显著提高。这预示着基础建设需求将会迅速抬升,2023 年柴 油需求将迎来上涨。

航空煤油:消费稳步攀升,预计需求将有大幅增长。煤油产量于 2022 年底逐渐攀升。2022 年底,随着防控政策放开,我国煤油产量超 过 2021 年同期水平,但尚未恢复到 2020 年年底水平。 航线运输量上升带动航空煤油需求增加。国内运输周转总量从 2022年 10月的 42.6 亿吨公里增加至 2023 年 1 月的 73.9 亿吨公里,运输旅客人数也从去年 10 月的 1592.4 万人提升至 2023 年 1 月的 3977.5 万人。 航空燃油预期需求情况持续向好。从未来 12 周国内始发的航班情况来看,预计航 空燃油消耗数从 2023 年 2 月 28 日的 8.42 万吨上/天涨到 5 月 16 日的 13 万吨/天,涨幅 54.39%,其中国内航线航空燃油消耗数将从 7.86 万吨/天涨至 12 万吨/天;预计航班量 将从 2 月 28 日的 1.30 万班/天上升到 5 月 16 日的 2.02 万班/天,其中国内航线将从 1.28 万班/天上升到 5 月 16 日的 1.97 万班/天。

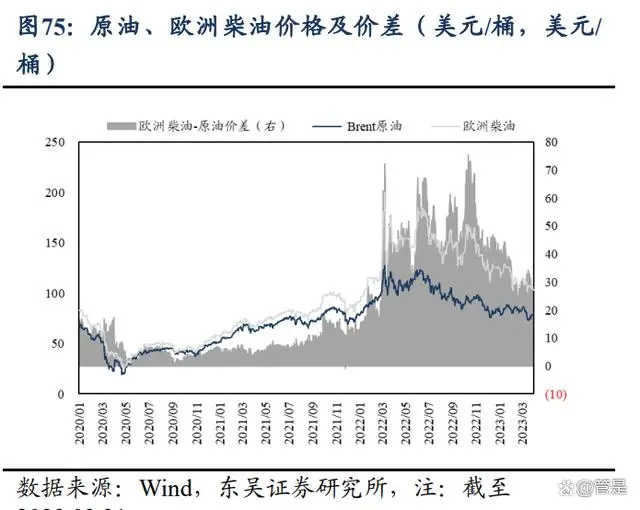

海外成品油价差扩大+出口配额增加,盈利空间有望释放

受 2020 年疫情冲击下海外炼厂关停潮以及 2022 年初俄乌冲突战争影响,当前海 外成品油价差仍处高位。自 2022 年 3 月以来,海外成品油价格大幅扩张,价差不断突 破历史新高。2022年 6-7月份以来,美联储持续加息下,市场信心薄弱推动油价重心下 行,海外成品油价差一定程度上收缩,但仍在高位震荡。截止至 2023 年 03 月 31 日当 周,美国柴油、汽油、航煤周均价分别为 113.86、112.33、114.49 美元/桶;与原油差价 分别为 35.24、33.71、35.87 美元/桶。欧洲柴油、汽油、航煤周均价分别为 104.68、 119.25、108.21 美元/桶;与原油差价分别为 26.07、40.63、29.59 美元/桶。新加坡柴油、 汽油、航煤周均价分别为 99.69、94.67、94.61 美元/桶;与原油差价分别为 21.13、 16.05、16.04 美元/桶。

西方制裁下,俄罗斯成品油贸易转移较为费力。2023 年 2 月 3 日,欧盟成员国、 七国集团(G7)和澳洲表示,已就俄罗斯石油产品的价格上限敲定协议。其中,对石 油产品价格上限涉及 2 个价格等级,俄罗斯石油产品(例如柴油)设定 100 美元/桶的 最高限价,燃料油等俄罗斯低质量产品的最高限价达成协议,设定为 45 美元/桶。2023 年 2 月 5 日,俄罗斯石油产品海运价格上限措施开始执行。同时,2023 年 2 月 5 日,欧 盟全面禁止海运进口俄罗斯成品油。

自 2022 年下半年起,欧洲买家希望在 2023 年 2 月俄罗斯成品油禁运前重建柴油库 存,欧盟柴油进口量大幅提升,同时从俄罗斯进口柴油占比不断下降,2023 年 1 月, 俄罗斯对欧盟的油品出口量已经环比大幅下降了 50 万桶/天,欧盟进口的俄罗斯柴油占 比已 2022 年 7 月的 62%降至 41%,俄罗斯与欧盟之间的柴油贸易量还有 70 万桶/天。

自欧盟从 2023 年 2 月 5 日开始对海运俄罗斯石油产品实施新的价格上限后,航运 数据显示,2023年 2月俄罗斯海运成品油日均出口量为 213万桶,较 2023年 1月约 270 万桶/日的近期高位下降了 21%,比俄乌战前平均水平低 24%,且降至 2022 年 5 月以来的最低水平,主要原因为非洲的新买家未能吸收从欧洲转移的俄罗斯成品油,导致俄 罗斯成品油出口大幅下滑。 我们认为,相比于原油贸易,俄罗斯较难将成品油贸易转向亚洲市场,原因是中 国和印度为成品油净出口国,较难承接大量的俄罗斯成品油输入。未来俄罗斯油品出 口下降或将进一步倒逼其国内炼能下降,导致全球炼油供给出现收缩,推动以柴油为 代表的成品油价差水平上移。

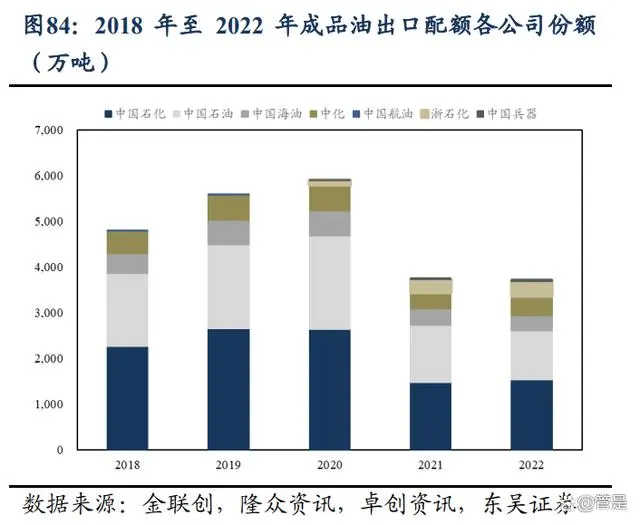

成品油出口配额放宽,助力出口油企增收创效。2023 年第一批成品油出口配额共 计下发 1899 万吨,同比上涨 46%,各油企出口配额相比去年同期也有不同程度的增长, 中国石化和中国石油出口配额最高,分别为 741 和 596 万吨,同比分别增长 71.93%和 41.57%。两者合计占据了全部成品油出口配额的 70.41%。首批配额已落地,相较十四 五开端出口政策收紧时期,成品油出口配额趋向放松,提振油企出口心态,助力企业 缓解库存压力、增收创效。

中石油出口配额占比第二,海外市场前景广阔。2018-2022 年,中国石油成品油出 口配额占比始终保持在仅次于中国石化的第二位,分别为 33.06%、32.83%、34.69%、 33.58%、28.75%。2023 年第一批成品油出口配额已落地,中国石油延续高点,占比为 31.38%。目前,海外成品油价差仍维持高盈利水平,配合成品油出口政策放宽迹象, 中石油海外业务前景广阔,盈利空间有望进一步释放。

成品油消费税逐渐规范化,国营炼化竞争优势增强

油品出厂方面: 由于石油在我国属于稀缺性资源,并且汽柴油在燃烧过程中会对环境产生一定的 影响,因此我国自 1994 年以来就在生产环节(即炼厂)对汽油和柴油按量征收消费税, 以督促最终消费者(汽车、卡车等)节约用油。至今我国成品油消费税已历经4次大幅 上调,汽油消费税从 0.2 元/升(约 278 元/吨)增至 1.52 元/升(约 2110 元/吨),柴油消 费税从 0.1 元/升(约 118 元/吨)增至 1.2 元/升(约 1411 元/吨)。

由于成品油消费税是在炼厂环节征收,若炼厂按照成品油的实际生产量缴纳消费 税,则成品油出厂价势必较高,在面对下游成品油批发商及终端零售加油站时没有价 格上的竞争优势。考虑到成品油的产品属性较难判断(似油非油),因此一直以来部分 炼厂(尤其是地方炼厂)通过“变名销售(把成品油当做化工品来卖)”的方式避免缴 纳成品油消费税,从而获得更高的盈利。但是,炼厂这种偷税漏税的行为一方面没有 尽到诚信缴税的义务,另一方面也破坏了成品油市场的正常运行。

因此,国家税务总局发布了 2012 年第 47 号文和 2013 年第 50 号文严格定义了成品 油消费税的征收范围,以对炼厂的变名销售行为进行针对性堵漏: 一、纳税人以原油或其他原料生产加工的在常温常压下呈液态状的产品(长得像 油的产品)对外销售按以下规则征收消费税: 1、符合汽油、柴油、石脑油、溶剂油、航空煤油、润滑油和燃料油这 7 大油种标 准的产品,按照相应的规定征收增值税; 2、规定 1 以外的符合国家标准或石油化工行业标准,且事先将省级以上(含)质 量技术监督部门(仅对送检样品负责)出具的相关产品质量检验证明报主管税务机关 进行备案的产品,不征收消费税; 3、规定 1 和 2 以外的产品,视同石脑油征收消费税。

二、纳税人以原油或其他原料生产加工产品如以沥青产品(长得像沥青的产品) 对外销售按以下规则征收消费税: 1、符合沥青产品的国家标准或石油化工行业标准,且事先将省级以上(含)质量 技术监督部门(仅对送检样品负责)出具的相关产品质量检验证明报主管税务机关进 行备案,不征收消费税; 2、规定 1 以外的产品,视同燃料油征收消费税。 由于消费税完税信息传递不畅通、成品油和其他石油化工产品难以区分、对炼化 企业的生产行为缺乏有效监管和省级政府及其税务机关对消费税征收不严格不积极等 原因,国家税务总局 2012年第 47 号文执行多年但是堵漏效果不明显,以地炼为代表的 炼厂仍然在变名销售不缴纳消费税。

为进一步解决炼厂少交成品油消费税的问题,国家税务总局发布了 2018 年第 1 号 文:自 2018 年 3 月 1 日起,所有成品油发票均须通过增值税发票管理新系统中的成品 油发票开具模块开具,通过该模块可开具成品油增值税专用发票、普通发票和电子普 通发票,并且必须在发票左上角打印“成品油”字样,目前对加油站开具的卷式增值 税普通发票暂无此要求。

4、化工:乙烯仍有进口替代空间,化工板块有望迎改善

中石油作为全国第二的乙烯生产企业,2022 年产能占比 12%左右。2022 年,公司 加快进行广东石化、吉林石化、广西石化乙烯项目建设,继续推进塔里木乙烯二期项 目以及抚顺、兰州乙烯改造项目工作。2022 年 11 月,中国石油吉林石化公司 120 万吨/ 年乙烯装置建设项目正式开工。2023 年 2 月,广东石化炼化一体化项目全面投产,120 万吨/年乙烯装置产出合格产品。2023 年 3 月,广西石化炼化一体化转型升级项目已完 成第一批次主项的基础设计审查工作。

随着中国经济的快速发展,人民生活水平得到了很大的提升,中国乙烯市场也正 蓬勃发展。2019 年至今,随着民营炼化一体化项目的集中投产,我国进入新一轮扩产 周期,2021 年国内乙烯产能 4191 万吨,产量 3817 万吨,开工率 91.10%,近 5 年开工 率一直维持在 90%以上的水平。然而目前国内供给仍无法满足乙烯需求,2021 年国内 乙烯消费当量达 6296 万吨(含乙烯下游衍生物折当量净进口),2021 年进口依赖度接近 40%,供需缺口为 2479 万吨/年,乙烯未来仍有较大进口替代空间。

乙烯生产工艺路线走向多元化。2021 年,我国乙烯生产路线主要以石脑油裂解为 主,约占 73%,CTO/MTO 工艺占比约 21%,其他生产路线占比 6.6%。乙烷裂解制乙 烯(含混合烷烃裂解)、重油催化热裂解制烯烃、原油直接裂解制烯烃、乙醇脱水制乙 烯等技术均已实现工业化,乙烯原料呈现出轻质化、多元化、一体化发展趋势。

中国石化和中国石油占领导地位。2015 年中国放开地方炼油企业进口原油使用权 并下放省级石化项目审批权限后,以及外资准入要求放宽,以四大民营炼化一体化项 目为代表的聚酯企业开始向产业链上游延伸投资,外资石化公司大举进入中国市场, 中国石化、中国石油、中国海油和中化集团等国有石化企业在此期间也大规模进行扩 张,乙烯市场参与主体愈加多元化。2022 年,中国石化及其合资公司的总产能为 1364.5 万吨/年,市场份额超过 30%;其次是中国石油,总产能为 531 万吨/年,市场份 额为 12%;中国海油的总产能为 220 万吨/年,占比 5%;产能在 100 万吨/年及以上的 生产企业的合计产能为 1120 万吨/年,占比 25%;小于 100 万吨/年的生产企业占比 3%。

四、销售:油品业务盈利回升,非油业务加快发展

1、销售业务总体情况

公司销售板块收入疫后迅速回升。2020 年,受全球新冠疫情的影响,公司大部分 油气产品销售量减少、价格也大幅下降,导致销售业务营收大幅缩减近 1/3。随着疫情 影响的减弱,国内成品油市场需求逐步恢复,公司大力加强精细营销,积极开发零售 和终端客户,同时积极统筹国内国际市场,合理安排成品油批发和出口,2021 年销售 业务营收迅速恢复到疫前水平,达到 2.14 万亿元,同比增长 45.4%。2022 年,受油价 高企影响,公司成品油销售价格提升,销售业务营收继续保持高增长,达到 2.74 万亿 元,同比增长 27.96%。公司销售业务板块毛利和经营利润显著上升。近年来,公司加强优化成品油配置 和流向,努力控制营销成本。2022年,公司销售业务板块毛利为 1014.68 亿元,同比增 长 52.73%,毛利率为 3.70%,经营利润为 143.74 亿元,同比上涨 8.26%。

疫后成品油需求有望回暖,成品油总经销量仍具备上升潜力。近几年由于市场竞 争激烈以及疫情的影响,成品油市场需求收缩,公司成品油销售受到一定阻碍,2022 年成品油总销量为 1.51 亿吨,同比下降 7.75%,其中汽油、柴油和煤油销量均有一定 程度下降。2023 年初,疫情消退,经济复苏,国内出行量和基建全面逐渐回暖,成品 油总销量有望回升。

加油站规模优势显著。十几年来,公司加油站数量持续增长,至 2022 年达到 22586座,国内排第二位,仅次于中石化,加油站规模优势显著。2020年后,受疫情冲 击影响,公司单站加油量一直呈现下降趋势,2021 年下降到 8.05 吨/日,同比下降 5.07%,2022 年下降到 7.79 吨/日,同比下降 3.23%,下降趋势变缓。公司加油站属于 自营性质,由于新建自营加油站的资金壁垒、时间成本极高,民营和外企炼化难以在 短时间内获得与中石化同等数量的能够施加完全影响力的自营加油站,中石油加油站 的规模优势将长期存在。

2、非油业务加快发展步伐

昆仑好客作为中国石油旗下非油业务品牌,其便利店于 2007 年开始规模发展。中 国石油非油业务加快市场化、专业化发展步伐,以加油站为平台,做大做精便利店业 务,做实做强汽服及集采、自有商品业务,加快推进加油站快餐、生鲜等业务,探索 广告、金融、保险、专卖、车辅产品、便民服务等跨界经营,通过融合、共享、跨界, 为消费者提供“一站式”的服务,着力构建“人·车·生活”生态圈。目前,昆仑好 客便利店遍布全国 31 个省区市,总量超过 2 万座,日服务进站客户达千万人次,成为 展示中国石油良好形象的重要窗口。

积极布局新能源站点,坚持油气与新能源融合发展。公司积极响应碳达峰、碳中 和战略目标,灵活运用合资合作、特许经营、延期租赁等轻资产方式开发加油加气站, 控制常规站特别是区外高价站开发,加快光伏站、充换电站、加氢站(综合能源服务 站)等新能源站点布局。2021年2月7日,公司合资建设的太子城服务区加氢站正式 投入使用,为冬奥崇礼赛区 50 辆氢能源大巴供应氢燃料加出中国石油加氢业务“第一枪”。同时公司坚持油气与新能源融合发展,扎实推进风光发电、地热、碳捕获、利 用与封存(CCUS)等新能源业务。

五、天然气销售:政策发力+国际气价回落,板块业绩有望改善

1、天然气产销业务情况

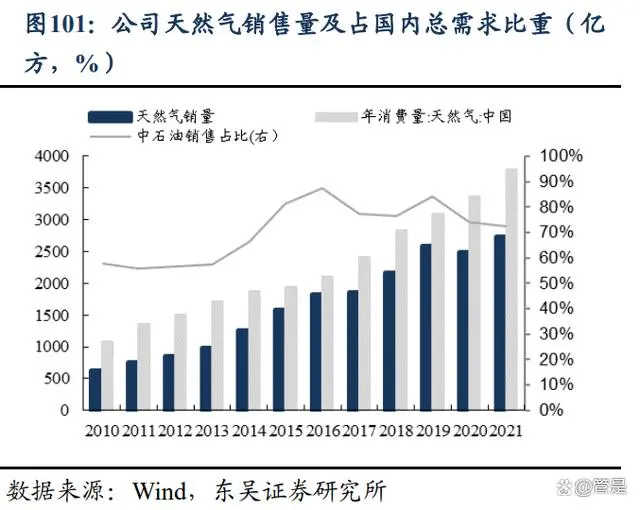

公司为我国最主要的天然气供应商。2022 年,公司销售天然气 2602.8 亿方,国内 天然气总需求为 3786.94 亿方,公司销售的天然气占国内总需求的 70.35%。在公司销 售的天然气中,外购气和自产气各占约 50%。

自产气: 中石油天然气探明储量位列国内第一,贡献我国超 60%的天然气产量。公司拥有 全国最大的天然气探明储量,约为中石化、中海油探明储量的 8 倍。2022 年,公司天 然气探明储量为 734530 亿立方英尺(20799 亿方),其中探明已开发储量、探明未开发 储量占比分别 57%、43%,尚有较大的开采潜力。在天然气产量贡献方面,中石油是 国内天然气产量贡献最大的公司,2022 年天然气产量占国内天然气产量的 61%,远高 于其余天然气企业。中石油在我国天然气领域拥有不可撼动的龙头地位,是保障我国 天然气能源安全的排头兵。

油气结构优化,天然气占公司能源结构比重近 50%。公司持续推进常规天然气以 及致密气、页岩气、煤层气等非常规天然气的勘探开发,多渠道引进国外天然气资源, 构筑多元化能源供应体系。2021 年,公司低碳天然气资源产量首次超过重碳石油资源 产量,是一次具有里程碑意义的油气结构转型。公司将继续实施“稳油增气”战略, 推动天然气产量快速增长,目标到 2025E 天然气产量占国内油气产量的比例将提升至 55%,实现从油气供应商向综合性能源公司的转型。

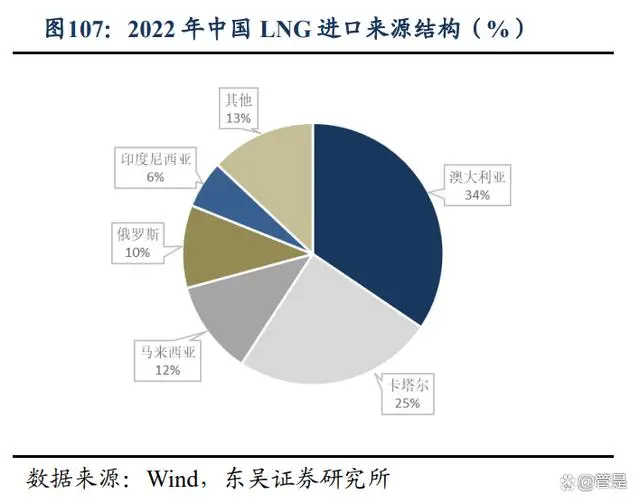

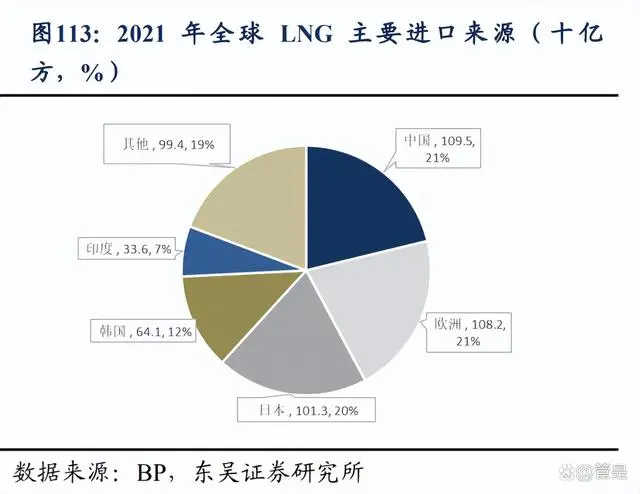

外购气: 我国进口气主要分为 LNG 和管输气。由于管道气进口具有局限性,跨国输气管道 建设周期偏长,且较容易受地缘政治问题的影响。而 LNG的进口是通过 LNG接收站进 入到国内,气态天然气液化之后体积缩小,运输灵活。因此,相比管道气而言,LNG 通常更受青睐。2022 年,我国进口天然气 1519 亿方,同比减少近 10%,其中 LNG 进 口占比 58.5%。我国 LNG 主要进口来源为澳大利亚和卡塔尔,两国合计占比近 60%; 管输气主要进口自土库曼斯坦,占比达 56%。此外,俄罗斯也是我国天然气重要进口 来源国。

国际天然气价格与原油价格高度相关,LNG 波动尤为剧烈,管输气价格相对稳定。 2023年初以来,原油价格持续在 80美元/桶附近震荡,较上年有明显回落,对气价产生 下拉作用;叠加冬季气温偏暖、欧洲有意需求压减以及地缘政治溢价减弱等原因,国 际气价出现下行趋势,我国 LNG 和管输气进口价也环比回落。2023 年中石油外购天然 气成本相比 2022 年有望下降,板块业绩有望改善。

天然气价格改革稳步推进,上下游价格有望实现联动。我国现行的天然气定价机 制为基准门站价格管理。供需双方可以基准门站价格为基础,在上浮 20%、下浮不限 的范围内协商确定具体门站价格。目前,我国国产陆上气和 2014 年底投产的进口管道 气的基准门站价由政府管制;海上气、页岩气、LNG、直供用户、2015 年投产的进口 管道气等门站价由市场形成。当前,国内天然气上游门站价格市场化程度已超过 50%, 且波动频繁,但下游价格疏导不够顺畅。未来有关部门或将建立健全规则相对统一的 天然气上下游价格联动机制,公司天然气销售的成本传导压力将进一步减小。

2、公司管道资产并入国家管网

管道资产注入国家管网集团。2020 年 7 月 23 日,中石油公告拟将所持有的主要油 气管道、部分储气库、LNG 接收站及铺底油气等相关资产出售给国家管网集团,获得 国家管网集团 29.9%股权,并成为国家管网的最大股东。自 2021 年 3 月 31日 24时起, 昆仑能源持有的北京管道公司 60%股权、大连 LNG 公司 75%股权全部转移至国家管网 集团。 管道重组后,公司天然气管道长度 1.7 万公里(截至 2021 年底),共计拥有 3 座 LNG 接收站(截至 2022 年 10 月),分别为:江苏如东 LNG 接收站、河北曹妃甸 LNG 接收站和中油深南 LNG接收站。公司重组后的 LNG接收站设计产能和储存能力仍然充 足,截至 2022 年 10 月,公司 LNG 接收站的总设计产能 1677 万吨/年,占全国接收站 设计产能的 15%;储罐能力 240 万立方米,占全国储罐能力的 17%。

此外,公司可以充分利用国家管网全国油气储运设施,提升运营效率及价值创造 能力。截至 2021 年 9 月末,天然气管道方面,国家管网在役天然气管道总里程 4.9 万 公里,约占全国干线管网的 62%,拥有 5 座地下储气库;LNG 接收站方面,国家管网 拥有 7 座 LNG 接收站,建成 21 座储罐。同时,根据国家管网集团提供的发展规划,随 着新建管道的逐步投运,国家管网集团具有良好的成长潜力,预计可为公司带来积极 的财务影响,支持核心业务发展。

3、国际气价下行,欧洲或尽早开启天然气补库

天然气是目前全球范围内比较稳定的清洁能源,其二氧化碳排放强度小于石油和 煤炭,且在解决风电、光伏发电存在的间歇式、不稳定问题上也可以发挥重要作用。 当前天然气的供给主要分为管道气和液化天然气(LNG)。相连大陆之间多采用管道输 送,而液化天然气多用于跨洋运输。由于全球天然气资源分布不均,主要的天然气生 产国家为美国、俄罗斯、伊朗、中国、卡塔尔等国。结合各国国内天然气消费需求量 来看,欧洲和亚太地区是主要的进口地区,而澳大利亚、卡塔尔、美国、俄罗斯是主 要的出口地区。

俄罗斯曾是欧洲最重要的天然气供给国。据国际能源署(IEA)数据显示,2021 年,欧洲从俄罗斯进口天然气总量约 1550 亿立方米,其中约 1400 亿立方米为管道气, 还有大约 150 亿立方米以 LNG 形式交付。整体来看,从俄罗斯进口天然气总量占欧洲 2021 年天然气进口量的 37%左右。而这一比例在 2022 年出现大幅下降,2022 年 1-10 月俄罗斯进口天然气占比只有约 20%,这一下降的主要原因是俄乌冲突导致俄罗斯向 欧洲停供天然气。

俄罗斯停供管道天然气,LNG 成供应欧洲主力。欧洲从俄罗斯运输天然气的主要 管道有北溪管线、乌克兰管线和土耳其流管线等,其中北溪管线的运输量最大,单管 线设计供气量为 550 亿方/年。而俄乌战争发生后,俄罗斯方宣布北溪 1 号天然气管道 因突发故障,将无限期关闭,这导致俄罗斯出口欧洲的天然气量大幅减少。为弥补俄 罗斯出口量的下降,欧洲加大了 LNG 的采购力度。

RepowerEU能源独立计划:可再生能源替代天然气。为加速摆脱对俄罗斯的化石燃 料的依赖,欧盟委员会 2022 年于 5 月正式公布了 “RepowerEU” 能源转型行动方案,该 方案计划在 2030 年前投资 3000 亿欧元,通过加快可再生能源产能部署、能源供应多样 化、提高能效等措施实现欧洲能源独立。在该政策推动下,可再生能源将逐渐取代部 分天然气需求。 供需矛盾尚不显著,海外天然气价格持续下降。2023 年初,欧洲地区平均气温高 于预期,1-3月供暖季的需求偏低,工业用气量减少,居民用气量有所控制;同时,欧 洲 LNG 进口量持续保持高位,供需矛盾尚不显著,天然气价格持续下降。欧洲的冬季 供暖从每年 9月开始,次年3月结束。供暖季结束后,欧洲各国的天然气储备将达到谷 值。由于欧洲进口结构已然发生变化,通过进口LNG实现储气的周期更长,欧洲或将 在今年早些时候开启储气。

(本文仅供参考,不代表我们的任何投资建议。如需使用相关信息,请参阅报告原文。)

翻译:

First, carrier-class oil and gas taps

1, Basic profile of the company

China National Petroleum Corporation Limited (” petrochina “or the” Company “) is the largest producer and marketer of oil and gas in the dominant oil and gas industry in China and one of the largest oil and gas companies in the world. The company was founded on November 5, 1999, and is a joint stock limited company established on the basis of the restructuring of the former China National Petroleum Corporation (now China National Petroleum Corporation Limited, referred to as “China Petroleum Group”).

The Company’s H shares and A shares were listed on the Stock Exchange of Hong Kong Limited (the “Hong Kong Stock Exchange”) on 7 April 2000 and the Shanghai Stock Exchange on 5 November 2007 respectively (Stock code 857 on the Stock Exchange of Hong Kong). Shanghai Stock Exchange Stock code 601857). Petrochina is a comprehensive international energy company engaged in a wide range of businesses related to oil and gas, integrating domestic and foreign oil and gas exploration and development and new energy, refining and chemical sales and new materials, support and services, capital and finance.

Sasac actual holding, subsidiaries extensive business.

The direct controlling shareholder of the company is China National Petroleum Corporation, which holds 82.46% of the company’s equity, and China National Petroleum Corporation is a super large state-owned enterprise directly under the State-owned Assets Supervision and Administration Commission of the State Council, so the State-owned Assets Supervision and Administration Commission of the State Council is the actual controlling person of the company. At present, the company has a number of wholly-owned subsidiaries and joint ventures in the world, covering petroleum and natural gas exploration and exploitation, transportation and sales, petroleum refining, petrochemical and other chemical products and new materials production, storage and transportation, import and export of petroleum, natural gas, petrochemical products and other services and technologies, new energy development and other activities.

CNPC’s main business is divided into four major sectors: oil and gas and new energy, refining chemical and new materials, natural gas sales and sales. Among them, oil and gas and new energy involve the exploration, development, production and sales of crude oil and natural gas as well as new energy business. The refining, chemical and new materials segment mainly includes the refining of crude oil and petroleum products, the production and sales of basic and derivative chemical products and other chemical products as well as new materials business. The sales segment mainly involves the sales and trading of refining products and non-oil products. The natural gas and pipeline segment consists primarily of natural gas sales, as well as oil and gas pipeline transportation.

2, Company performance

The net profit of the company is highly positively correlated with the oil price. In 2020, the impact of the new coronavirus epidemic, domestic production and life stagnation, oil prices plummeted, the company’s earnings were greatly affected, operating income fell 23.2%, and net profit fell 58.4%. With the weakening of the impact of the epidemic and the recovery of international oil prices, the company’s profit has rebounded significantly, and the operating income in 2021 has increased by 35.2% and the net profit of the parent has increased by 385.0%. In 2022, the Russia-Ukraine conflict catalyzed the international oil price to a new high, and the company’s profit continued to rise, the company’s operating income was 3,239.17 billion yuan, up 23.9% year-on-year, and the net profit of the mother was 149.38 billion yuan, up 62.1% year-on-year.

The oil and gas and new energy sectors are the main profit sources in 2022.

From the perspective of revenue, the sales sector contributes the most to the company’s operating income. From the perspective of gross profit margin, oil and gas and new energy sectors are highly positively correlated with oil prices, refining and new materials sectors and sales sectors are negatively correlated with oil prices, and the gross profit margin of natural gas sales sectors is at a long-term low. From the perspective of gross profit, the high oil price period is mainly contributed by the oil and gas and new energy sector, while the low oil price period is mainly contributed by the sales sector. In 2022, with the high oil price, the gross profit of the oil and gas and new energy sector reached 240 billion yuan, an increase of 67.5% year-on-year.

The level of capital expenditure is stable, and the peak of refining and chemical investment has passed. Since 2018, the level of capital expenditure of petrochina has remained basically stable. From 2021 to 2023E, the proportion of oil and gas and new energy sector expenditure was stable at 80%, and the proportion of refining and new materials sector expenditure continued to decline from 21.7% to 14.0%, and the peak of investment in refining and chemical projects was about to pass. The actual capital expenditure of the company in 2022 is 274.3 billion yuan, and the planned capital expenditure of the company in 2023 is 243.5 billion yuan, which is 0.62% higher than the planned capital opening level of the same period last year, and 11.23% lower than the actual capital expenditure level of the same period last year.

3, Financial status of the company

After the epidemic, the net profit rate on sales and the return on equity rebounded, and the profitability improved. During the oil price cycle from 2011 to 2022, the company’s net profit rate on sales fluctuated in the range of 1.5% to 7.5%, and it also showed strong impact resistance when the oil price was depressed in 2016 and 2020, and still maintained positive net profit rate on sales and ROE. After the impact of the epidemic in 2020, petrochina’s net profit rate on sales and ROE have rebounded significantly.

The company’s asset-liability ratio is stable and moderate. In the past ten years, the company’s asset-liability ratio has stabilized at about 45%, reflecting the company’s sound financial situation. Compared with domestic and foreign oil companies, the company’s asset-liability ratio is at a moderate level. The company’s operating cash flow increased, consolidating the financial foundation. In the past five years, the company’s operating cash flow has been sufficient and stable at 350-400 billion yuan, and has continued to rise from 2021 to 2022, providing financial support for the high-intensity capital expenditure required for the company’s operation and development.

Second, oil and gas and new energy: steady pace of oil and gas increase, new energy business speed up

1, Oil and gas and new energy business segment

Petrochina is the largest oil and gas producer in China. The company is mainly engaged in oil and gas exploration and exploitation in the upstream. And has many large oil and gas areas such as Daqing, Changqing, Tarim, Southwest, Xinjiang and Liaohe. Among them, the Daqing oil area is the largest oil field in China, with annual crude oil output of 30.03 million tons in 2022. Which has remained above 30 million tons for eight consecutive years.

Changqing Oilfield is the largest oil and gas field in China. With an annual output of 25.7 million tons of crude oil and 50.65 billion cubic meters of natural gas in 2022. And an annual oil and gas output equivalent of 65 million tons. In addition, in the unconventional field, CNPC has also actively promoted the construction of shale oil and shale gas national demonstration zones. And fully promoted the exploration and development of shale oil and gas in an integrated way. In 2022, the total output of shale oil and gas increased 2.9 times and 2.3 times respectively compared with 2018.

The operating efficiency of oil and gas and new energy sectors is highly correlated with oil prices.

The operating income of the company’s oil and gas and new energy sectors is positively correlated with oil price fluctuations. And the gross profit margin of the sectors fluctuates greatly with oil prices. In 2022, under the environment of sharply rising oil prices. The gross profit of the sector will be +67.5% year-on-year to 240.11 billion yuan. And the gross profit margin will be +5pct year-on-year to 26.40%.

The change of upstream capital expenditure of the company is positively correlated with the oil price. And is also affected by the national policy of increasing storage and production. The company’s capital expenditure in 2022 will be 274.3 billion yuan. Among them, the capital expenditure of oil and gas and new energy was 221.6 billion yuan. Which was mainly used for the exploration and production of economies of scale in key basins. Such as Tarim, Sichuan, Ordos, Junggar, Songliao and Bohai Bay, increasing the development of unconventional resources such as shale gas and shale oil. And promoting new energy projects such as clean power and CCUS; Overseas. We actively responded to changes in the situation, focused on key blocks to deepen exploration for economies of scale, strengthened capacity construction of key projects in the Middle East, Central Asia, and the Americas, and continued to optimize business layout and asset structure.

It is estimated that the capital expenditure of the Oil and Gas and New Energy segment in 2023 will be 195.5 billion yuan

It is estimated that the capital expenditure of the Oil and Gas and New Energy segment in 2023 will be 195.5 billion yuan. Mainly to continue to strengthen the exploration and development of economies of scale in key domestic basins. Such as Songliao, Ordos, Junggar, Tarim, Sichuan and Bohai Bay. And to increase the development of unconventional resources such as shale gas and shale oil. Promote clean power, CCUS, hydrogen demonstration and other new energy projects. Overseas to improve the concentration of business development, promote efficient development. Do a good job in the operation of existing projects in the Middle East, Central Asia, the Americas, Asia Pacific and other cooperation zones. At the same time, increase efforts to obtain high-quality projects. And continue to optimize the asset structure, business structure and regional layout.

Petrochina oil and gas operating cost advantage is prominent. In the past five years, petrochina and Sinopec’s oil and gas operating costs have been relatively stable. Fluctuating between $11-13 / barrel and $14-17 / barrel, respectively. And petrochina’s oil and gas operating costs per barrel are lower. Lower oil and gas operating costs allow companies to stay afloat even during periods of low oil prices. Oil and gas operating cost advantages effectively ensure the company’s profit space, consolidate the leading competitive advantage.

The company insists on efficient surveying and has made new progress in stabilizing oil and gas.

In terms of crude oil development, the company has strengthened risk exploration efforts based on key areas. Intensified the exploration of Ordos Mesozoic conventional oil, Songliao Gulong shale oil and other areas of increased storage. And focused on the exploration of new formations in Mahu Shawan, Junggar, Qixia-Maokou and other strategic replacement areas. Striving to achieve strategic discoveries and breakthroughs. In 2022, the company produced 906 million barrels of crude oil, an increase of approximately 2.1%. In 2023, the company plans to produce 913 million barrels of crude oil, an increase of 0.7%. In terms of natural gas development, the company accelerated the construction of gas field production capacity.

Among them, Changqing, Southwest and Tarim are the main areas of production and production increment. In 2022, the company produced 4,675 billion cubic feet of natural gas. Accounting for 46.23% of its oil and gas production equivalent. In 2023, the company plans to produce 4,888.9 BCF of natural gas, an increase of 4.6 percent. Combined, the company produced 1.69 billion barrels of oil and gas equivalent in 2022, an increase of approximately 3.73%. In 2023, the company plans to produce 1.728 billion barrels of oil and gas equivalent, an increase of 2.51%.

The company’s reservoir is fully developed and its natural gas reserves are stable.

In terms of crude oil. First, the economic recoverable reserves adjust with the oil price. And the decline of oil price leads to the decline of the company’s economic recoverable reserves. Second, with the steady and continuous production of crude oil, the discovered recoverable reserves continue to be depleted. And the two reasons have led to a significant decline in the company’s remaining recoverable crude oil reserves after 2014, from 10.59 billion barrels in 2014 to 6.42 billion barrels in 2022. In terms of natural gas, the company’s overall strategy of stabilizing oil and gas from 2014 to 2016 has promoted the increase of natural gas storage and production. And the remaining recoverable natural gas reserves have decreased slightly in 2016 to 73.5 trillion cubic feet in 2022.

From a horizontal comparison point of view. Petrochina’s remaining recoverable oil and gas reserves account for the largest proportion in the “three barrels of oil” company. But due to the longer mining life of onshore oil and gas fields in China. The decay problem is more obvious. And in recent years, the proportion of petrochina’s reserves in the “three barrels of oil” has continued to decline. Accounting for 67.5% of the reserves level of 18.66 billion barrels of oil equivalent in 2022.

Petrochina’s storage and production ratio ranks first in the “three barrels of oil”. And the company’s storage and production ratio is relatively stable from 2020 to 2022. And the company’s recoverable life of oil and gas in 2022 is 11 years. Due to the long exploitation time of onshore oil and gas fields. The company’s reserve replacement rate in the past five years is less than the other “two barrels of oil”.

2, to ensure national energy security, increase storage and production

To promote the energy revolution, we need to maintain the steady growth of crude oil and natural gas production capacity. Energy is an important material basis of the national economy. Affecting the country’s macroeconomic development and controlling the country’s future destiny. With the intensification of the energy revolution, it is urgent to accelerate the strategic adjustment of China’s energy structure. Consolidating the foundation of domestic energy production and ensuring basic people’s livelihood is the prerequisite of energy revolution. In the context of the “double carbon” goal, oil and natural gas are the most important primary energy sources besides coal. And maintaining the stable growth of crude oil and natural gas production capacity is an important basic measure for the adjustment of the national energy structure.

The demand for crude oil in China continues to grow, and the dependence on foreign countries gradually rises. Since 2003, China has become the world’s second largest oil consumer and the largest crude oil importer.

In 2017, China surpassed the United States to become the world’s largest net importer of crude oil. In fact, oil and gas resources are relatively abundant in our country. According to the 2022 China Mineral Resources Report, China’s proven oil reserves reached nearly 3.7 billion tons. In the third oil resources assessment, China’s total offshore oil reserves can reach nearly 25 billion tons. Although China is rich in oil resources, due to the geographical conditions and the difficulty of exploitation. The investment cost of crude oil exploitation in China is high. So the exploitation volume is always maintained at the medium level.

In the past decade, China’s crude oil production has grown slowly. Reaching a stage peak of 215 million tons in 2015, and then began to decline. On the other hand, domestic crude oil demand has been growing steadily in the past decade, reaching 718 million tons in 2021, an increase of 6.33%. Under the double impact of exploitation problems and high-intensity consumption. China’s dependence on foreign oil resources has gradually climbed and remained high. In 2022, China’s crude oil production will reach 204 million tons. And net imports will reach 520 million tons, with import dependence as high as 72%.

The demand for natural gas will increase significantly, and China’s production still needs to be increased.

Natural gas is a kind of clean and environmentally friendly high quality energy source. With the acceleration of China’s energy structure transformation. The market has put forward higher requirements for the exploration and development of natural gas resources and the production and supply capacity. Although China’s natural gas exploration and development has made remarkable achievements, production and supply capacity has gradually increased,. And the compound growth rate of natural gas production has reached 7.23% in the past ten years. The demand is still in short supply.

In the past 11 years, China’s natural gas demand has increased significantly. In 2010, China’s natural gas demand was 108.9 billion cubic meters. By 2021, China’s natural gas consumption reached 378.7 billion cubic meters. An increase of more than twice, the compound growth rate of up to 12%. Therefore, the external dependence of natural gas in our country is also growing gradually. In 2021, China’s natural gas production will be 209.2 billion cubic meters. Net imports will be 169.5 billion cubic meters, and import dependence will be 45%. With the tightening of environmental protection policies and the acceleration of the process of coal to gas projects. China’s future natural gas demand will continue to increase significantly, and its external dependence may exceed 50%.

Policy level to promote, support and promote the rapid growth of oil and gas production.

There is a contradiction between the increasing energy demand and the actual supply. Which restricts the sustainable development of our country in the future. And it is urgent to reduce the external dependence of oil and natural gas. In March 2021, the 14th Five-Year Plan clearly requires oil and gas exploration and development to be included in the core technology of national scientific and technological research. It emphasizes consolidating the domestic production base, maintaining stable production and increase of crude oil and natural gas. And doing a good job in planning, layout and control of coal-to-oil and gas strategic bases.

In February 2022, the National Development and Reform Commission and the National Energy Administration issued the “Opinions on Improving the Institutional Mechanisms and Policy Measures for the Green and Low-carbon Energy Transformation”, which once again emphasized the improvement of the clean and efficient utilization mechanism of oil and gas and the improvement of the clean and efficient exploitation capacity of oil and gas fields. In the future, as the exploration and development of oil and natural gas resources continues to increase. The policy level will promote, support and promote the rapid growth of oil and natural gas production. Especially clean energy natural gas will welcome a breakthrough period of rapid growth.

3, oil prices or continue to stabilize at a high level

Supply side: Global upstream capital expenditure growth is limited, and supply elasticity in major crude oil producing countries is declining

The lack of global upstream investment in crude oil from 2015 to 2021 has led to the current tight crude oil supply. And high oil prices in 2022 have not driven upstream capital spending. In 2020, the COVID-19 pandemic hit international oil prices. And global upstream capital expenditure contracted by $149 billion from 2019, a 31% decrease from the previous year. In 2021, the global economic recovery combined with OPEC+ alliance production cuts, Brent oil prices reached an average of 70.94 US dollars/barrel, an increase of 64% compared with 2020. But the global upstream planned capital expenditure increased by 25 billion US dollars compared with 2020, only an increase of 7.7%.

However, it is still significantly lower than 2019 levels. At the beginning of 2022, international oil prices rose all the way to more than $90 / barrel. But the upstream spending planned by global oil and gas companies at the beginning of 2022 was only $33 billion higher than actual capital spending in 2021. An increase of only 8.6% year-on-year, and still significantly lower than the level in 2019.

Affected by the transition of new and old energy sources, the willingness to invest in traditional oil and gas in the future is insufficient.

We believe that in the process of the transformation of the new and old energy structure. The demand for crude oil will peak around 2027, if the investment is increased now. The development and production cycle of traditional oil fields will take 3-5 years, and the demand will decline after production. And the long-term return rate of traditional crude oil projects will be uncertain. Faced with this problem, European companies (such as Shell) transition to integrated energy service providers, oil and gas production decline; American companies (such as Chevron, Conocophillips, Occidental Petroleum) focus on traditional energy. But oil and gas production is only stable, and the willingness to increase significantly is not strong.

The current decline in Russian crude oil production is limited. In April 2022, the impact of the Russia-Ukraine conflict appeared. And Russian crude oil production fell by 900,000 barrels per day from the previous month to 9.1 million barrels per day. However, since May 2022, with the transfer of Russian crude oil export trade to India and China, Russian crude oil production has gradually recovered, as of February 2023, crude oil production has recovered to 9.91 million barrels per day, 170,000 barrels per day lower than before the conflict between Russia and Ukraine (referring to January-February 2022, the same below). The decline was limited.

As of February 2023, Russia’s oil exports declined due to the EU’s embargo on Russian refined oil products and the G7’s price limit policy on Russian refined oil products.

In February 2023, Russia’s total oil exports were 7.5 million b/d, down 600,000 b/d from pre-conflict levels and 500,000 b/d from January 2023, of which 4.9 million b/d were crude oil exports, down 100,000 b/d from pre-conflict levels and down 200,000 b/d from the previous month. Exports of refined products were 2.6 million b/d, down 500,000 b/d from pre-conflict levels and 300,000 b/d from the previous month. Capital expenditure is insufficient, and Russian crude oil production has reached capacity bottlenecks. According to the International Energy Information Agency (IEA), Russia’s crude oil production capacity has fallen from 10.42 million barrels per day in October 2021 to 10.2 million barrels per day in 2023. And Russia’s crude oil production capacity has been declining. In March 2023, Russia plans to cut production by 500,000 barrels per day, which could cause further supply contraction.

As of October 2022, the actual OPEC+ production increase has not reached the planned target. On the one hand, countries with the capacity to increase production such as Saudi Arabia and the United Arab Emirates maintain cautious production increases, on the other hand. Other OPEC+ countries have reached production bottlenecks and are unable to increase production.

At the October 2022 ministerial meeting, OPEC+ decided to continue to reduce production by 2 million barrels per day on the August 2022 production target base. And the reduction range is from November 2022 to December 2023. The current round of production cuts began until February 2023, and OPEC+ actual production was stable at less than 40 million barrels per day. And the implementation of production cuts was good. From May 2023 to the end of 2023, Saudi Arabia, along with other OPEC and several non-OPEC members. Voluntarily cut oil production by more than 1.6 million barrels per day.

This round of production reduction faces the objective constraint of insufficient capacity to increase production.

On the one hand, OPEC+ production reduction burden countries can better implement the production reduction plan. On the other hand, countries that do not meet production targets are struggling to achieve significant increases due to insufficient capacity. Because of this, we are more optimistic about the implementation of this round of production reduction plan. When some OPEC+ countries have reached their production limits and the global crude oil supply strain has not been effectively alleviated. Only Saudi Arabia and the United Arab Emirates have surplus production capacity. Which is 1.75 million barrels per day and 890,000 barrels per day respectively by February 2023. We believe that Saudi Arabia’s internal coordination capacity and oil price regulation capacity have been further enhanced. Its willingness to keep prices high is strong. And its efforts to curb production to prop them up may be more effective.

The recovery of US crude oil supply after the epidemic is slow.

First, the major shale oil and gas companies in the United States are choosing to return more earnings to shareholders rather than expand investment amid tighter capital constraints from investors. Second, under the impact of the epidemic in the early stage, shale oil companies used inventory Wells to maintain production. After the epidemic, oil and gas companies need to accelerate the drilling of new Wells at higher costs to make up for the consumption of high-quality Wells in the past to achieve production increase.

Third, the shortage of human and material resources and the rising cost have become the main problems faced by US shale oil companies in oil and gas production. Which has prolonged the oil and gas production cycle and slowed down the production rate. According to the US Energy Information Administration (EIA). It is expected that the US crude oil production will increase by 560,000 barrels per day to 12.44 million barrels per day in 2023. And the US crude oil production will gradually recover, but the increase in production will be limited. And the average annual increase in production will not be as high as 1.5 million barrels per day before the epidemic.

Demand side: It will take time for crude oil demand to peak

Transportation gasoline and diesel accounted for half of the global oil consumption. Mainly considering the impact of the replacement effect of new energy vehicles. Considering that the high price of traditional energy promotes the acceleration of the penetration of new energy vehicles. We adopt the scenario assumption that the penetration rate of new energy vehicles will rise according to the S-type. According to our model, we predict that by 2025. The consumption of gasoline and diesel in the global transportation sector will peak. And the penetration of global new energy vehicle sales in 2025 will be 24%. Subsequently, due to the rapid penetration of new energy vehicles. The global ownership of new energy vehicles continues to accelerate growth. The global demand for general gasoline and diesel has accelerated decline. And the global sales penetration of new energy vehicles will reach 100% by 2040.

Based on our forecast that global demand for gasoline and diesel for transportation will peak in 2025, as well as our assumptions and models for aviation kerosene, industrial oil, chemical oil and other oils, we expect total global demand for crude oil to peak around 2027.

There is a growth gap of about 4 million BPD between peak demand in 2027 and total demand in 2022. From 2027 to 2040, the rapid replacement of new energy vehicles will lead to a sharp decline in transportation gasoline and diesel year by year. And the total demand for crude oil will accelerate the decline.

From 2040-2060, the market will no longer sell traditional fuel vehicles. And the annual consumption of transportation gasoline and diesel will slowly decline year by year with the scrapping of traditional energy retention vehicles. And the decline in crude oil demand will slow down. It is expected that the increase of global crude oil demand in 2022-2023 will be 1.5 million to 2 million barrels per day. And the increase of global crude oil demand in 2024-2026 will be about 1 million barrels per day. And the global crude oil demand will reach its peak in 2027. In the medium and long term, global crude oil demand still maintains a growth trend. And the peak moment has not yet arrived.

From the long-term demand structure, the proportion of gasoline and diesel consumption for transportation will decrease year by year, and the proportion of chemical oil will increase year by year, and chemical oil will become the main incremental source of crude oil demand in the future.

Oil prices are expected to remain high in 2023. Supply side, tight. Under the background of energy structure transformation, international oil companies still maintain cautious and restrained production pace, capital expenditure is limited. And the willingness to increase production is insufficient. Affected by sanctions, Russia’s crude oil production capacity is insufficient and will decline to a certain extent. The supply elasticity of OPEC+ has decreased. The willingness to cut production to support oil prices is strong, and Saudi Arabia’s price control ability has increased. The US crude oil production is limited, there are long-term production bottlenecks. And the release of strategic crude oil stocks from 2022 into 2023 replenishment cycle.

On the demand side, growth.

In the first half of this year, the domestic economy recovered but the overseas economy declined. And in the second half of the year, the domestic and foreign economies further recovered. And the demand side showed a pattern of low before high.

Overall at home and abroad, global crude oil demand is still growing. In addition, we believe that even if there is an economic recession in 2023. Because the Federal Reserve will slow down interest rates or even cut interest rates in order to revive the economy. The Saudi-led OPEC+ supports oil prices by controlling production, and non-OPEC cannot increase production on a large scale. The possibility of a sharp fall in oil prices is small. In the absence of sudden large shocks, oil prices will continue to operate at a relatively stable high level. Petrochina’s oil and gas and new energy sector performance or will continue to maintain stable and good performance.

4, new energy business speed up

The company’s new energy business accelerated development. In 2022, CNPC’s investment in new energy will reach 7.67 billion yuan, an increase of 252% year on year. The construction of key projects will be accelerated. And the development of clean production energy alternatives and external clean energy supply markets has achieved remarkable results. Actively obtain clean power grid connection indicators, vigorously develop wind power, photovoltaic power generation, geothermal heating and carbon capture, utilization and storage (” CCUS “) business, the first wind and storage integration development project – Daqing Oilfield two small distributed power cluster application demonstration project phase I connected to the grid power generation. The cumulative wind power installed capacity of more than 1.4 million kilowatts.

The cumulative geothermal heating area has reached 25 million square meters. And the development and utilization capacity of new energy has reached 8 million tons of standard coal per year. The company aims to achieve the proportion of new energy production capacity to reach 7% of primary energy production by 2025. And strive to supply green zero-carbon energy to exceed its own consumption of fossil energy by 2035. Basically realize the strategic replacement of heat, electricity and hydrogen for oil and gas business. And strive to achieve “near zero” emissions by 2050. And the capacity of new energy business occupies half of the country.

Third, refining and new materials: Stricter policies + industry improvement, sector performance is expected to usher in improvement

1, The approval of refining and chemical projects has become stricter, and CNPC has more inventory advantages

Since September 2021, the CPC Central Committee and The State Council have issued the Opinions on Fully. Accurately and Comprehensively Implementing the New Development Concepts to Achieve Carbon Peak Neutrality. And The State Council has issued the Notice on Issuing the Action Plan for Carbon Peak before 2030 (Guofa (2021) No. 23). The National Development and Reform Commission issued the “Several Opinions on Strict Energy Efficiency Constraints to Promote Energy Conservation and Carbon Reduction in Key Areas” and the “Action Plan for Strict Energy Efficiency Constraints to Promote Energy Conservation and Carbon Reduction in Key Petrochemical and Chemical Industries (2021-2025)” to promote the carbon peak in the petrochemical industry and strictly control new refining capacity.

By 2025, the domestic primary processing capacity will be controlled within 1 billion tons. And the capacity utilization rate of main products will be increased to more than 80%. In December 2021, the Central Economic Conference pointed out that new renewable energy and raw material energy use will not be included in the total energy consumption control. We believe that in the context of limited supply side development. The subsequent substantial new refining and chemical capacity is limited.

Less than 100 million tons of refining capacity per year is under construction or planned for 2023 and beyond. CNPC’s Guangdong Petrochemical 20 million tons/year refining and chemical integration project in February 2023 to achieve full production, Shandong Yulong Island phase I 20 million tons/year project and Zhenhai refining and chemical 11 million tons/year project is expected to be completed in 2023.

On the other hand, according to the “14th Five-Year Plan” petrochemical industry planning guide given by the Petroleum and Chemical Industry Planning Institute

On the other hand, according to the “14th Five-Year Plan” petrochemical industry planning guide given by the Petroleum and Chemical Industry Planning Institute. During the 14th Five-Year Plan period, China will continue to promote refining enterprises to “reduce oil and increase”. And the oil yield of new refining and chemical projects is low.

The focus of the “14th Five-Year Plan” petrochemical industry planning is to eliminate small production capacity, integrate refining indicators, build a longer process, a higher operating rate, and a more diversified refining and chemical integration project, improve the efficiency of China’s petrochemical production, reduce the waste of oil products in the production process. And achieve the “eat dry squeeze” of resources. With the development of the national policy direction and the refined and differentiated value of downstream chemicals continuously excavated in the actual operation process. Under the background of double carbon. The refinery extending to the downstream chemical materials and taking the path of small oil head and large chemical industry has become the future development trend.

From the perspective of China’s “oil reduction and increase” policy orientation and the oil yield of large refining and chemical projects. Although China’s refining capacity will increase in the next few years, the oil yield is not high. And the contribution to the oil supply is limited. In this case, the petrochina refining sector may particularly benefit from the upcoming contraction in the supply side of refined oil products. At present, the company still has a number of key refining and chemical projects under construction. The future of the refining and chemical sector is still promising.

2, Basic situation of refining, chemical industry and new materials business

The company’s refining capacity ranks second in China. CNPC has continuously improved the smooth operation level of refining and chemical plants. And the smooth operation rate of the plant reached 99.7% during the year. By the end of 2021, the company has a total of 8 large-scale refining and chemical integration enterprises in China and 13 10 million tons of refineries. Refining gross margin is negatively correlated with crude oil prices. In 2022, under the catalytic role of the Russia-Ukraine conflict, the international crude oil prices are high. And the rise in crude oil prices leads to the increase in the procurement cost of refining raw materials. Which leads to a decline in refining gross margin of 1.8pct to 7.1%. In 2022, the company’s refining and chemical industry revenue reached 1,157,918 billion yuan, an increase of 36%.

The operating profit was 82.212 billion yuan. It was down 5 per cent year-on-year. Thanks to the company’s continuous expansion and upgrading of refining and chemical projects to improve efficiency, the profit of the refining and chemical segment in 2021-2022 was close to the level of the low oil price period in 2016-2018. In 2023, the economic recovery is accompanied by increased travel demand. And the performance of the company’s refined oil sector is expected to improve.

Basic information of refining business

The refinery structure is adjusted as needed, and the oil reduction and increase are in progress. The company’s refining products mainly include gasoline, diesel and kerosene. The company’s refined oil yield showed an overall upward trend from 2010 to 2019. After 2020, the company continued to promote transformation and upgrading, reducing oil and increasing oil. And by 2022, the company’s refined oil yield was 64.2%, falling to a 10-year low.

According to market demand, the company’s diesel ratio has continued to decline in the past 10 years. From 2.31 in 2010 to 0.98 in 2021, in 2022, domestic travel was affected by the epidemic, gasoline demand declined, diesel slightly better. The company timely raised the diesel ratio to 1.23. In addition, the company will also promote the optimal allocation of regional resources, give full play to the advantages of characteristic crude oil resources and refinery installations, optimize production routes and product programs. And increase the production of low-sulfur Marine fuel oil, paraffin, lubricating oil, asphalt and other characteristic products.

Basic situation of chemical business

The company’s chemical sector mainly has five categories of products. Which are ethylene, synthetic resin, synthetic fiber raw materials and polymers, synthetic rubber, urea. The company adheres to “reduce oil and increase”, “reduce oil and increase special”. And continuously optimize the product structure; The Japanese Research Institute of New Materials was established. The research and development of new chemical materials was increased. And the proportion of high-end special materials and high value-added products was increased significantly. In the past five years, the company’s chemical production has continued to increase. And the total output of the company’s chemical products in 2022 is 23.73 million tons, an increase of 6.8%.

3, oil refining: consumption tax supervision has become stricter, good for state-owned oil refining leaders

Crude oil prices are stable at high levels, and spreads are expected to reach their highest in recent times

In January 2016, the National Development and Reform Commission issued the “Measures for the Management of Oil Prices”. Article 6 of which more clearly regulated the pricing issue of the domestic refined oil market. That is, “when the crude oil price in the international market is lower than $40 per barrel (inclusive). The refined oil price is calculated according to the crude oil price of $40 per barrel and the normal processing profit rate.” When the price is above US $40 per barrel and below US $80 (inclusive). The price of refined oil products is calculated according to the normal processing profit rate.

When it is higher than $80 per barrel, the processing profit rate is deducted until the price of refined oil is calculated according to the zero profit of processing. Above 130 US dollars per barrel (inclusive). In accordance with the principle of taking into account the interests of producers and consumers, to maintain the stable operation of the national economy, to adopt appropriate fiscal and tax policies to ensure the production and supply of refined oil products, gasoline and diesel prices in principle, no or less.”

According to the scatter chart of international oil prices and domestic gasoline and diesel retail prices since January 2016, it can be found that this rule has a clear guiding significance in practical use.

When the international crude oil price is higher than 80 US dollars/barrel, the domestic gas and diesel prices basically no longer change. And the profits brought by cost changes are cut by enterprises. When the international crude oil price is at $80 / barrel. The price difference between domestic gasoline, diesel and crude oil has reached a stage high. We believe that in the absence of sudden large shocks, oil prices will continue to operate at a relatively stable high level. The center is slightly lower than 2022, considering Saudi Arabia’s fiscal balance oil prices. The bottom of the oil price will be at $70-80 / barrel. Therefore, we are optimistic about the future performance of the refining sector.

Domestic demand for refined oil products picked up, helping the refining business profit rise

2022Q4, affected by the peak of domestic epidemic infection, the economy is in the trough period. Using PMI assisted analysis, the PMI index in November 2022 was 48.0%, down 2.1pct year-on-year and 1.2pct month-on-month. The PMI index for December 2022 was 47%, down 3.3pct year-on-year and 1.0pct month-on-month. In 2023Q1, the PMI level reached the highest in recent years. And the trend of economic recovery after the epidemic was significant. In February 2023, the PMI index was 52.6%. An increase of 2.4pct year-on-year and 2.5pct month-on-month, reaching the highest value since 2018. In March 2023, the PMI index was 51.9%, a year-on-year increase of 2.4pct, a month-on-month decline of 0.7pct. And the expansion of both production and demand has slowed down. On the whole, 2023 is expected to usher in a rapid economic recovery after the epidemic, driving on a fast road rarely seen in recent years.

Gasoline: Urban traffic conditions are good, confirming the long-term stability of gasoline demand.

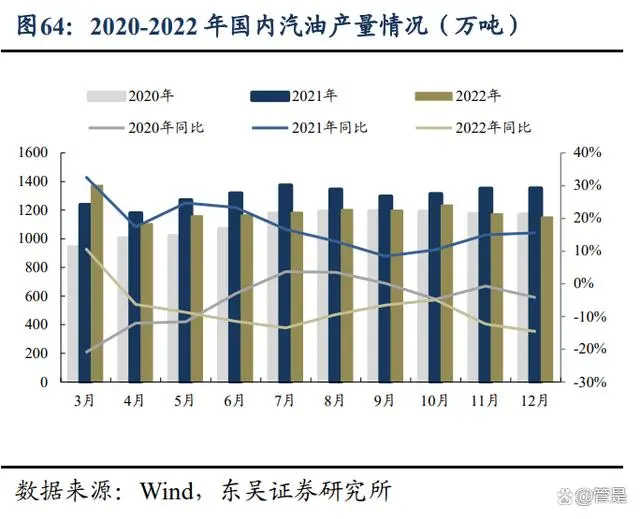

Gasoline demand is no longer constrained by the epidemic, and demand is rapidly recovering. 2022Q4 gasoline consumption is blocked, and 2023 is rapidly picking up. Affected by the epidemic in the fourth quarter of 2022 and the high price of upstream crude oil, gasoline demand has been strongly suppressed, and the domestic gasoline output in 2022Q4 is 35.613 million tons. Which is lower than the 40.179 million tons in Q4 of 2021. However, it is an increase from 35.53 million tons in Q4 2020.

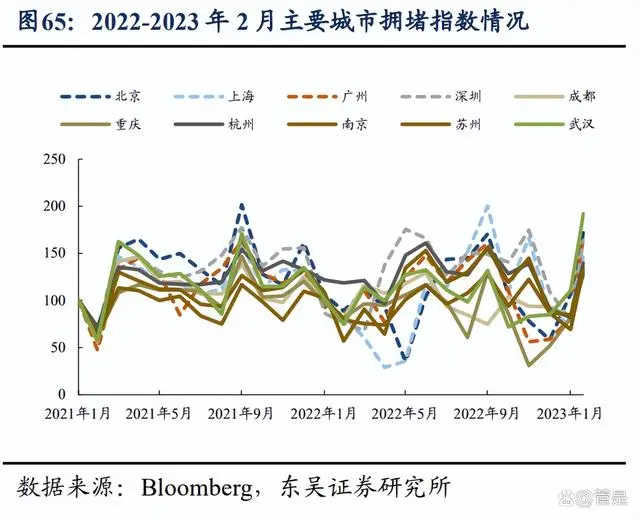

At the beginning of 2023. The number of urban traffic vehicles has increased significantly compared with the same period in previous years. In February 2023, the congestion index of Beijing reached 172, an increase of 92.96%; Shanghai’s congestion index reached 146, an increase of 73.83%. The congestion index of Guangzhou reached 167, an increase of 96.97%. Shenzhen’s congestion index reached 164, up 115.29 percent year-on-year. The congestion index of other major cities also showed an increasing trend compared with previous years.

Diesel: Infrastructure recovery signals are obvious, helping diesel demand rise.

2022Q4 diesel oil production has increased significantly compared with 2021Q4, and the growth trend is good. This strong growth is expected to continue through 2023. After the Spring Festival in 2023, the recovery signal of infrastructure is obvious. Which is expected to help the demand for diesel fuel rise rapidly. According to the statistics of the Centennial construction network. The return to work rate of 10.5% and the labor arrival rate of 14.69% on the tenth day of the first month of 2023 are lower than the level of the same period in 2021 and 2022.

However, the rate of resumption of work on January 24 reached 76.5% and the rate of labor arrival reached 68.20%. Almost the same as the level in the same period in 2021. By the beginning of February, the return to work rate reached 86.1%, and the labor arrival rate reached 83.9%. Although the return to work rate and the labor arrival rate in 2023 have not fully recovered to the level of 2021. They have significantly improved compared with 2022. This indicates that the demand for infrastructure will rise rapidly, and the demand for diesel oil will rise in 2023.

Jet fuel: Consumption is rising steadily and demand is expected to increase significantly.

Kerosene production gradually increased by the end of 2022. At the end of 2022, with the release of the prevention and control policy. China’s kerosene production exceeded the level of the same period in 2021, but has not yet recovered to the level at the end of 2020. Rising airline traffic has led to increased demand for jet fuel. The total turnover of domestic transport increased from 4.26 billion tonne-km in October 2022 to 7.39 billion tonne-km in January 2023, and the number of passengers transported also increased from 15.924 million in October last year to 39.775 million in January 2023. The forecast demand for jet fuel continues to improve.

From the perspective of domestic flights departing in the next 12 weeks, aviation fuel consumption is expected to rise from 84,200 tons/day on February 28, 2023 to 130,000 tons/day on May 16, an increase of 54.39%. Among them, domestic aviation fuel consumption will rise from 78,600 tons/day to 120,000 tons/day. The number of flights is expected to rise from 13,300 on February 28 to 20,200 on May 16, of which domestic routes will rise from 12,800 to 19,700 on May 16.

The spread of overseas refined oil products is expanding + export quotas are increasing, and the profit space is expected to be released

Due to the shutdown of overseas refineries under the impact of the epidemic in 2020 and the impact of the conflict between Russia and Ukraine in early 2022. The current overseas refined oil product price spread is still high. Since March 2022, the price of refined oil products overseas has expanded significantly. And the price spread has continuously broken through the record high. Since June to July 2022, under the continuous interest rate hike of the Federal Reserve. Weak market confidence has pushed the center of gravity of oil prices down. And the price spread of overseas refined oil products has contracted to a certain extent, but it is still oscillating at a high level.

As of the week ending March 31, 2023, the average weekly price of diesel. Gasoline and aviation coal in the United States was 113.86, 112.33 and 114.49 US dollars/barrel, respectively. The price difference with crude oil was 35.24, 33.71 and 35.87 USD/barrel, respectively. The average weekly prices of diesel, gasoline and jet fuel in Europe were $104.68, $119.25 and $108.21 per barrel, respectively. The price difference with crude oil was 26.07, 40.63 and 29.59 dollars per barrel, respectively. The weekly average prices of diesel, gasoline and jet fuel in Singapore were 99.69, 94.67 and 94.61 USD/barrel respectively. The price difference with crude oil was 21.13, 16.05 and 16.04 dollars per barrel, respectively.

Under Western sanctions, Russia’s refined oil trade transfer is more difficult.

On February 3, 2023, EU member states. The Group of Seven (G7) and Australia said they had finalized an agreement on a price cap for Russian oil products. Among them, the price cap on oil products involves two price grades, setting a maximum price of $100 / barrel for Russian oil products (such as diesel), and reaching an agreement on a maximum price limit for Russian low-quality products such as fuel oil, set at $45 / barrel. On February 5, 2023, the seaborne price cap for Russian oil products came into force. At the same time, on February 5, 2023.

The European Union imposed a total ban on imports of Russian refined oil products by se. TSince the second half of 2022, European buyers want to rebuild diesel stocks before the Russian refined oil embargo in February 2023. The EU diesel imports have increased significantly, while the proportion of diesel imports from Russia has been declining. In January 2023, Russia’s oil exports to the EU has fallen significantly by 500,000 barrels per day. The EU’s share of Russian diesel imports has fallen from 62% in July 2022 to 41%. And diesel trade between Russia and the EU remains at 700,000 b/d.

Since the European Union imposed a new price cap on seaborne Russian oil products on February 5, 2023,

Since the European Union imposed a new price cap on seaborne Russian oil products on February 5, 2023, shipping data shows that Russian seaborne oil product exports averaged 2.13 million barrels per day in February 2023, down 21% from the recent high of around 2.7 million barrels per day in January 2023. It was 24 percent below the pre-war average and the lowest level since May 2022. Mainly because new buyers in Africa failed to absorb Russian refined oil diverted from Europe, leading to a sharp decline in Russian refined oil exports.

In our view, it is more difficult for Russia to shift its refined oil trade to Asian markets than crude oil trade, because China and India are net exporters of refined oil products and it is more difficult to accept large amounts of Russian refined oil imports. In the future, the decline in Russian oil exports may further force its domestic refining capacity to decline, leading to a contraction in global refining supply and pushing up the price spread of refined oil products represented by diesel.

The relaxation of export quotas for refined oil products has helped export oil companies increase revenue and create efficiency.

In 2023, the first batch of refined oil export quotas were issued a total of 18.99 million tons, up 46% year-on-year. And the export quotas of various oil companies also increased to varying degrees compared with the same period last year. And the export quotas of China Petrochemical and China Petroleum were the highest. Respectively 7.41 and 5.96 million tons, an increase of 71.93% and 41.57% year-on-year. Together, the two accounted for 70.41% of the total oil product export quota. The first batch of quotas has landed, compared with the beginning of the 14th five-year export policy tightening period, refined oil export quotas tend to relax, boost the export mentality of oil companies, help enterprises to alleviate inventory pressure, increase revenue and create efficiency.

China’s oil export quota accounts for the second, and the overseas market has broad prospects. From 2018 to 2022, petrochina’s export quota of refined oil products has always maintained the second place after Sinopec. With 33.06%, 32.83%, 34.69%, 33.58% and 28.75%, respectively. The first batch of refined oil export quotas in 2023 has landed. And China Petroleum has continued to reach a high point, accounting for 31.38%. At present, the price spread of overseas refined oil products still maintains a high level of profitability. And with the signs of relaxing the export policy of refined oil products, petrochina overseas business prospects are broad. And the profit space is expected to be further released.

The consumption tax on refined oil products was gradually standardized, and the competitive advantage of state-owned refining and chemical industry was enhanced

As oil is a scarce resource in our country. And gasoline and diesel fuel in the combustion process will have a certain impact on the environment, so since 1994. China has been in the production link (that is, refinery) on gasoline and diesel consumption tax according to the amount. In order to urge the final consumer (cars, trucks, etc.) to save oil. So far, China’s refined oil consumption tax has been significantly increased four times, gasoline consumption tax from 0.2 yuan/liter (about 278 yuan/ton) to 1.52 yuan/liter (about 2110 yuan/ton), diesel consumption tax from 0.1 yuan/liter (about 118 yuan/ton) to 1.2 yuan/liter (about 1411 yuan/ton).

Since the consumption tax on refined oil is levied at the refinery. If the refinery pays the consumption tax according to the actual production of refined oil. The ex-factory price of refined oil is bound to be higher. And there is no competitive advantage in the face of downstream refined oil wholesalers and terminal retail gas stations. Considering that the product attributes of refined oil are difficult to judge (like oil is not oil). Some refineries (especially local refineries) have been avoiding the consumption tax on refined oil by “selling by changing the name (selling refined oil as a chemical)”. So as to obtain higher profits. However. This kind of tax evasion behavior of the refinery on the one hand did not fulfill the obligation of paying taxes in good faith. On the other hand, it also destroyed the normal operation of the refined oil market.

Therefore, the State Administration of Taxation issued No. 47 in 2012 and No. 50 in 2013 to strictly define the scope of the collection of refined oil consumption tax

Therefore, the State Administration of Taxation issued No. 47 in 2012 and No. 50 in 2013 to strictly define the scope of the collection of refined oil consumption tax. In order to prevent the leakage of the refinery’s renamed sales behavior: 1. Tax on products (products that look like oil) produced and processed by taxpayers with crude oil or other raw materials in liquid form under normal temperature and pressure shall be levied on foreign sales in accordance with the following rules:

1. Products that meet the standards of gasoline, diesel oil, naphtha, solvent oil, aviation kerosene, lubricating oil and fuel oil shall be levied on VAT in accordance with the corresponding provisions. 2, other than the provisions of 1 in line with national standards or petrochemical industry standards. And in advance of the provincial level above (including) quality and technical supervision department (only responsible for the sample) issued by the relevant product quality inspection certificate to the competent tax authorities for the record, no consumption tax. (3) Products other than 1 and 2 shall be deemed to be subject to consumption tax on naphtha.

(2) Taxpayers using crude oil or other raw materials to produce and process products such as asphalt products (products that look like asphalt) for foreign sales shall be subject to the following rules:

1, in line with the national standards of asphalt products or petrochemical industry standards. And in advance of the provincial level above (including) quality and technical supervision department (only responsible for the sample) issued by the relevant product quality inspection certificate to the competent tax authorities for the record, no consumption tax. (2) Products other than those stipulated in 1 shall be regarded as fuel oil for consumption tax purposes.

Due to the lack of smooth transmission of consumption tax payment information. The difficulty of distinguishing between refined oil and other petrochemical products. The lack of effective supervision of the production behavior of refining and chemical enterprises. And the provincial government and its tax authorities are not strict and active in the collection of consumption tax. The State Administration of Taxation No. 47 in 2012 has been implemented for many years. But the plugging effect is not obvious. Refineries represented by the land chain are still selling under the new name without paying excise tax.

In order to further solve the problem of the refinery underpaying the consumption tax on refined oil products. The State Administration of Taxation issued No. 1 in 2018: Since March 1, 2018. All invoices for refined oil products must be issued through the Finished Oil Invoice Issuance module in the new VAT Invoice Management system. Through which special invoices for refined oil VAT, ordinary invoices and electronic general invoices can be issued. And the word “refined oil” must be printed in the upper left corner of the invoice. At present, there is no such requirement for the rolled VAT ordinary invoice issued by gas stations.

Chemical industry: ethylene still has room for import substitution, and the chemical industry sector is expected to improve

Petrochina, as the second largest ethylene producer in China, accounts for about 12% of the total production capacity in 2022. In 2022, the company will accelerate the construction of ethylene projects in Guangdong Petrochemical, Jilin Petrochemical and Guangxi Petrochemical, and continue to promote the Tarim Ethylene Phase II project and the ethylene transformation projects in Fushun and Lanzhou. In November 2022, the construction project of 1.2 million tons/year ethylene plant of petrochina Jilin Petrochemical Company officially started. In February 2023, Guangdong Petrochemical, refining and chemical integration Project was fully put into operation, and 1.2 million tons/year ethylene plant produced qualified products. In March 2023, the Guangxi Petrochemical, refining and chemical integration transformation and upgrading project has completed the basic design review of the first batch of sub-main items.