为规范企业数据资源相关会计处理,强化相关会计信息披露,近日,财政部制定印发了《企业数据资源相关会计处理暂行规定》(以下简称《暂行规定》),自2024年1月1日起施行。

一、《暂行规定》的要点内容

(一)《暂行规定》不涉及对现有会计准则的突破,进一步体现了会计的谨慎性原则。

根据答记者问中的相关表述,《暂行规定》是“明确企业数据资源适用于现行企业会计准则,不改变现行准则的会计确认计量要求”,并是对“现行企业会计准则体系下的细化规范,在会计确认计量方面与现行无形资产、存货、收入等相关准则是一致的,不属于国家统一的会计制度要求变更会计政策”。相较于《征求意见稿》阶段,《暂行规定》进一步体现了会计的谨慎性原则,删去了《征求意见稿》中“发挥数据要素价值”、《征求意见稿》起草说明中“合理反映数据要素价值”等表述,避免了“数据要素”这一经济学概念对会计学意义上“数据资源”(由“信息资源”衍生而来)的干扰,更加聚焦企业数据资源的会计处理过程。

(二)《暂行规定》修改了数据资产入表的业务模型,进一步细化了不同业务模式下的会计处理。

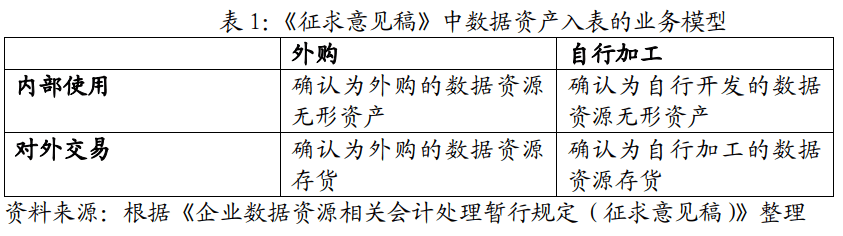

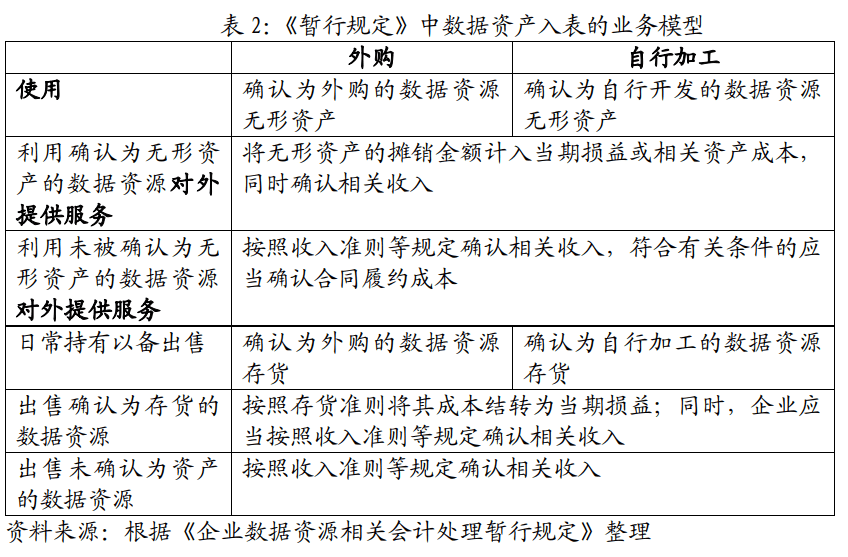

在《征求意见稿》阶段,数据资产入表的业务模型主要集中在“数据交易双方如何进行会计处理”,采用“二分法”分为“企业内部使用的数据资源相关会计处理”和“企业对外交易的数据资源相关会计处理”。在《暂行规定》中,则是根据企业使用、对外提供服务、日常持有以备出售等不同业务模式,明确相关会计处理适用的具体准则,并进一步明确了不满足资产确认条件而未予确认的数据资源的相关会计处理。

(三)《暂行规定》增加数据资源在企业资产负债表中的列示,进一步明确了“表内确认”要求。

关于数据资产入表一直有“表内确认观”和“表外披露观”等不同观点。“表内确认观”又分为数据资源作为单独会计科目核算和放入已有会计科目核算的不同路径;“表外披露观”则主张在管理层分析与讨论或报表附注中披露数据资源。《征求意见稿》中对数据资源仅有在会计报表附录中进行披露的要求,一定程度上体现了“表外确认观”的思路。《暂行规定》则明确了企业数据资源在资产负债表中的相关列示,进一步明确了数据资源要基于既有会计科目进行“表内确认”的要求。《暂行规定》要求,企业在编制资产负债表时,应当根据重要性原则并结合本企业的实际情况,在“存货”项目下增设“其中:数据资源”项目,反映资产负债表日确认为存货的数据资源的期末账面价值;在“无形资产”项目下增设“其中:数据资源”项目,反映资产负债表日确认为无形资产的数据资源的期末账面价值;在“开发支出”项目下增设“其中:数据资源”项目,反映资产负债表日正在进行数据资源研究开发项目满足资本化条件的支出金额。数字化转型网www.szhzxw.cn

(四)《暂行规定》创新采取“强制披露加自愿披露”方式,对企业财务报表具有重要影响的数据资源相关信息进行强制披露,同时对有利于增强企业财务报表可理解性的数据资源相关信息进行自愿性披露,进一步强化数据资源相关信息披露。

《暂行规定》围绕各方的信息需求重点,一方面细化会计准则要求披露的信息,另一方面鼓励引导企业持续加强自愿披露,向利益相关方提供更多与发挥数据资源价值有关的信息,兼顾信息需求、成本效益和商业秘密保护。对企业财务报表具有重要影响的数据资源相关信息进行强制披露,如数据资源无形资产使用寿命的估计情况及摊销方法、数据资源存货可变现净值的确定依据等;对有利于增强企业财务报表可理解性的数据资源相关信息进行自愿性披露,如数据资源的应用场景或业务模式、对企业创造价值的影响方式,与数据资源应用场景相关的宏观经济和行业领域前景等。

(五)《暂行规定》将自2024年1月1日起施行,企业应当采用未来适用法应用规定。

根据《暂行规定》,企业对可比期间的信息不予追溯调整,如在规定施行前已费用化计入当期损益的数据资源相关支出不再调整,即不应将前期已经费用化的数据资源重新资本化。

二、 相关企业如何适用《暂行规定》

根据答记者问相关要求,企业在贯彻实施《暂行规定》时需要注意下列事项:

(一)正确做好前后衔接。

《暂行规定》是在现行企业会计准则体系下的细化规范,在会计确认计量方面与现行无形资产、存货、收入等相关准则是一致的,不属于国家统一的会计制度要求变更会计政策。同时,《暂行规定》要求采用未来适用法应用本规定,企业在本规定施行前已费用化计入当期损益的数据资源相关支出不再调整,即不应将前期已经费用化的数据资源重新资本化。

(二)严格执行企业会计准则。

《暂行规定》执行后,相关企业报表表观将得到改善。原来相关会计活动计入期间费用影响当期损益,现在可以计入资产,改善资产负债率,减少投入期对利润的影响,改善利润率。但是,企业应当严格按照企业会计准则关于相关资产的定义和确认条件、无形资产研究开发支出的资本化条件等规定以及《暂行规定》的有关要求,结合企业数据资源的实际情况和业务实质,综合所有相关事实和情况,合理作出职业判断并进行会计处理。数字化转型网www.szhzxw.cn

(三)积极加强信息披露。

企业应当充分认识提供有关信息对帮助更好理解财务报表、揭示数据资源价值的重要意义,主动按照企业会计准则和《暂行规定》的披露要求,持续加强对数据资源的应用场景或业务模式、原始数据类型来源、加工维护和安全保护情况、涉及的重大交易事项、相关权利失效和受限等相关信息的自愿披露,以全面地反映数据资源对企业财务状况、经营成果等的影响。

三、 企业数据资产入表的意义

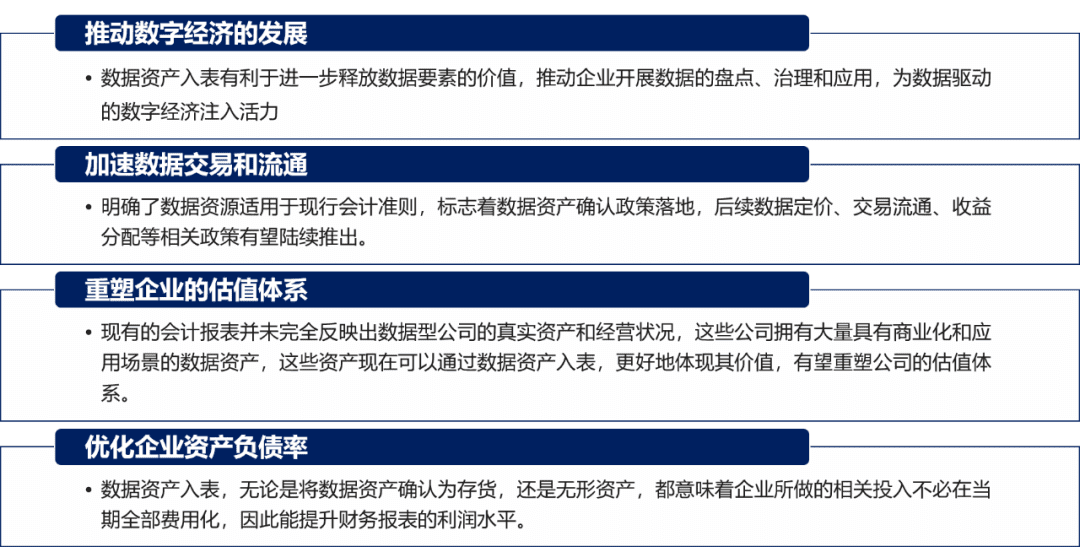

推动数字经济的发展:数据资产入表有利于进一步释放数据要素的价值,推动企业开展数据的盘点、治理和应用,为数据驱动的数字经济注入活力

加速数据交易和流通:明确了数据资源适用于现行会计准则,标志着数据资产确认政策落地,后续数据定价、交易流通、收益分配等相关政策有望陆续推出。

重塑企业的估值体系:现有的会计报表并未完全反映出数据型公司的真实资产和经营状况,这些公司拥有大量具有商业化和应用场景的数据资产,这些资产现在可以通过数据资产入表,更好地体现其价值,有望重塑公司的估值体系。

优化企业资产负债率:数据资产入表,无论是将数据资产确认为存货,还是无形资产,都意味着企业所做的相关投入不必在当期全部费用化,因此能提升财务报表的利润水平。

四、数据资产入表的基础认知

(一)文件的出台背景是回应理论界和实务界的呼声。

这个文件并不修改现行会计准则,也没有提供增量会计规则,只是对现行会计准则的重申和针对性的细化。文件中介绍说明中明确写到:《暂行规定》在充分论证的基础上,明确企业数据资源充分适用于现行企业会计规则,不改变现行总则的会计确认计量要求。

(二)不能将文件简单解读为允许数据资产入表。

因为该文件没有改变现行会计准则规定,也没有提供增量会计规则,只是对现行准则的重申何针对性的细化。数字化转型网www.szhzxw.cn

(三)很多问题本身不存在,比如数据资产入表时价值如何评估等,这与入表无关。

(四)确权和交易是数据资产非常重要的问题。

确权和交易都属于会计的前提而不是会计本身。这个文件既不解决数据资产确权问题,也不解决交易问题。确权是法律问题,交易是市场问题,交易的前提是确权,确权后才能交易,这些都不是会计问题。

(五)文件出台会让会计师处理数据资产相关支出时向资本化倾斜

影响可能体现在文件发了以后,会计职业界,尤其是注册会计师在判断一项数据相关资产入账时会比原来积极一些,具体积极到什么程度没法猜测。没有这个文件时,一笔和数据资产有关的支出会计师可能更倾向于把它费用化;文件出来后,会计师有可能会更激进一些,考虑资本化处理,使得有一些资产入账。但是这个量不大,并且只针对未来增量资产,不涉及存量数据资产入表的问题。

英文翻译:

In order to standardize the accounting treatment related to enterprise data resources and strengthen the disclosure of relevant accounting information, the Ministry of Finance recently formulated and issued the Interim Provisions on Accounting Treatment Related to Enterprise Data Resources (hereinafter referred to as the Interim Provisions), which will take effect from January 1, 2024.

Main points of the Provisional Provisions

(1) The “Provisional Provisions” do not involve a breakthrough in the existing accounting standards, and further reflect the principle of accounting prudence.

According to the relevant statements in the answer to the reporter’s question. The “provisional provisions” are “clear that the enterprise data resources are applicable to the current enterprise accounting standards. And do not change the accounting recognition measurement requirements of the current standards” . And are “detailed specifications under the current enterprise accounting standards system, in terms of accounting recognition measurement. And the current intangible assets, inventories, income and other relevant standards are consistent.”

Accounting systems that are not part of the national uniform system require changes in accounting policies.” Compared with the “Draft for Comments” stage, the “Provisional Provisions” further reflects the principle of accounting prudence, deleting the “draft for Comments” in the “play the value of data elements”, “reasonable reflection of the value of data elements” in the drafting instructions of the draft for comments. It avoids the interference of the economic concept of “data elements” to the “data resources” (derived from “information resources”) in the accounting sense, and focuses more on the accounting process of enterprise data resources.数字化转型网www.szhzxw.cn

(2) The Provisional Provisions modify the business model of data assets entering the statement and further refine the accounting treatment under different business models.

In the phase of the Draft for Comments, the business model of data asset entry into the table mainly focuses on “how to conduct accounting treatment between the two parties to the data transaction”, and adopts a “dichotomy” to divide into “accounting treatment related to data resources used within the enterprise” and “accounting treatment related to data resources of the enterprise’s external transactions”. In the “Provisional Provisions”, the specific standards applicable to relevant accounting treatment are clarified according to different business models such as enterprise use, external service provision, daily holding for sale, and further clarify the relevant accounting treatment of data resources that do not meet the conditions for asset recognition and are not recognized.

(3) The Interim Provisions increase the listing of data resources in the balance sheet of the enterprise, and further clarify the requirements of “acknowledgement in the statement”.

There have always been different views on data asset entry into the statement, such as “on the statement recognition view”. And “off the statement disclosure view”. The “view of recognition in the statement” can be divided into different ways of accounting data resources as separate accounting items. And accounting in existing accounting items. The “off-balance sheet disclosure approach” advocates the disclosure of data resources in management analysis. And discussion or in notes to financial statements. The requirement of disclosure of data resources only in the appendix of accounting statements in the Draft for Comments reflects the idea of “off-balance sheet confirmation” to a certain extent.

The “Interim Provisions” clarify the relevant listing of enterprise data resources in the balance sheet. And further clarify the requirements of “in-table recognition” of data resources based on existing accounting accounts. The Provisional Provisions require that when an enterprise is preparing a balance sheet. It shall, in accordance with the principle of materiality. And in combination with the actual situation of the enterprise, add a “Wherein: data resources” item under the “inventory” item to reflect the ending book value of the data resources recognized as inventories on the balance sheet date.

Add the item “Where: Data Resources” under the item “Intangible Assets” to reflect the ending book value of data resources recognized as intangible assets at the balance sheet date. Add the item “Where: Data Resources” under the item . “Development Expenditure” to reflect the amount of expenditure to meet the capitalization conditions for the ongoing research . And development of data resources at the balance sheet date.数字化转型网www.szhzxw.cn

(4) The Interim Provisions innovatively adopt the method of “mandatory disclosure plus voluntary disclosure” to make mandatory disclosure of information related to data resources that have an important impact on the financial statements of enterprises.

And at the same time make voluntary disclosure of information related to data resources that are conducive to enhancing the comprehensibility of the financial statements of enterprises . And further strengthen the disclosure of information related to data resources.

The Provisional Provisions focus on the information needs of all parties, on the one hand. Specify the information required to be disclosed by accounting standards, on the other hand, encourage. And guide enterprises to continue to strengthen voluntary disclosure, provide more information related to the value of data resources to stakeholders. And take into account information needs, cost effectiveness and trade secret protection.

Mandatory disclosure of information related to data resources that have an important impact on the financial statements of enterprises, such as the estimation. And amortization method of the service life of intangible assets of data resources. The basis for determining the net realizable value of data resource inventories, etc. Voluntary disclosure of information related to data resources that are conducive to enhancing the comprehensibility of corporate financial statements, such as application scenarios or business models of data resources, ways of influencing enterprise value creation, macroeconomic and industry prospects related to data resource application scenarios, etc.数字化转型网www.szhzxw.cn

(5) The Provisional Provisions will take effect from January 1, 2024, and enterprises shall adopt the application provisions of the Future Application Law.

According to the “Interim Provisions”, the enterprise will not retroactively adjust the information of the comparable period, if the data resource related expenditure that has been expensed in the profit and loss of the current period before the implementation of the provisions is no longer adjusted, that is. The data resource that has been expensed in the previous period should not be re-capitalized.

How relevant enterprises apply the Provisional Provisions

According to the relevant requirements, enterprises need to pay attention to the following matters when implementing the Provisional Provisions:

(1)Ensure proper coherence.

The “Interim Provisions” is a detailed specification under the current accounting standards system for enterprises, which is consistent with the current intangible assets, inventories, income. And other relevant standards in accounting recognition and measurement. And does not belong to the national unified accounting system requiring changes in accounting policies. At the same time, the “Interim Provisions” requires the application of the future application of the provisions, the enterprise before the implementation of the provisions have been expensed into the profit and loss of the current period of the data resources related expenses are no longer adjusted, that is, the data resources that have been expensed in the earlier period should not be re-capitalized.

(2) Strictly implement accounting standards for enterprises.

After the implementation of the “Provisional Provisions”, the appearance of the relevant enterprise statements will be improved. Previously, the relevant accounting activities were included in the period expenses to affect the current profit and loss. But now they can be included in assets to improve the asset-liability ratio. Reduce the impact of the investment period on profits. And improve the profit margin. However, enterprises shall, in strict accordance with the provisions of the Accounting Standards for enterprises on the definition . And recognition conditions of relevant assets, the capitalization conditions of intangible assets research and development expenditures. And the relevant requirements of the Provisional Provisions, combine the actual situation of enterprise data resources and business essence, synthesize all relevant facts and circumstances, and make a reasonable professional judgment and accounting treatment.

(3) Actively strengthen information disclosure.

Enterprises shall fully understand the significance of providing relevant information to help better understand financial statements. And reveal the value of data resources. And take the initiative to comply with the disclosure requirements of the Accounting Standards for enterprises and the Interim Provisions. Continue to strengthen the voluntary disclosure of relevant information such as application scenarios or business models of data resources, sources of original data types, processing, maintenance and security protection, major transactions involved. And the invalidity and limitation of relevant rights, so as to comprehensively reflect the impact of data resources on the financial status and operating results of enterprises.

The significance of enterprise data assets into the table

Promote the development of digital economy: The entry of data assets into the table is conducive to further releasing the value of data elements, promoting enterprises to carry out data inventory, governance and application, and injecting vitality into the data-driven digital economy

Accelerate data transaction and circulation: It is clear that data resources are applicable to the current accounting standards, marking the landing of data asset confirmation policy. And subsequent data pricing, transaction circulation, income distribution . And other related policies are expected to be introduced one after another.

Reshape the valuation system of enterprises: the existing accounting statements do not fully reflect the real assets. And business conditions of data-oriented companies. These companies have a large number of data assets with commercialization and application scenarios. And these assets can now be entered into the table through data assets to better reflect their value, which is expected to reshape the valuation system of companies.数字化转型网www.szhzxw.cn

Optimize enterprise asset-liability ratio: Data assets are entered into the statement, whether the data assets are recognized as inventories or intangible assets, it means that the relevant investment made by the enterprise does not have to be fully cost in the current period, so it can improve the profit level of financial statements.

Basic cognition of data assets entering the table

(1) The background of the introduction of the document is to respond to the voice of the theoretical and practical circles.

This document does not modify the current accounting standards, nor does it provide incremental accounting rules . But merely reiterates and refines the current accounting standards. The introduction notes in the document clearly write: “Interim Provisions” on the basis of full demonstration. It is clear that enterprise data resources are fully applicable to the current enterprise accounting rules. And do not change the accounting recognition and measurement requirements of the current general rules.

(2) The document should not be interpreted simply as allowing data assets to enter the table.

Because the document does not change the current accounting standards provisions, nor does it provide incremental accounting rules, only the reiteration of the current standards how targeted refinement.

(3) Many problems do not exist in themselves, such as how to evaluate the value of data assets when they are entered into the statement, which has nothing to do with the entry into the statement.

(4) Confirmation and transaction are very important issues for data assets.

Both rights and transactions belong to the premise of accounting rather than accounting itself. This document does not address the issue of ownership of data assets, nor does it address the issue of transactions. Right confirmation is a legal issue, transaction is a market issue. The premise of transaction is to confirm the right, after confirming the right to transaction. These are not accounting issues.

(5) The introduction of documents will allow accountants to treat data asset-related expenses with a bias toward capitalization

The impact may be reflected in the fact that after the document is issued, the accounting profession, especially the CPA, will be more active in judging the entry of a data-related asset than before, to what extent it is impossible to guess. Without this document, an accountant may be more inclined to charge for an expense related to a data asset; After the documents come out, the accountant may be more aggressive and consider capitalizing, so that some assets are recorded. But this amount is not large, and only for future incremental assets, does not involve the inventory of data assets into the table.

本文由数字化转型网(www.szhzxw.cn)转载而成,来源于 谈数据;编辑/翻译:数字化转型网小汤圆。

免责声明: 本网站(https://www.szhzxw.cn/)内容主要来自原创、合作媒体供稿和第三方投稿,凡在本网站出现的信息,均仅供参考。本网站将尽力确保所提供信息的准确性及可靠性,但不保证有关资料的准确性及可靠性,读者在使用前请进一步核实,并对任何自主决定的行为负责。本网站对有关资料所引致的错误、不确或遗漏,概不负任何法律责任。

本网站刊载的所有内容(包括但不仅限文字、图片、LOGO、音频、视频、软件、程序等) 版权归原作者所有。任何单位或个人认为本网站中的内容可能涉嫌侵犯其知识产权或存在不实内容时,请及时通知本站,予以删除。