多米诺骨牌的第一张,倒了。

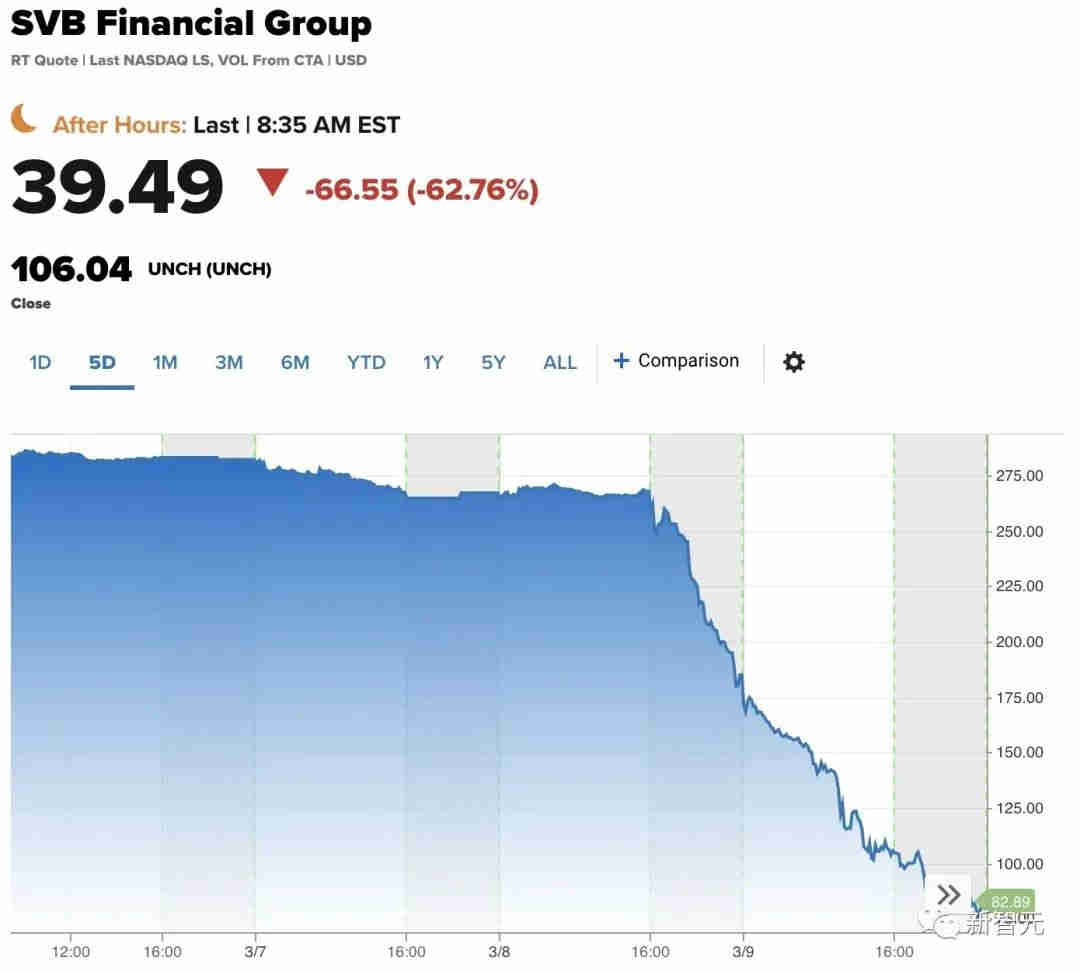

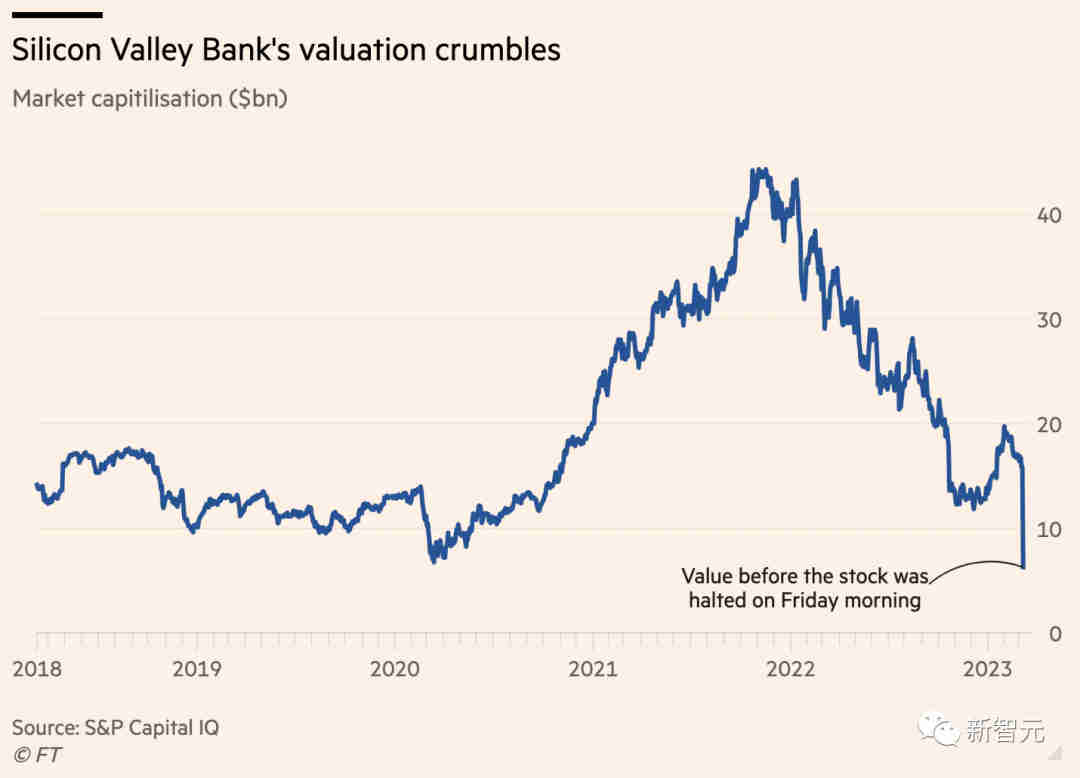

3月9日,全美第16的硅谷银行(Silicon Valley Bank,SVB)突然暴跌超过60%,市值蒸发94亿美元。

3月10日,硅谷银行宣布破产,由美国联邦存款保险公司(FDIC)接管。

这也是自2008年以来,美国金融业出现的最大倒闭案。

但讽刺的是,3月7日,硅谷银行连续5年登上福布斯年度美国最佳银行榜单,并入选福布斯首届金融全明星名单。

一、硅谷的至暗时刻

拥有约2090亿美元资产和1731亿美元存款的硅谷银行,主要为硅谷的创投公司提供资金,与整个硅谷的风险资本密切相关。

Y Combinator的首席执行官Garry Tan今天早上发帖称,硅谷银行的倒闭对于初创企业来说将是「灭顶之灾」,会让美国的创新倒退10年以上。

30%的YC公司因硅谷银行倒闭而受到牵连。由于无法使用这些资金,这将意味着他们将无法在短短30天内支付员工工资。

如果我们不找到解决办法,今天的初创公司,明天的谷歌和Meta,都将消失。

调查显示,近400家初创公司表示他们正面临风险,超过100家表示自己在未来30天内可能无法支付工资。

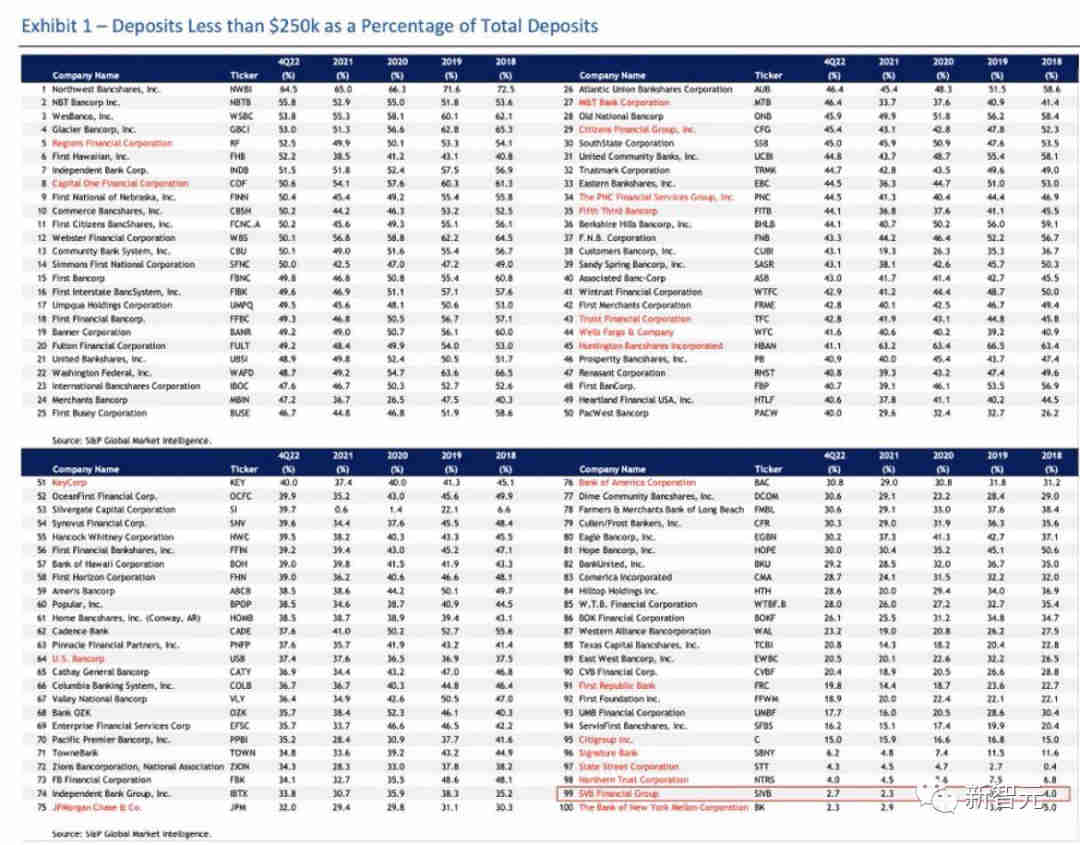

更大的问题在于,虽然FDIC接手后表示会对储户进行赔付。但初创公司存到硅谷银行的钱,大部分都超过了25万,所以是没有联邦保险的。据估计,这个数字可能高达97.3%。

钱拿不出来,工资发不出来,账单也付不起。

更糟糕的是,一家满足科技创业公司特定需求的银行,现在已经不复存在了。

此次事件堪称美国创投界的黑天鹅。

根据「特特理财」的分析,造成事件的最大元凶,就是美联储的不断加息。

本来,加息是为了降低通胀,让钱流回银行,然而硅谷银行做的是科技公司的贷款,既然获得贷款的成本越来越高,科技公司就开始大量把钱取出。

但问题来了,硅谷银行不仅因为买入大量固定收益类产品锁死了流动性,而且还各种上杠杆,试图用10亿美元贷出1000亿美元的效果。

具体来说,硅谷银行把价值910亿美元的存款,都放在了抵押贷款和美国国债等长期债券中。然而,在美联储积极提高利率后,现在的价值比硅谷银行当初购买时蒸发了150亿美元。

当地时间周三晚上,硅谷银行宣布将尝试在新股发行中筹集数十亿美元,并披露公司因出售受去年利率急剧上升影响的债券造成了18亿美元的损失。

消息一出,硅谷银行的股价在周四开始暴跌,这反过来又助长了美国创业公司从硅谷银行撤出资金的热潮。

感觉大事不妙的储户和投资者纷纷开始提现,总金额高达420亿美元。

这些操作不仅使硅谷银行的股价在周五进一步下跌,而且直接造成了美国这十几年来最大的银行挤兑之一。在当天上午的预交易中,其股价约为36美元,而在周三时则为267美元。

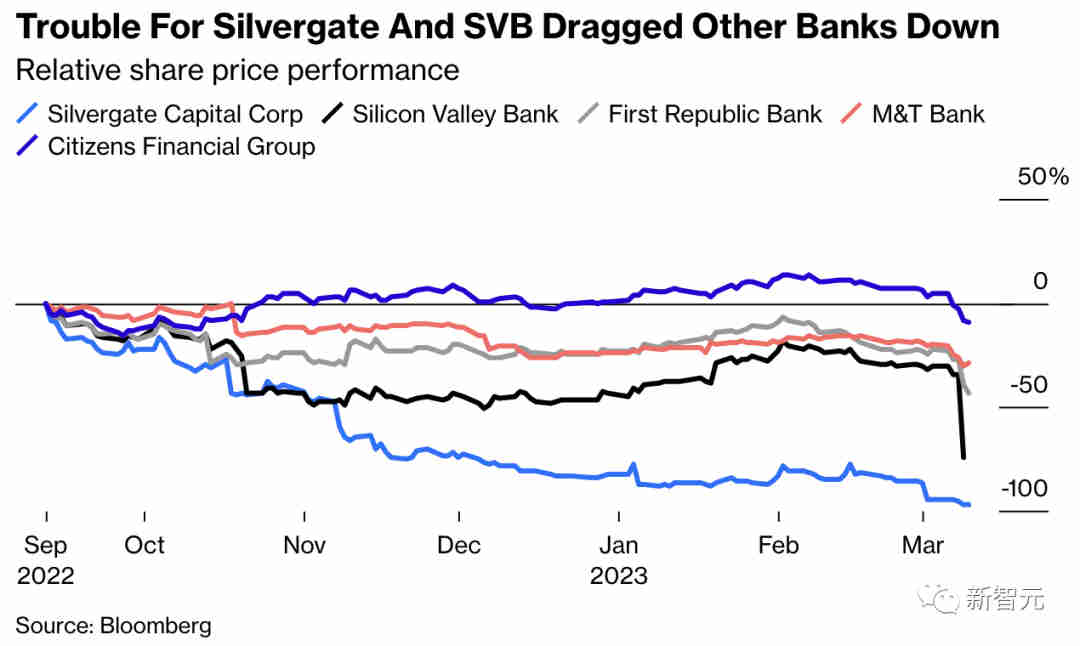

此外,硅谷银行的暴跌,也拖累欧美银行股指数重挫,导致摩根大通、美国银行、富国银行、花旗集团等美国四大银行的市值蒸发520亿美元。

搞不好,此次事件就会导致美国的金融危机,全世界都要跟着遭殃。

硅谷银行,或许就会是当年的雷曼兄弟。

据爆料,Meta向美国证券交易委员会(SEC)提交的文件显示,在2022年12月31日时,Meta在硅谷银行有约100亿美金的现金和等价物,占到Meta总资产的14%。

硅谷银行的部分客户包括:

- 科技初创公司,如Airbnb、Uber和LinkedIn。

- 生命科学公司:涉及生物技术、制药、医疗设备和医疗保健的生命科学公司,如Illumina和Intuitive Surgical。

- 风险资本家和私募股权公司:风险投资和私募股权公司,如红杉资本和Accel Partners。

- 新兴经理人:通过融资、银行和咨询服务为风险投资和私募股权领域的新兴经理人提供支持。

- 葡萄酒和饮料行业:为葡萄酒和饮料行业提供服务,包括酿酒厂、啤酒厂和酿酒厂,提供针对其独特需求量身定制的银行和金融服务。

- 公司和投资银行客户:为一系列客户提供公司和投资银行服务,包括中型市场和大型公司以及机构投资者。

二、硅谷银行,给了科技行业40年

可悲的是,硅谷银行给了科技行业40年,科技行业却连40小时的时间,都不给硅谷银行。

作为一家银行,专注于一个行业是有好处的,近一半的美国初创公司都会在硅谷银行开设银行业务。而随之而来的风险就是,客户的痛苦很快就会成为银行的痛苦。

而就如今这场大混乱的罪魁祸首——风险资本家,却似乎从骚乱中隐身了。正是他们对硅谷银行宣布筹集资金的消息作出反应,引发了对银行的挤兑,最终引起了大乱。

四十年来,硅谷银行一直是美国科技界的重要盟友,共同抵御着互联网的泡沫,和2008年的金融危机。然而,在问题出现的第一时间里,风投家们就立马关闭了银行,撺掇创始人拿走自己的钱。

风投们很乐意在出现问题的第一个迹象时就关闭银行,鼓励创始人拿走他们的钱。现在,他们的仓促行事把整个行业都拖入了危机。初创公司该如何支付工资?硅谷未来的融资需求将何去何从?

美国时间周四下午,彭博社界接连报道,一些最知名的风险投资公司,包括Peter Thiel的Founders Fund、Coatue Management 和Union Square Ventures,都在急催创始人把资金从硅谷银行中转移出去。

不久之后,其他行业也纷纷效仿。一些人试图警告大家不要反应过度,但为时已晚。

正如一位VC所说的那样,「我不认为硅谷银行会倒闭,但我也不想成为冤大头。」

但还没有开始就已经结束了,因为监管机构在宣布融资计划后不到48小时,就介入关闭了硅谷银行。

摩根士丹利周五早些时候的一份报告称,硅谷银行拥有「绰绰有余的流动性,足以为与风险投资客户烧钱相关的存款外流提供资金」,可用流动性资金约为 1800 亿美元,而资产负债表内的存款为1650亿美元。

也许在接下来的几天和几周内,硅谷银行会发现一些严重的会计渎职行为,事情崩溃只是时间问题。

而加州金融保护与创新金融部周五发布的一份新闻稿表示,由于「流动性不足和资不抵债」,它接管了硅谷银行,但没有透露更多细节。

三、利率对科技公司意味着什么?

可以说,正是曾经的低利率,促成了硅谷科技的十年繁荣。

自2008年金融危机以来,美联储几乎一直保持着低利率。然而在2021年11月,为应对通胀,美联储宣布加息。

现在,借贷会变得更昂贵,这意味着许多投资者不会投资股票,而是转而投资债券或国债。这会切实改变在低利率环境中蓬勃发展的科技行业。

沃顿商学院金融学教授Itay Goldstein表示,「一旦投资者不再投入新资金,那么所有初创公司的生存都将更加困难。」

由于借贷成本低,Netflix、特斯拉和戴尔等公司才能够举债。

很多企业都是在这个低利率时期诞生的,比如,加密货币正是对2008年金融危机的反应,在正常的利率环境中,加密货币从未存在过。

而加息后,投资者有了更多的回报选择, 较少的VC资金会使初创公司的吸引力降低。

随着消费者支出的收紧,电子产品的市场可能会减少,尤其是如果美联储如愿以偿,并且有更多人失业的话。

苹果、谷歌和亚马逊都是在正常利率时期诞生的。但现在,较少的VC资金使初创公司的工作场所吸引力降低。随着消费者支出的收紧,电子产品的市场可能会减少——尤其是如果美联储如愿以偿,并且有更多人失业的话。

而现在,硅谷银行已经倒闭,硅谷的科技公司还能继续运营吗?谁也不知道。

四、对中国投资者的影响

一夜之间,焦虑的情绪便蔓延到了中国。

在这个仅次于硅谷的世界第二大风险投资市场中,它的命运牵动着无数人。

20年前,硅谷银行在中国建立起了第一家分支机构——与上海浦东发展银行共同成立的合资银行。

根据The Information的报道,一位软件创业公司的创始人表示:「硅谷银行对于我们来说至关重要,因为最初的时候像花旗这样的银行都不愿意进行合作。」

随着硅谷银行的崩盘,中国初创公司想要在美国寻找合作银行与投资者,会变得更加困难……

翻译:

The first of the dominoes fell.

On March 9, Silicon Valley Bank (SVB), the nation’s 16th-largest, suddenly plunged more than 60%, wiping out $9.4 billion in market value.

On March 10, Silicon Valley Bank declared bankruptcy and was taken over by the Federal Deposit Insurance Corporation.

It is the biggest failure of the US financial sector since 2008.

But ironically, on March 7, Silicon Valley Bank made Forbes’ annual list of America’s Best Banks for the fifth year in a row and was named to Forbes’ inaugural Financial All-Star list.

Silicon Valley’s Darkest Hour

With about $209 billion in assets and $173.1 billion in deposits, Silicon Valley Bank primarily funds venture capital firms in Silicon Valley and is closely linked to venture capital across the Valley.

Garry Tan, the CEO of Y Combinator, posted this morning that the failure of Silicon Valley banks would be “catastrophic” for start-ups and set back American innovation by more than a decade.

Thirty percent of YC companies were affected by the failure of Silicon Valley banks. Without access to the funds, it would mean they would not be able to pay staff in as little as 30 days.

If we don’t find a solution, the startups of today, the Google and Meta of tomorrow, will disappear.

Nearly 400 startups said they were at risk, and more than 100 said they might not be able to make payroll in the next 30 days, according to the survey.

The bigger problem is that even though the FDIC took over and said it would pay depositors. But startup deposits in Silicon Valley banks, most of which exceed $250,000, are not federally insured. By some estimates, the figure could be as high as 97.3 percent.

I can’t get my money, I can’t get my wages, I can’t pay my bills.

To make matters worse, a bank that catered to the specific needs of tech startups no longer exists.

The event is a black swan for American venture capital.

According to analysis by Twitter Money, the biggest culprit is the Federal Reserve’s interest rate hikes.

The interest rate hike was supposed to lower inflation and get money flowing back to the banks, but Silicon Valley Bank made loans to technology companies, and now that loans are getting more expensive, tech companies are pulling money out in droves.

But the problem was that Silicon Valley banks not only locked up liquidity by buying lots of fixed-income products, but also leveraged themselves, trying to lend $100 billion out of $1 billion.

Specifically, Silicon Valley Bank has $91 billion worth of deposits tied up in mortgages and long-term bonds such as Treasury bonds. However, after the Fed aggressively raised interest rates, it is now worth $15 billion less than when Silicon Valley Bank bought it.

On Wednesday night, Silicon Valley Bank announced it would try to raise billions of dollars in a new share offering, disclosing a $1.8 billion loss from selling bonds exposed to last year’s sharp rise in interest rates.

The news sent shares of Silicon Valley Bank tumbling on Thursday, which in turn helped fuel a wave of U.S. startups pulling money out of Silicon Valley banks.

Savers and investors, sensing that something was wrong, began withdrawing $42 billion.

The moves not only sent Silicon Valley Bank’s share price down further on Friday, but also contributed directly to one of the biggest bank runs in the United States in more than a decade. Its shares were trading at about $36 in pre-trading that morning, compared with $267 on Wednesday.

In addition, the collapse of Silicon Valley Bank also dragged down European and U.S. bank stock indexes, wiping $52 billion off the market value of the four largest U.S. banks — jpmorgan Chase, Bank of America, Wells Fargo and Citigroup.

Or it could lead to a financial crisis in the United States and the rest of the world suffering.

Silicon Valley Bank might be Lehman Brothers.

According to the disclosure, Meta filed with the US Securities and Exchange Commission (SEC), as of December 31, 2022, Meta had approximately $10 billion in cash and equivalents in Silicon Valley Bank, representing 14% of Meta’s total assets.

Some of Silicon Valley Bank’s clients include:

1. Tech startups like Airbnb, Uber and LinkedIn.

2. Life science companies: Life science companies involved in biotechnology, pharmaceuticals, medical devices and healthcare, such as Illumina and Intuitive Surgical.

3. Venture capitalists and private equity firms: Venture capital and private equity firms such as Sequoia Capital and Accel Partners.

4. Emerging Managers: Support emerging managers in venture capital and private equity through financing, banking and advisory services.

5. Wine and beverage industry: For services to the wine and beverage industry, including wineries, breweries and distilleries, providing banking and financial services tailored to their unique needs.

6. Corporate and Investment Banking clients: Provides corporate and investment banking services to a range of clients, including mid-market and large corporations and institutional investors.

Silicon Valley Bank, which gave the tech industry 40 years

Sadly, Silicon Valley Bank gave the tech industry 40 years, but the tech industry won’t give Silicon Valley Bank 40 hours.

As a bank, it pays to focus on one industry: nearly half of all U.S. startups set up banking operations at Silicon Valley Banks. The risk is that the customer’s pain quickly becomes the bank’s pain.

Venture capitalists, the main culprits of today’s mayhem, seem to be hiding from the chaos. It was their reaction to Silicon Valley Bank’s announcement that it was raising capital that triggered a run on the bank that eventually led to mayhem.

For four decades, Silicon Valley Bank has been an important ally of the U.S. tech community, weathering the dotcom bubble and the 2008 financial crisis. In the first instance, however, VCS shut down banks and egged founders on to take their money.

VCS are happy to shut down banks at the first sign of trouble, encouraging founders to take their money. Now their haste has plunged the entire industry into crisis. How should startups pay salaries? What will happen to Silicon Valley’s future funding needs?

On Thursday afternoon, Bloomberg reported in quick succession that some of the most prominent venture capital firms, including Peter Thiel’s Founders Fund, Coatue Management and Union Square Ventures, Are rushing founders to move their money out of Silicon Valley banks.

Before long, other industries followed suit. Some tried to warn everyone not to overreact, but it was too late.

As one VC put it, “I don’t think Silicon Valley Bank will fail, but I don’t want to be a sucker either.”

But it was over before it even began, as regulators stepped in to shut down Silicon Valley Bank less than 48 hours after the capital raising was announced.

A Morgan Stanley report earlier on Friday said Silicon Valley Bank had “more than enough liquidity to fund deposit outflows related to the burn of venture capital clients”, with about $180bn in available liquid funds compared with $165bn in deposits on its balance sheet.

Perhaps in the coming days and weeks, Silicon Valley banks will uncover some serious accounting malfeasance, and it’s only a matter of time before things fall apart.

A press release Friday from the California Department of Financial Protection and Innovation Finance said it took over Silicon Valley Bank due to “illiquidity and insolvency,” but gave no further details.

What do interest rates mean for tech companies?

Arguably, it was low interest rates that led to the Silicon Valley tech boom of the decade.

The Fed has kept interest rates low almost continuously since the 2008 financial crisis. In November 2021, however, the Fed raised interest rates in response to inflation.

Now, borrowing will become more expensive, which means many investors will move away from stocks and into bonds or Treasurys. That could make a real difference to a tech industry that thrives in a low-interest rate environment.

“Once investors stop putting in new money, it’s going to be harder for all startups to survive,” said Wharton finance professor Itay Goldstein.

Companies such as Netflix, Tesla and Dell have been able to borrow because of their low borrowing costs.

Many businesses were born during this period of low interest rates. Cryptocurrencies, for example, were a reaction to the 2008 financial crisis and would never have existed in a normal interest rate environment.

With higher rates, investors have more options for returns, and less VC money makes startups less attractive.

As consumer spending tightens, the market for electronics could shrink, especially if the Fed gets its way and more people lose their jobs.

Apple, Google and Amazon were all born at a time of normal interest rates. But now, less VC money is making the startup workplace less attractive. As consumer spending tightens, the market for electronics could shrink – especially if the Fed gets its way and more people lose their jobs.

Now that Silicon Valley Bank has collapsed, can Silicon Valley tech companies continue to operate? No one knows.

The impact on Chinese investors

Overnight, anxiety spread to China.

Its fate matters to millions in the world’s second-largest venture capital market after Silicon Valley.

Silicon Valley Bank opened its first branch in China 20 years ago, in a joint venture with Shanghai Pudong Development Bank.

According to The Information, one founder of a software startup said, “Silicon Valley Bank was critical to us because banks like Citi were reluctant to cooperate in the beginning.”

With the collapse of Silicon Valley banks, it will be harder for Chinese startups to find banks and investors in the United States…

本文由数字化转型网(www.szhzxw.cn)转载而成,来源:新智元;编辑/翻译:数字化转型网宁檬树。

免责声明: 本网站(https://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。